ING Fixed Income Perspectives - November 2013

ING U.S. Investment Management

Fixed Income Perspectives

November 27, 2013

Christine Hurtsellers, CFA

Chief Investment Officer, Fixed Income and Proprietary Investments

Matt Toms, CFA

Head of U.S. Public Fixed Income

Bond Market Outlook

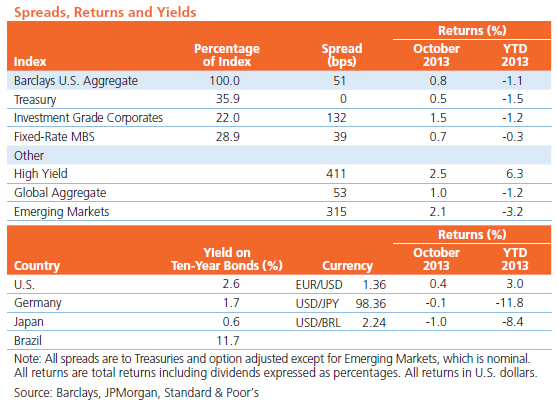

Global Interest Rates: Given rich valuations globally, we remain broadly neutral on interest rate risk with the exception of Japan.

Global Currencies: Positive growth and reduced easing will support the U.S. dollar; we are bearish on the yen and euro, favoring export-driven EM currencies.

Corporates: Spreads are near the year’s lows and should generally tighten toward year-end, though October’s rally may have reduced some of the upside.

High Yield: With investors fearful of interest rate risk, high yield flows have been positive and the market remains biased to the upside.

Mortgages: While the market remains supported by the Fed, the reaction of rate-sensitive mortgages to eventual QE tapering is a dominant concern.

Emerging Markets: Outflows remain a key driver of performance; we favor hard currency sovereigns over corporates.

Macro Overview

- Happy Thanksgiving! Notwithstanding the turkeys in Washington and the absence of a fiscal deal with all the trimmings, there’s plenty to be thankful for this holiday season. Multiple helpings of quantitative easing and nearly five years of zero interest rate policy — now served à la mode with forward interest rate guidance — helped spawn the resurgent housing sector and recovering labor market we enjoy today. As the impulse for fiscal tightening wanes and the U.S. economy continues to grow, the Fed can start gobbling a smaller share of Treasury and agency MBS issuance — hopefully without souring the market’s risk appetite in the process. Market behavior will continue to be driven by a dovish Fed likely to remove monetary accommodation late rather than early, keeping interest rates lower for longer, the housing market nourished, the labor market and household wealth improving, and the appetite for domestic equity and fixed income healthy.

- So why not celebrate with a second helping of risky assets? The concern underlying all this quantitative binging — not only by the U.S. but notably in Europe and Japan — has been deflation. With no signs of inflationary consequences to date, the Fed has convinced the market that it’s possible to battle the “D” word without any harmful inflationary repercussions. But what if the Fed and other central bankers are wrong? Any emergence of inflation fears would threaten the Fed’s ability to continue its accommodative policies, likely resulting in volatility and a re-pricing of risk across all asset classes.

- Thankfully, inflationary pressures will continue to be subdued, as the global propensity to save outweighs the impulse to consume. And while the forces of deflation are still at work in the world and U.S. growth likely will be lower than widely assumed, the world’s largest economy is poised to generate 2014 growth in excess of the long-term trend. Combined with improvements outside our borders, this should keep the “D” word at bay and help sustain a healthy appetite for risky assets. While QE gyrations may inspire bouts of market nausea, the distinction between tapering and rate hikes will keep higher-yielding “carry” assets in favor. Fixed income valuations, while no longer cheap, are fair by our estimation and are likely to become significantly richer before the turn of the cycle.

Sector Overviews

Global Interest Rates

- Despite strong October payroll data, Treasuries five years and shorter haven’t really budged, suggesting the Fed may have succeeded in its efforts to distinguish tapering from rate hikes in the mind of the market. This should limit volatility and help insulate spread sectors from a selloff when tapering finally begins.

- Economic growth has improved since the summer, and the improvement is likely to continue through first quarter 2014. Rates are above fair value in the U.S., and fair value is likely to increase, though slowly enough to allow for positive total returns given the FOMC’s strong commitment to dovish guidance.

- For the first time in years, long-term rates impacted more by tapering expectations are offering a clear term premium. If long-dated forwards (e.g., 10y10y) move above 5%, that may signal a reasonable buying opportunity, though caution is warranted between now and the beginning of tapering. Given rich valuations across the developed and emerging worlds, we remain broadly neutral on interest rate risk, with the exception of Japan.

Global Currencies

- Positive growth, higher U.S. rates and the expectation of reduced Fed easing will be supportive of the U.S. dollar. We remain bearish on the Japanese yen and are less constructive on the euro in the wake of the recent ECB rate cut that was inspired by mounting fears of deflation. As developed market central banks remain accommodative, emerging market currencies are selectively attractive. Downside risks are prominent, particularly for countries with weaker economic fundamentals and larger external funding needs; instead, we favor export-driven economies in Asia and EMEA that will benefit from the marked improvement in China.

Investment Grade Corporates

- Spreads are near the year’s lows. Corporate fundamentals showed slight improvement during the third quarter, but leverage continues to slowly increase. November supply has been heavy; spreads traded sideways earlier in the month before moving to their tightest levels since the crisis. Recent years have seen spreads generally tighten during the final months of the year, but the surprisingly strong October rally may have diminished some of the upside.

- Spreads should remain well-supported into 2014 given the fading impact of fiscal tightening, positive global macro conditions and the expectation of accommodative monetary policy. However, higher interest rates and shifting expectations about the timing and impact of Fed tapering may act as a headwind.

High Yield Bonds

- Margins continue to hold up well due to cost control, but top-line growth remains difficult to come by. Leverage has increased from post-crisis lows but remains below prior-cycle highs, and low financing rates have kept interest coverage near historical highs. The bulk of issuance continues to go to refinancings.

- Flows have been positive, and the market remains biased to the upside. With investors more concerned about interest rate risk than credit risk, high yield spreads offer more-than-adequate compensation for likely credit losses and the ability to absorb at least a portion of any further rise in interest rates. While prices are off their highs, CCCs are still trading above par, heightening the importance of credit selection and the early detection of credit problems. Withdrawal of stimulus, political discord and anemic global growth expectations are the largest concerns.

Mortgages

- Higher financing costs, renewed HARP fears and tapering expectations have kept most MBS participants other than the Fed on the sidelines. Supply has fallen consistently of late and Fed buying will keep the mortgage basis supported for now; however, net issuance will turn positive after QE, leaving considerable slack for investors to digest. Higher coupons look more attractive in this environment.

- Non-agency RMBS spreads have shown little movement in recent weeks. New issuance is expected to be relatively quiet through year-end; the technical picture, while improved since the summer, remains exposed. The yield or carry advantage remains positive, but taper talk could result in spread widening.

- Though the relative value case for CMBS can still be made, the primary impediments to sustained tightening — i.e., supply concerns and a reluctance to buy duration — have re-emerged. An upsized new-issue pipeline coupled with taper concerns will lead longer-duration new-issue paper to underperform legacy product. Going forward, there will be a premium on security selection as losses begin to materialize and valuations disperse.

Emerging Markets

- Outflows remain one of the key drivers of performance across the EM complex. The extension of Fed bond buying and accommodative monetary policy globally gives us greater conviction that emerging markets will stabilize, particularly as fundamentals improve for countries like China. On the hard currency side, we expect corporates to underperform sovereigns. Our outlook is skewed to the downside on the local currency side, particularly for countries with weaker economic fundamentals and larger external funding needs.

ING U.S. Investment Management’s fixed income strategies cover a broad range of maturities, sectors and instruments, giving investors wide latitude to create a new portfolio structure or complement an existing one. We offer investment strategies across the yield curve and credit spectrum, as well as in specialized disciplines that focus on individual market sectors. We build portfolios one bond at a time, with a critical review of each security by experienced fixed income managers. As of June 30, 2013 ING U.S. Investment Management managed $121 billion in fixed income strategies in the United States.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 8020

© ING Investment Management