Part 1: The Making of a Debt Crisis

This three-part series examines the life cycle of a debt crisis and looks at where the US, UK and eurozone are in the recovery process. This first post explains the phases of a debt crisis. Part 2 will look at where the US stands in the deleveraging process, while Part 3 will focus on why the UK and eurozone lag the US in balance-sheet repair.

Investors are inundated with media commotion about the US debt ceiling/default dilemma, the Federal Reserve’s tapering strategy and other issues. But this chatter distracts from what really matters when it comes to economic recovery — repairing balance sheets in the private sector.

Life cycle of a debt crisis

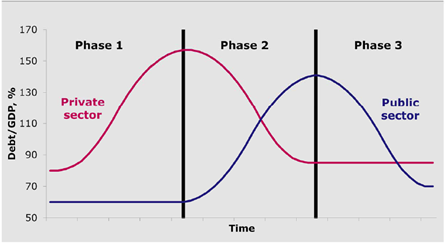

The emergence of a credit bubble and its aftermath — the process of “bubble and burst” — may be visualized as two overlapping bell curves, as shown below. The curves illustrate the typical trajectory of leverage — the ratio of debt to income, measured by gross domestic product (GDP) — in the private and public sectors.

Debt Crisis: Two Curves, Three Phases

Source: Invesco, for illustrative purposes only

A debt crisis occurs over three phases:

- Phase 1: The bubble inflates, financed by rising debt-to-income ratios in the private sector.

- Phase 2: After the bubble has burst, the private sector typically starts to deleverage by reducing spending, repaying debt and repairing balance sheets. These spending cutbacks trigger recession, which, in turn, results in declining government revenues, government budget deficits and a higher ratio of government debt to GDP. As the recession intensifies, the government may also commit to additional fiscal stimulus measures, further expanding the public sector’s deficits and debt ratio. That’s why the government’s debt ratio typically starts to rise steeply at exactly the moment when the private sector begins to deleverage.

- Phase 3: Eventually, private-sector balance sheets are repaired, and normal growth can resume. The recovery of private-sector growth restores government revenues, narrows the fiscal deficit and enables the government debt-to-GDP ratio to start declining.

Part 2 of this series will examine why the US is outpacing both the UK and the eurozone in balance-sheet repair and recovery from the debt crisis.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

|

NOT FDIC INSURED |

MAY LOSE VALUE |

NO BANK GUARANTEE |

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is a US distributor for retail mutual funds, exchange-traded funds, institutional money market funds and unit investment trusts. Van Kampen Funds Inc. is a sponsor of unit investment trusts. Both entities are wholly owned, indirect subsidiaries of Invesco Ltd.

© 2013 Invesco Ltd. All rights reserved.