From the Taj Mahal to Westminster Abbey: Notes from a Global Investor

From the Taj Mahal to Westminster Abbey: Notes from a Global Investor

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

|

|

I recently returned from India, a nation where an incredible 600 million people are under the age of 25. That’s nearly double the entire population of the U.S.!

What’s amazing about that figure is that, unlike the 1970s when India had no global footprint, today’s generation is increasingly gaining access to the Internet.

Social networking platforms are seeing an incredible growth trajectory in India, as one of the fastest growing markets. In fact, by 2016, the country is set to be Facebook’s largest population in the world, according to the BBC.

While Forbes India reports that there are only 137 million users in India, with the growing population and rising wealth, we expect this number to grow substantially.

I believe this connectivity changes the growth pattern for commodities. Like I told Kitco’s Daniela Cambone at the Metals & Minerals Investment Conference in San Francisco, this population carries on its love of gold. Mineweb reports that about 1 million couples will marry this wedding season, with around 33,000 weddings taking place on November 19 alone.

Gold traditionally accompanies these events, and a typical gift is “a pendant, earrings or a ring, weighing 5-10 grams depending on financial circumstances. Parents of the bride generally give heavier items like a necklace or bangles weighing 50 grams or more,” according to Mineweb.

Still, to help manage expectations, investors should anticipate a short-term headwind for the precious metal as India’s GDP per capita has stalled. The World Bank estimated India to grow 6.1 percent this year, but lowered its forecast to 4.7 percent due to a slowdown in manufacturing and investment.

The long-term picture looks positive though. While India grew at 4.8 percent in the third quarter, the finance ministry is confident the country can return to its “high-growth plan.” It projects the economy to pick up, accelerating to around 6 percent in the next fiscal year and about 8 percent in another two years, says The Wall Street Journal.

India’s growing GDP is very important to gold’s rise, especially when it comes to the Love Trade, where about 50 percent of the world’s population buys gold out of love. The math shows that an increasing GDP per capita in this part of the world has historically been linked to the rising price of gold.

Related to the Fear Trade—buyers holding the metal out of fear of poor government policies—gold has recently become less attractive due to the slightly positive real interest rates in the U.S.

As we explain in our Special Gold Report on the Fear Trade, one of its strongest drivers is real interest rates, which is when the inflationary rate of return is greater than the current interest rate.

Our model tells us that a real interest rate of more than 2 percent is typically bearish for gold.

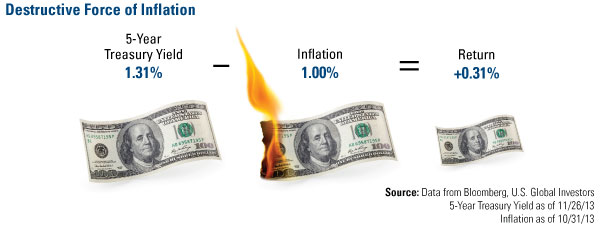

Still, the real rate is not very close to the 2-percent tipping point. As of the end of November, the 5-year Treasury yield is 1.31 percent while inflation is at 1 percent. Investors end up with a slightly positive return of 0.31 percent.

click to enlarge

With onerous regulations continuing to slow down the flow of money, I believe the government will need to keep its printing presses warm, eventually reigniting the Fear Trade.

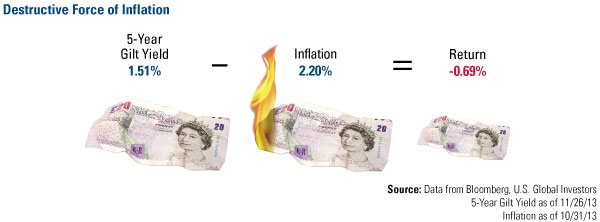

Keep in mind that real rates are not positive in every country. As I will be showing in my presentation at the Mines and Money conference in London, U.K. investors are still losing money after inflation. The 5-year gilt yield is at 1.51 percent, but inflation is at 2.2 percent, resulting in a negative real rate of return.

click to enlarge

What Are You Thankful For?

Sitting around a table with family and friends at Thanksgiving is an ideal time to reflect on the priceless value of our loved ones. I am also thankful for the thousands of loyal and curious readers who choose to spend their time every weekend reading the Investor Alert to keep informed with what’s going on in the investment world.

In the spirit of this holiday weekend, here’s one additional thing investors can be thankful for: The nearly 30 percent return in U.S. stocks so far this year.

|

|

This is despite Americans being bombarded with negative messages of the health care reform. TIME printed a busted “Obamacare” pill accompanied by the headline, “Broken Promise: What It Means for This Presidency.” The Economist features an image of President Barack Obama sinking in water with the headline, “The man who used to walk on water.” This November, Obama’s approval rating sank to a new all-time low.

While the government may not be functioning well right now, there is a lot that is working well in America. The stock market reflects that, even though the headlines don’t.

Take a look at the chart below, which shows President Obama’s second-term presidential cycle in comparison with 4-year presidential cycles from 1929 through 1940 and the presidential cycles from 1953 through 2012. The current cycle beats both of the historical trends.

To me, the chart indicates that investors who ignore the negative headlines and focus on the strength of the U.S. stock market are the ones who have been very profitable this year.

click to enlarge

When it comes to investing, what are you thankful for?

Index Summary

- Major market indices finished slightly higher this week. The Dow Jones Industrial Average rose 0.13 percent. The S&P 500 Stock Index gained 0.06 percent, while the Nasdaq Composite advanced 1.71 percent. The Russell 2000 small capitalization index rose 1.60 percent this week.

- The Hang Seng Composite rose 0.92 percent; Taiwan gained 3.57 percent while the KOSPI gained 1.93 percent. The 10-year Treasury bond yield gained 1 basis point this week to 2.75 percent.

All American Equity Fund - GBTFX • Holmes Growth Fund - ACBGX • MegaTrends Fund - MEGAX

Domestic Equity Market

The S&P 500 Index set another post-financial crisis high of 1,807 mid-week and finished the week slightly up by 0.06 percent. Positive economic data during the week offset concerns about taper-timing of the Federal Reserve’s stimulus program, as weekly jobless claims fell to the lowest level since September and the LEI Index came in better-than-expected. To date, the S&P 500 is up over 160 percent since the market bottomed in March of 2009 at the depths of the financial crisis.

click to enlarge

Strengths

- Tech stocks were the strongest sector this week led by the hardware and equipment group. The top performer in the S&P 500 was JC Penney, as news that the CEO purchased $1 million of its shares helped boost sentiment on the stock.

- Consumer discretionary stocks were also notable performers, led by luxury brands such as Tiffany & Co which posted strong third-quarter earnings as well as Coach.

- Industrial sector stocks took a breather this week and finished flat. Stronger performers included Nielsen Holdings, Textron and Ingersoll-Rand, led by a better-than-expected LEI index report for October.

Weaknesses

- The energy and utilities sectors were among the worst performers as crude oil prices fell about $2 per barrel to a multi-month low of $92.78.

- The materials sector also fell more than 1 percent as investors booked profits in strong second-half year performers Freeport McMoRan and Cliff Natural Resources.

- ADT Corp was the worst performer in the S&P 500 this week falling 7.84 percent. The home security provider announced that its third largest shareholder, Corvex Management LP, would sell its stake in the company and that Corvex’s founder Keith Meister had resigned from ADT’s board of directors.

Opportunities

- The current macro environment remains positive as economic data remains robust enough to give investors confidence in an economic recovery, but not too strong as to force the Fed to change course in the near term.

- Money flows are likely to find their way into domestic U.S. equities and out of bonds and emerging markets.

- The improving macro backdrop out of Europe and China could be the catalyst for a rally into year end.

Threats

- A market consolidation could occur in the near term after such a strong year.

- Higher interest rates are a threat for the whole economy. The Fed must walk a fine line and the potential for policy error is potentially large.

- The debt ceiling and government shutdown have passed, but the economic fallout will likely be felt over the next weeks and months as it negatively affects upcoming economic data releases.

The Economy and Bond Market

Treasury bond yields rose by 1 basis point this week as economic data came in better-than-expected, further encouraging outflows from fixed-income securities into the broader equity market.

click to enlarge

Strengths

- Chicago’s Purchasing Manager Index for October was reported at 63.0, ahead of expectations of 60 and firmly in expansionary mode.

- Initial jobless claims fell by 7,000 last week to a seasonally adjusted 316,000, the lowest level since late September. Analysts were expecting jobless claims to fall to 330,000.

- The S&P/Case-Shiller Composite 20 Home Price Index for September was 165.66, the highest level in five years, and up 13.29 percent year-over-year.

Weaknesses

- The November Consumer Confidence Index came in at 70.4, below survey consensus and below the prior month print.

- Durable goods orders (ex-transportation) for October declined by -0.1 percent, below expectations of growth of 0.5 percent, and in line with the prior month.

- Pending home sales fell for a fifth straight month, dipping 0.6 percent in October, per the National Association of Realtors which said that the recent government shutdown, rising interest rates, and rising home prices all contributed to the decline.

Opportunities

- Despite recent conflicting commentary, the Fed continues to remain committed to an overall accommodative policy and is unlikely to raise interest rates in 2013 or 2014.

- Key global central bankers remain in easing mode, including the European Central Bank (ECB), Bank of England and the Bank of Japan. An ECB policymaker commented this week that the ECB could adopt negative interest rates or quantitative easing to lift inflation.

- There remain many moving parts to the taper decision and it is very possible that tapering could be delayed well into 2014.

Threats

- Inflation in some corners of the globe is getting the attention of policymakers and may be an early indicator for the rest of the world.

- Trade and/or currency “wars” cannot be ruled out which may cause unintended consequences and volatility in the financial markets.

- The recent bond market selloff may be a “shot across the bow” as the markets reassess the changing macro dynamics.

Gold Market

For the week, spot gold closed at $1,251.39, up $7.76 per ounce, or 0.62 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, were off 0.31 percent. The U.S. Trade-Weighted Dollar Index lost 0.06 percent for the week.

Strengths

- China’s net imports of gold from Hong Kong climbed to the second-highest level on record in October as jewelers and retailers bought the metal to build up inventories ahead of a peak-demand season at the end of the year. A total net purchase of 131 tonnes in the month, nearly 20 percent above the 111 tonnes in September, is only slightly lower than the record of 136 tonnes of net imports registered in March 2013. Back in the second quarter, the market dismissed the surge in Chinese purchases of physical gold as purely speculative and one-time, mainly attributable to the sharp decline in the gold price. However, as seen in recent macro data, the appetite for gold from China has proved to be both remarkable and persistent. The much touted ETF liquidations that helped bring gold prices down to the $1,200 level have been absorbed entirely by China. Gold refineries in Switzerland have been busy converting the 400-ounce bullion bars, typically owned by ETFs, into one kilogram bars preferred by Chinese jewelry makers and gold investors.

- Chow Tai Fook Jewellery Group Ltd., the world’s largest listed jewelry chain, forecasted steady growth for the rest of the fiscal year after first-half profits almost doubled on a surge in Chinese demand for gold. Net income rose to HK$3.5 billion and was above the average estimate of HK$2.98 billion from five analysts compiled by Bloomberg. The company said it opened 118 new points of sale, which includes standalone stores and concessionaire counters, taking the total to 1,954 as of the end of September. Not surprisingly, Tiffany & Co., the world’s second-largest jewelry retailer, delivered blowout earnings this week, mostly due to international growth, where the Asia Pacific region had sales growth of 27 percent. Investors should remember that roughly 50 percent of the global demand for gold is fueled by the “Love Trade,” and evidenced by the success of these two retailers.

- Enthusiasm with the broader equity markets in the United States is getting fairly toppy. The spread between the bull and the bear camps in the Investor Intelligence poll recently widened to 41.4 percentage points. The last time it was this high was in April 2011 and returns seen three to six months later were close to 15 percent lower. In addition, margin debt is now at an all time record of $412 billion, up 30 percent from a year ago. From a contrarian standpoint, when returns have come too easy relative to fundamentals, courtesy of the Federal Reserve, one should read the present tape as “time to take some money off the table and buy what has been written off,” such as gold in the current environment. Plain and simple asset allocation, sell high and buy low, is a prudent plan to grow your wealth.

Weaknesses

- Gross speculative short positions on the COMEX have doubled in the past three weeks to 82,842 contracts. According to David Rosenberg of Gluskin Sheff, this is only the fifth time that this has happened in the past decade, which as a strong contrarian indicator sets up the gold market for a nice countertrend rally. The biggest factor weighing on the market is a resumption of selling by ETFs. ETF holdings stabilized during the summer, but have since resumed, with investors having liquidated 1 million ounces over the past month, with 600,000 ounces of that coming over the past week. The renewed decline in ETF holdings suggests that weak hands haven’t completely exited the market.

- Waterton Global Mining laid off 182 employees at its Nevada operations, as the company’s Hollister Mine and Esmeralda Mill commence the next phase of its “value creation plan.” Waterton is going to concentrate on drilling and resource definition in the near term as the company believes it provides the best long-term value and sustainability. Similarly to Hollister, Ryan Gold Corp. announced the shutdown of its Yukon operations given the generally poor market conditions for exploration companies. The company will conserve its cash and cease exploration activities. Despite having funds to proceed, it appears both these companies are not going to attempt to “swim against a fast moving river” any longer. This news marks the proverbial “tap-out” sign or surrender flag for two juniors, which continue to piece together signs of a market bottom.

- Detour Gold, the worst performing stock in the Toronto Stock Exchange this year, sank to the lowest close since December 2008 on news that Chief Executive Officer Gerald Panneton resigned without providing a reason. He will be replaced by Paul Martin, the chief financial officer, on an interim basis. Detour Gold has plunged 86 percent this year with the market dismissing Mr. Panneton’s assurances that Detour did not need to raise more capital. It is very likely Detour will come back for additional funding through the ramp-up period, with the downside risks to equity holders remaining very high and not necessarily fully priced in.

Opportunities

click to enlarge

- According to Dr. Martin Murenbeeld, Dundee’s Chief Economist, if we were to summarize gold market developments for 2013 to date the first concept that would come to mind would be that of a great rotation out of debt and into equity. What has actually happened is a great rotation out of gold and into equity instead. The chart above compares the gold price and the S&P500, showing that the correlation between the two is about as negative as it has ever been. The most curious part is that gold has declined in the face of exponential growth of global liquidity. The negative correlation of gold is much higher with the S&P 500, than with the U.S. dollar for example, which suggests the S&P 500 is driving the gold complex. The chart shows that gold is now -2.4 standard deviations below the S&P 500, an oversold level that on purely statistical terms, has to trigger a correction in the near to medium term.

- Gold producers’ price-to-cash-flow multiples remain near the lowest in at least a decade, according to a recent Bloomberg study. Even after a mild bounce during the third quarter, the multiples are well below one standard deviation from the historical average. Not only have the multiples tumbled, but so have the consensus cash flow projections made by analysts, which have declined more than 50 percent from the first quarter of 2012. The resulting cratering of stock prices has many investors completely abandon the sector. However, the fact that cash flow multiples, which tend to be fairly consistent, are sitting at oversold levels bodes well for a bottom in gold stocks.

- Throughout this year, the Indian government increased import duties on gold and silver three times in a bid to protect the currency from a widening current account deficit. The All India Gems and Jewellery Federation has finally stepped up and appealed to the government to roll back the import duty from 15 percent to 5 percent. The abrupt and arbitrary rulings are threatening jewelers by making it very difficult to access the much needed gold and silver. The import curbs force jewelers to pay a record $200 per ounce premium over the London price from next month to obtain supplies, according to the All India Gems & Jewellery Trade Federation. The premium is currently at near record $120-$130 an ounce. As a result, Mumbai-based Tara Jewels said that it will close some of its less profitable gold-led stores to adapt to the current regulatory environment.

Threats

- Goldman Sachs is set to swap $1.68 billion in cash with the Venezuelan central bank, to be backed by $1.85 billion of the nation’s gold reserves. The terms of the loan dictate the South American government will pay 7.5 percent plus three month LIBOR over seven years, with Goldman Sachs holding the gold in a margin account. Speculation has been rampant after some details of the story were leaked to the press, with some analysts calling the transaction a classic, non-transparent emerging market transaction where deduction is necessary to guesstimate where the story is going. In our view, the gold provided by Venezuela to Goldman Sachs will create another source upon which the bank can write and sell massive paper gold bets on, increasing the already speculative paper gold market, and continuing to disturb the well-earned reputation of physical gold.

- The daily gold fix in London, the benchmark used by miners, jewelers and central banks to trade the yellow metal, is being scrutinized amid speculation there could be superior knowledge by those involved in the fixing. Tradition calls for five banks to meet, from a few minutes to an hour, to set the price of gold twice a day. However, unnamed traders who have been involved in the process, as well as other dealers and economists argue that knowledge gleaned from the calls could potentially give traders an unfair advantage in the market. Although there is no concrete evidence of wrongdoing, both academics and economists concur in that the system is outdated and vulnerable to abuse, especially considering gold trading is a $20 trillion market.

- Turquoise Hill Resources has filed its final prospectus for the $2.4 billion rights issue. Rights have been priced at $2.40 per share, a 42 percent discount to the November 25 close price of $4.16 per share. The rights issue is a one-for-one, resulting in 1,006 million new shares being issued. The analysts at BMO Research calculate that the issuance will cause existing shareholders who forgo their rights, a theoretical 21 percent dilutionary effect. Despite the numerous dilutions, the highly attractive underground development would be well capitalized, thereby reducing financial risk. Political risk remains a concern and is reflected in the relatively attractive post rights price to net present value (P/NPV) multiple of 0.6x; Turquoise Hill provided no further update regarding its ongoing discussions with the Mongolian Government.

Energy and Natural Resources Market

Strengths

- Natural gas futures climbed over 4 percent this week to the highest level in five months nearing $3.83 per million British thermal units (mmbtu). Cold weather across much of the country boosted heating demand.

- Gold bullion closed up this week by nearly $10 per ounce as the U.S. dollar index weakened to a three-week low.

Weaknesses

- Crude oil futures slid 1 percent this week as an interim agreement with Iran regarding its nuclear program diffused geopolitical risk and raised the possibility of Iranian supply coming back to the market in the future.

- Aluminum prices closed at a four-year low of $0.80 per pound this week on signs that global supply will outpace demand in an already well-supplied market.

Opportunities

- In a move designed to combat overcapacity in the steel sector, China will relocate some factories and encourage more companies to invest in overseas projects, said an official with the country's top planning agency. Li Zhongjuan, an inspector of industrial planning for the National Development and Reform Commission (NDRC), said the country will continue to optimize the steel sector through industrial transfers and directing capacity to areas with comparative advantages. In the meantime, the NDRC will ratchet back new projects and take on existing, outdated production through legal and market-oriented means, Li said at a recent conference of the China Iron and Steel Association.

click to enlarge

- The fastest growth ever within U.S. crude output will mean a supply glut as soon as 2015, spurring the industry to challenge a 38 year ban on most exports. Refineries in the Gulf Coast, East Coast and Canada can handle another 1.75 million barrels a day before becoming saturated in the first half of 2015, causing domestic prices to fall relative to international grades. The U.S. will have to expand plants, curb output or allow exports, according to Washington-based PFC Energy, a consulting unit of research company IHS Inc. Most of the growth in the U.S., poised to become the world’s largest producer by 2015, is in lighter grades extracted from shale rock formations. Many refineries are configured for heavier crudes from the Middle East and Latin America. That mismatch is creating a surplus of domestic supply with nowhere to go, raising pressure to ship oil overseas. The industry’s push to export will face resista nce from members of Congress concerned that gasoline prices would rise. Senator Ron Wyden, an Oregon Democrat who chairs the Energy and Natural Resources Committee, would need to see benefits to consumers before supporting such a move, spokesman Keith Chu wrote in a November 6 email.

- For decades, governments dreamed of harnessing the Congo river's enormous energy at the Inga rapids with an expansion of the dam large enough to power half of Africa. Years of conflict and misrule in the Congo meant the project was never realized. Instead, in the cavernous halls of Inga's two dams, water drips from the ceiling and rusted pipes sit above puddles. Five of the 14 turbines no longer spin at all, a sign of the decay. Now a deal with South Africa to buy electricity from Inga has revived talk of the giant hydro project that could illuminate a continent whose economies are rapidly expanding but lack the power supply to sustain it. "We had to find a buyer for this energy. Otherwise we cannot build Inga," Bruno Kapandji, Congo's minister of energy and hydro power, told Reuters. "South Africa is a solvent and credible buyer," he continued. Following a year of talks, South Africa has promised to buy at least half the electrici ty from Inga III, a $12 billion dam that, once built, will produce 4,800 mega watts (MW) of energy. Much of the rest may go to the Congo’s power-starved mining industry. This is nearly three times the amount produced from Inga's two existing dams, which are decades old and have been crippled by neglect, government debt and risk-averse investors. Success for Inga III would help to raise investors' confidence in the remaining five stages of the Grand Inga project. At an estimated cost of $50 to $80 billion, Grand Inga would produce 44,000MW, dwarfing all other hydro-electric projects in the world, including China's Three Gorges Dam. "This incredible feat of human ingenuity, when completed, will have the capacity to power Africa and indeed to export electricity beyond the continent," South African President Jacob Zuma said at a signing ceremony in Kinshasa.

Threats

- The Las Angeles Times reports, “India is now the world's third-largest grain producer after China and the United States.” The adoption of higher-yielding crop varieties and the spread of irrigation have led to this remarkable tripling of output since the early 1960s. Unfortunately, a growing share of the water that irrigates three-fifths of India's grain harvest is coming from wells that are starting to go dry. This sets the stage for a major disruption in food supplies for India's growing population. In recent years, about 27 million wells have been drilled, chasing water tables downward in every Indian state. Farmers can also reduce water use by using more efficient irrigation techniques and by growing less thirsty crops. For example, more wheat and less rice.

- The Financial Times reported, “King Coal has lost its crown. Since prices spiked in the wake of the Australian floods of 2010 it has been all one way for thermal coal – down. But a rally in several coal benchmarks has brought the market back to life and raised hopes the fossil fuel, which is used to generate electricity around the world, might have bottomed. The Australian spot price has risen almost 9 per cent since its August low to $82.80 a tonne, while its South African equivalent is nearly 17 percent higher at $83.39. Yet the outlook for thermal coal remains poor. Supply continues to expand, with producers in Australia and Indonesia, the world’s biggest exporter, still to curtail output in the face of weaker prices.” One industry executive says, “There’s good demand everywhere, but there is just too much supply.” An unusually cold winter in the northern hemisphere and fu rther disruptions in Colombia, which exports almost 70 percent of coal to Europe, could help support thermal coal. Most analysts expect prices to come under pressure in 2014, especially if demand from China weakens.

- The latest SteelBenchmarker assessment by World Steel Dynamics shows that the disparity in global steel prices continues to grow. U.S. domestic hot rolled coil (HRC) prices have risen to $736 per ton ($736/t), the highest since May 2012, and following domestic scrap prices upwards. In contrast, European hot rolled coil prices have slipped $10/t over the past fortnight, and remain well below levels seen in the first quarter this year, while Chinese domestic HRC prices also slipped to only $3/t over the low over the past 12 months. U.S. domestic prices are now trading at a $260/t premium to Chinese prices and a $177/t premium to the benchmark World Export price. According to Macquarie research, such arbitrages have proven unsustainable in the past, and seen substantial increases in U.S. steel import volumes.

|

|

||

|

|

|

|

|

|

||

![[thumb]](/images/content_image/data/50/50b18d1726a2f3422cf4acdd0f3b1683.jpg)

![[thumb]](/images/content_image/data/66/66be506c2df418238c74102446cfdced.jpg)

![[thumb]](/images/content_image/data/20/209b602b657eb2beb45c00560ec5a9e2.jpg)

Emerging Markets

Strengths

- Brokerage firms were positively surprised by the scope and tone of the recently proposed reforms by China’s government. While implementation is crucial and will take time, they believe that the prospect of reform will drive a re-rating of the Chinese equity market, narrowing the valuation gap versus the rest of the region. They recommend overweighting in Chinese H shares and A shares.

- China’s October profits at major industrial companies increased 15.1 percent year-over-year, down from 18.4 percent in September, according to the NBS. The deceleration is mainly due to a higher comparison base as industrial profit growth recovered in third-quarter 2012. In year-to-date terms, profits rose 13.7 percent in the first 10 months compared with 13.5 percent in the first nine months.

- China’s health care industry sales grew 19.9 percent year-over-year in October, up from 18.1 percent in September and 15.1 percent in October 2012. Industry profit was up 18.7 percent in October versus 17.8 in September 2013 and 14.3 percent in October 2012.

- China is the largest online market. According to I-Research, China’s internet population surpassed that of the U.S. in 2006 and the number of smartphone users surpassed those in the U.S. in first half of 2013. Online sales have increased 19 times over the past five years. Online penetration rate reached 6.3 percent in 2012, already surpassing 5.1 percent in the U.S. About 33 percent of apparel, footwear and sportswear sales in China were online in 2012 versus 5 percent in 2008.

- Yingluck Shinawatra, the prime minister of Thailand, survived a no confidence vote. On the economic front, Bank of Thailand, the central bank, cut interest rates by 25 basis points to help the weakening economy. Thailand’s current account turned a surplus from a deficit in September, and private consumption index was flat versus a negative change in September, indicating the economy is stabilizing, though not out of woods yet.

- Korea industrial production (IP) growth rose in October to 3.0 percent year-over-year and 1.8 percent month-over-month in October after dipping 3.9 percent in September, disrupted by one-off factors such as the automakers’ strike and Chuseok holidays.

- European stocks climbed the most in almost two weeks as consumer confidence in Germany rose to a six-year high according to a GfK market survey. The research market group reported the mood among German households jumped to a higher-than-expected 7.4 points on the GfK scale, up from 7.1 points in the previous month. Analysts’ forecast for the period showed stagnation or a slight improvement at best. The GfK indicator is at its highest level since August 2007 coinciding with increases in German business climate and domestic demand as reported the prior week.

click to enlarge

- Hungary’s central bank announced its 16th-consecutive benchmark rate reduction. The Monetary Council weighed the outlook for consumer prices, and remains supportive for further easing, even after policy makers lowered the benchmark rate by 20 basis points to 3.2 percent. The inflation rate fell to 0.9 percent in October, the lowest since 1974, and has remained below the central bank’s 3.0 percent target since February. The possibility of further reductions was made more likely when the European Central Bank (ECB) cut its benchmark rate on November 7 amid deflation risk.

Weaknesses

- Hong Kong’s October retail sales value was up 6.3 percent year-over-year versus consensus for 7.3 percent, the fourth-consecutive month to see single-digit growth. Luxury goods sales were 16.8 percent, while clothing and department store products were 10 percent.

- In October, Thailand’s trade deficit was widened to $1.8 billion after a $0.5 billion surplus in September, while exports showed 0.7 percent contraction year-over-year versus 7.1 percent contraction in September. Imports were down 5.4 percent in October versus down 5.2 percent in September. Thailand’s industrial production contracted 0.1 percent in October from September. Thailand’s auto sales were also down which forced the auto production utility rate to drop 12.4 points since November 2012 which may revert to the upside if auto exports pick up momentum.

- Foreigners were still net sellers throughout the week ($95.6 million) in the Philippines, and they have been net sellers in 17 of the 19 total trading days in November. Top names sold by foreigners this week were fundamentally healthy companies. The Philippines’ third-quarter GDP growth slowed to 7 percent from 7.6 percent in the second quarter.

- An HSBC report shows October’s monthly equity inflows are concentrated in developed market equity funds, with minimal flows to emerging market funds. Total equity inflows hit a nine-month high, but were mainly directed to developed market equity funds, reiterating this year’s trend. Despite a second consecutive week of inflows, appetite for emerging market equity funds remained low. Positioning data across the emerging market universe shows that, in spite of mild inflows, fund managers cut their exposure to overall emerging markets in their global portfolio to 7.3 percent, the lowest since August 2009.

- South Africa’s gross domestic product rose an annualized 0.7 percent in the three months through September, down from a revised 3.2 percent in the previous quarter. Africa’s largest economy is ailing after strikes demanding above-inflation wage increases in mining, construction and car manufacturing this year disrupted output, leaving economic growth on course to expand at the slowest pace since the 2009 recession.

Opportunities

click to enlarge

- As shown in the chart above, the market share of online sales in China is rising quickly, accounting for nearly 9 percent of China’s retail sales now and still growing 50-60 percent per year. Taobao and Tmall’s online shopping platform recorded 35 billion renminbi in sales on November 11 2013, the so-called Single’s Day, representing 40 percent of national total retail sales on that day. Tencent’s Wechat attracts 500 million users to chat via mobile phone, capping the growth of voice calls and text messages to low-single-digits. The online platforms of Alibaba and Baidu take depositors less than 10 mouse clicks to buy a monetary fund product with a 4.5 percent annualized return.

- The European recovery has proved a tailwind to Dow Jones sales growth; at least one-third of the companies in the Dow Jones Industrial Average (DJIA) reported revenue growth numbers from their European customers in the third quarter. During the previous quarter, only one-tenth of the companies in the industrials index reported revenue growth in Europe. This last quarter was also the highest number of DJIA companies to report sales growth in Europe since the fourth quarter of 2011, according to Scott Gooch of Jefferies. The results show the European recovery is gaining momentum which should benefit its main trading partners in Eastern Europe.

- China's premier, Li Keqiang, announced the reaching of an agreement with Hungary and Serbia to assist in building a railway between the two Eastern European countries. The project is set to jumpstart greater cooperation between China and Central and Eastern European countries. China, which now boasts the world's second-largest railway network and the longest mileage of high-speed rail tracks, can assist in the needs of Central and Eastern European countries for modern transportation and infrastructure.

Threats

© US Global Investors

- Indonesia fell short of its goal at the debut domestic dollar bond sale, indicating onshore liquidity is tight.

- Brazilian President Dilma Rousseff is expected to oppose Petrobras’ proposed fuel pricing formula, arguing it will impact gasoline prices and increase inflation. Petrobras currently sells fuel domestically at a sizeable discount to international market prices. The Presidential Palace also voiced concern over the proposed formula becoming a pricing reference for other regulated sectors, while it pondered if the process would take pricing and timing control from government hands. Backstage, presidential aides have commented the formula proposed by the board of Petrobras has been discarded. The effort now is to find a middle ground that allows for the company to increase prices closer to market prices, and increases the pricing predictability for financial planning purposes, while ensuring the executive retains some autonomy over the decision of future adjustments.

- The Russian ruble weakened to its lowest in more than four years on the back of corporate demand for foreign currency to meet debt payments. Russian companies are expected to pay back nearly $30 billion in principal of foreign debt in December, highlighting both the need for substantial amounts foreign currency, and the considerable leverage of Russian corporations. The ruble has been under pressure by consumer prices running at 6.3 percent, well above the central bank’s target.