Two things have marked 2013 as an extraordinary year for U.S. stocks: big gains and an exceptionally smooth ride. Recently investors have been worried about the former, i.e.is the market in a bubble. In my opinion, the bigger risk, at least in the near term is the latter:low volatility.

Year-to-date, market volatility (measured usingimplied volatilitybased onthe VIX) is around 14, compared to historical average of around 19. More recently the VIX Index has dropped as low as 12, approaching the multi-year lows seen in March and August.

To be sure, at least some of the drop in volatility is probably justified. In the past, market volatility has typically been driven by a number of factors: past volatility,market momentum, and credit market conditions. Most of these factors suggest that equity market volatility should be somewhat lower than normal:

- Market momentum has been exceptionally strong this year. By the end of October, the12-month trailinggain for the S&P 500 was 25%.

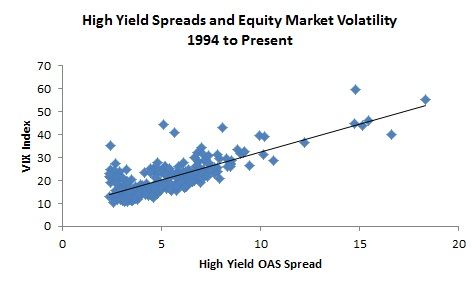

- Low equity market volatility is normally associated with easy credit market conditions. As spreads get tighter, indicating easier credit market conditions, volatility typically declines. The 20-year correlation between the VIX and high yield spreads is nearly 80%. As the chart below shows, a rough rule of thumb is that for every 100 basis point (bps) tightening in high yield spreads, the VIX typically drops by around 2.5 bps.

Source: Bloomberg

The problem today is that even after accounting for strong momentum and benign credit conditions,volatility looks unjustifiably low. In addition, there are other, less benign factors that investors may be ignoring.

The most important one may be what’s going on in Washington. Historically, when political and policy uncertainty is elevated, volatility has been higher. Today’s low volatility seems to be implicitly suggesting that Washington will arrive at another last-minute deal when the budget skirmishes resume in January. Even if that proves to be correct, investors may be paying insufficient attention to another factor that could keep political uncertainty high: the fallout fromthe Affordable Care Act (ACA). Continuing problems associated with the rollout of ACA risk keeping policy uncertainty elevated and undermining consumer confidence, and by extension growth.

Low volatility has a way of persisting, until it doesn’t. In other words, volatility is likely to stay low until something jars investors out of their complacency. When exactly that will happen is unclear, but for investors there are a couple of things to consider.

More tactical oriented investors may want to consider strategies that allow them to “buy volatility,” potentially profiting from a possible spike. Everyone else may want to consider trimming their equity exposure or at leastwaiting for a better entry point before putting new money to work. This is because, while I continue to believe thatstocks will be higher a year from now, with volatility so low, there’s likely to eventually be another spike.

Source: Bloomberg

© iShares Blog