For Whom the Nobel Tolls: Efficient Market or Irrational Exuberance?

In “The Importance of Being Different” (5/4/2013), I denigrated the “Efficient Market Hypothesis” advanced by University of Chicago Professor Eugene Fama. This may prove to have been a high point of my contrarian career, since the Royal Swedish Academy of Sciences just awarded Fama its prestigious Nobel Memorial Prize in Economic Science, to be shared with two other American professors: Yale’s Robert Shiller and the University of Chicago’s Lars Peter Hansen.

In all fairness, Fama was not the only famous economist to be victimized by my sarcasm. I also mentioned Nobel laureates Harry Markowitz and Paul Samuelson, and added, “While picking on Nobel Prize winners’ contributions to investment science, we should not forget that Long-Term Capital Management, a fleetingly famous hedge fund that in 1998 incurred losses so catastrophic as to require the intervention of the Federal Reserve, counted two Nobel laureates on its board.”

Some people argue that there simply should not be a Nobel Prize for economic science. In an August 24, 2013, opinion piece for The New York Times, two philosophy professors, Alex Rosenberg and Tyler Curtain, made the following points:

“It’s easy to understand why economics might be mistaken for science. It uses quantitative expression in mathematics and the succinct statement of its theories in axioms and derived “theorems,” so economics looks a lot like the models of science we are familiar with from physics.” But, “The trouble with economics is that it lacks the most important of science’s characteristics – a record of improvement in predictive range and accuracy” (my italics).

My more simplistic view is that successful investment is less a function of knowledge than a function of common sense and of one’s ability to control overreactions and psychological biases. Alas, there has been no suggestion of a Nobel Prize for common sense or self-control.

Before I deal with the intended subject of this paper, which is the seeming paradox of professors Fama and Shiller’s sharing a Nobel Prize, I should apologize for knowing nothing about their co-laureate, Professor Lars Peter Hansen. A rushed effort to familiarize myself with his work was short-lived: First, Wikipedia introduced him as an “econometrician,” an instant put-off for me; then, I read on Google a description of his work and understood nothing. So, for now at least, I remain in the dark about Hansen’s achievements.

On the other hand, I am reasonably familiar with the works of Fama and Shiller, having read a number of their papers over the years.

Fama is one of the fathers of the Efficient Market Hypothesis, which holds that markets are “informationally efficient.” If, as the hypothesis assumes, investors immediately incorporate any newly available information into the price of an asset, the implication is that it is nearly impossible to “beat the market” (unless, of course, one has a special advantage such as inside, non-public information).

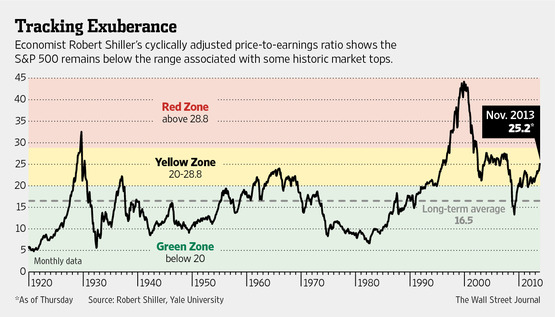

Shiller, at the opposite, believes that investors’ behavior is importantly influenced, if not primarily determined, by psychology. For example, he points out that stock prices fluctuate more than dividends (or corporate earnings), which should not happen if investors were fully rational. He concludes that markets are prone to “Irrational Exuberance,” the title of his best-selling book, and that a disciplined investor paying attention to value can, indeed, outperform the market.

Shiller’s views have been very publicly vindicated by his timely warnings of two bubbles before they burst: the stock market “tech” bubble in 2000 and the real-estate bubble in 2005. Since his views incorporate contrarian and value notions, I obviously lean toward them.

Fama’s work is better known by financial professionals than by the broad public, and it has been widely embraced by financial consultants and asset allocators. Yet, I have a problem with the idea implied in the Efficient Market Hypothesis: that it is impossible to lastingly beat the market. True, there is a large body of studies documenting that most investors do worse, not only than official indices but also than the average of the investment population. In fact, blaming “certain behavioral biases,” Daniel Kahneman, a psychologist but also another Nobel laureate in economics(!), said it plainly:

“Many individual investors lose consistently by trading, an achievement that a dart-throwing chimp could not match” (Thinking, Fast and Slow, Farrar, Strauss and Giroux, 2011).

I am not a statistician, but it seems to me that if a majority of investors fails to approach even average returns, then a few must be doing quite a bit better. In fact, this all along has been the argument of Warren Buffett and several other lastingly successful investors.

When Fama’s and Shiller’s nominations were announced, a number of observers clearly had some difficulty refraining from giggling. Paul De Grauwe, professor at the London School of Economics, tweeted, “Nobel Prize for Fama who led millions to believe financial markets are efficient and for Shiller who showed the opposite. What a contradiction.”

But there may be less of a contradiction here than meets the eye.

First of all, besides his work on the Efficient Market Hypothesis, Fama has done extensive research with Dartmouth Professor Kenneth French on the returns from stocks with different characteristics of value, growth, past performance, etc. In the process, the two have created an extensive database regularly used by many other researchers as well.

Their studies evidenced a number of “anomalies” that would not occur if the markets were totally efficient. The first and most striking one was the existence of a momentum factor: Stocks that have been doing well have a tendency to continue to do well – at least for a while. But then, the two professors further observed that the stocks of small-capitalization companies had a tendency to outperform those of larger companies, and that “value” stocks with a low price-to-book ratio outperformed stocks with a high price-to-book ratio.

To Professor Fama’s credit, he published these results even though they seemed to contradict his hypothesis of an efficient market. Together with his colleague, he even developed the “Fama and French Three Factor Model.” Traditional portfolio analysis has mainly been concerned with assessing future market volatility and how individual stocks or portfolios would be influenced by overall market behavior. The Fama and French model added value and size considerations that could help in allocating portfolios to different categories of stocks.

Disappointingly, however, Fama seems to have held to his Efficient Market Hypothesis and continued to treat the compelling results used in the Fama and French model as anomalies that might be due to the greater riskiness of the outperformers.

If the logical conclusion of the Efficient Market Hypothesis is that it is impossible to guess where the market is going next, and generally which asset might outperform it, investors might as well buy an index fund. In fact, many investors of note recommend that approach for small, individual investors. But the “anomalies” uncovered by Fama and French do exist, and a serious investor may desire to take advantage of them. As often happens in investing, which ones are most promising depends on the time frame considered.

Reviewing some of the literature on momentum investing, for example, Travis Morien, an Australian financial adviser, notes in his blog that momentum is relatively short-lived and does not seem to affect a stock’s performance beyond one year, if that long. The result, he observes, is that momentum investors frequently need a very high turnover in their portfolios to take advantage of the effect.

Even more to the point, most successful long-term investors, of both the growth and value persuasions, profess that buying a stock should be likened to the purchase of a whole company. Anybody remotely familiar with business knows that companies have to deal with multi-year cycles, and that management strategies, too, often take years to bear fruit. So momentum investing, which only looks months ahead, really is like jumping on a bandwagon hoping that the conductor knows where he is going. In fact, it could be argued that financial analysis is totally useless for momentum investors.

By contrast, David Dreman, a leading student and practitioner of contrarian investment strategies, notes that contrarian stocks, if purchased when they are deeply oversold (a timing challenge, as we will see), outperform the market for an extended period of time – frequently several years.

Fama and French, as well as other researchers, have clearly identified a number of characteristics that, over time, have been demonstrated statistically to produce superior returns from the stocks sharing them. This is where approaches like their Three Factor Model become interesting. If you combined several of these selection criteria into a screen designed to identify stocks attractive for purchase, you would expect to raise your odds of success. However, early in my career I experimented with (rudimentary) computer screens and the results were discouraging.

Let’s say we screen for stocks with low price/earnings (P/E) ratios; as a group, the cheapest ones tend to outperform the whole sample over time. But there is what I would call a “sample effect”: The “cheapest” decile of a 5,000-company universe would contain 500 companies with the lowest P/E ratios, for example. Presumably, a number of these companies would be cheap for a reason and would go out of business within a few years. On those, you would lose 100 percent of your investment. But the stocks of companies that were on the verge of bankruptcy but survived might appreciate 200-300 percent or more. As a result, the whole 500-company category would probably yield a well-above-average return.

The problem with following this approach is that, besides the resulting feeling of playing roulette with one’s portfolio, a 500-stock portfolio is impractical to buy, own, and monitor. One way to reduce the sample size is to eliminate stocks with P/E ratios in excess of 8 instead of 10. But the more you lowered the P/E ratio, the greater the proportion would be of selected companies that had serious problems not identifiable in a screen. So, in my early tests, I experimented with “qualitative screens”: debt, liquidity, and profitability ratios intended to keep only companies likely to survive. Then, the number of selected companies shrank dramatically; but unfortunately, many of those that remained had problems that could not be screened out but became quickly apparent upon closer investigation.

In summary, a multi-factor model seemed to work, albeit with a level of casualties, as long as it remained quantitative (size, valuation, etc.). But there seemed to be no easy way of refining it with qualitative criteria. This is not entirely satisfying for fundamental investors who need to feel “in control” of their portfolios.

I should mention a working paper written in May 1993 by Josef Lakonishok et al. for the National Bureau of Economic Research: “Contrarian Investment, Extrapolation and Risk.” The three professors investigated a number of screening criteria, including companies’ growth in sales over the five years prior to the formation of the samples. Paradoxically, stocks of companies with the slowest past sales growth significantly outperformed the stocks of companies with the fastest past sales growth, and this was true for each of the ensuing five years. If nothing else, this illustrates the role of investors’ expectations (as influenced by past results and measured by current valuations) on future investment returns, which brings us back to Shiller’s work.

The problem with Shiller’s psychological/value approach is that it does not help determine precisely when a bubble has reached the bursting point. Because of crowd psychology and the way in which investment fads and fashions feed on themselves, value criteria alone are not great market-timing tools. A grossly overvalued stock can always rise some more before collapsing, and a very cheap stock can always decline some more before rebounding.

In fact, on 1/25/2013, Shiller himself stressed in a Business Insider interview that, while CAPE (the Cyclically Adjusted Price Earnings ratio) has a pretty good fit with subsequent 10-year returns from stocks, it is not a timing mechanism:

“It doesn’t tell you [to] wait until it goes all the way down to a P/E of 7, or something…The important thing is that you never get completely in or completely out of stocks. The lower CAPE is, as it gradually gets lower, you gradually move more and more in.”

Famed economist John Maynard Keynes, who was either a highly successful investor or a very poor one depending on the period analyzed, reportedly put it this way: “The market can stay irrational longer than you can stay solvent.” Unfortunately, as he reminded investors, “In the long run we are all dead.”

In the end, the Nobel Academy described quite well the rationale for awarding a joint prize: “There is no way to predict the price of stocks and bonds over the next few days or weeks. But it is quite possible to foresee the broad course of these prices over long periods, such as the next three to five years. These findings…were made and analyzed by this year’s Laureates.”

François Sicart (in Paris)

Disclosure: This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized.

© Tocqueville Asset Management