Recently, I spoke on a panel regarding the State of Illinois (our panel literally “Under the Spotlight”). Our panel touched on many topics affecting the State but, when all was said and done, it seemed that the panel uniformly recognized that Illinois needed to do something about their pension problem (we had an interesting discussion about one party rule and speculated as to why they can’t seem to get anything done on pension reform – can you say re-election). As regular readers know, we have written on the subject on several occasions as we track pension data for over 900 plans across the 50 States and for all cities with populations greater than 100,000.

Let’s start with a baseline fact that 22 States have a Funded Ratio of less than 70% and 11 States have a Funded Ratio of less than 60% (mind you, that doesn’t cover the Commonwealth of Puerto Rico sporting a funded ratio of just under 9%). For the sake of ensuring Illinois does not feel picked on and to let you know this is not about Illinois, I offer our bottom dwellers (which include Lumesis’ home State of Connecticut) and move forward.

|

Illinois |

40.37% |

|

Indiana |

42.53% |

|

Kentucky |

46.77% |

|

Connecticut |

49.08% |

|

Louisiana |

55.86% |

Lumesis Data Team, State CAFRS

My point is not to highlight an issue which you have undoubtedly heard of, but to take this issue to the next level. Thomas Donlan recently authored an article, “Risky Rates”, in which he explored some of Detroit’s problems and cited the fact that Detroit’s advisors had forecasted the city’s pension investments could earn 8% per annum over the next 40 years. New actuaries were hired and reduced the estimated investment return to 7% (which is, according to the National Association of State Retirement Administrators, below the 7.75% average). Still, Detroit’s pension problem was big enough to be one of the factors that drove it to file for bankruptcy.

The rate of return on a blend of nearly risk-free Treasuries is about 4% and, as many know, Moody’s suggested corporate-bond rate is 5.5%. So, here is a math estimate, as presented by Donlan when looking at the funded/unfunded issue, for you to ponder: if one were to reduce the expected rate of return from 8% to 5.5%, the Funded Ratio would decline by about 30% and the Annual Required Contribution would almost double.

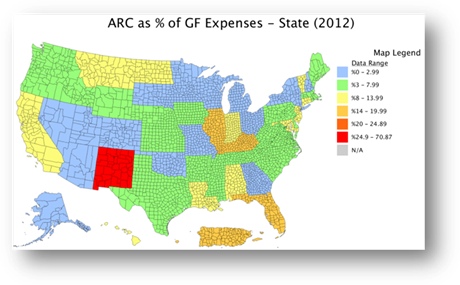

The below map shows the Annual Required Contribution as a Percent of General Fund Expenses for 2012. Contemplate, if you will, a scenario where that percentage doubles. What services would need to be cut or curbed, or how much would revenue need to increase?

DIVER Analytics, Map Module, State CAFRs

An alternative to address this problem just might be raising taxes. Politics aside – really – I offer some sobering data from the Treasury Department reported on in Thursday’s WSJ, “More Taxpayers Are Abandoning the U.S.” (and it’s not just Tina Turner, yes, Tina renounced her US citizenship last week). According to the article, year to date, 2,369 people renounced their citizenship or turned in their green cards compared to 1,781 for all of 2011. Citing an immigration specialist, the article noted that “[n]othing has changed in immigration law that would make people want to renounce… Current or anticipated changes in tax law and enforcement are driving this increase.” To the extent a solution to the pension woes (or other indebtedness) involves further tax increases, one must consider mobility (State to State or otherwise), especially amongst those that can afford to (usually the wealthy who are taxed at higher rates). Why? Because there is zero appetite (rightly so) to increase taxes on the middle class.

How about asking Uncle Sam for more dough (after all, the Fed does have its printing presses working full-time). Back to the conference -- not my panel but one where a State (Michigan) and city official (Philadelphia) expressed differing thoughts around reliance on the Federal government with the city expressing less of a level of reliance. Recall that a committee of our elected officials have until mid-December to present a way forward around the budget, deficit reduction, etc. We have been forewarned not to expect any grand deal – what a surprise. Absent something meaningful, we face the prospect of living with the Sequester or some other fate (although we have been promised no further government shutdown – I did hear reports that the shutdown actually led to a deficit reduction despite paying Federal employees not to work). Why am I going here? Because Michigan is not the only State that has a healthy level of reliance on Washington – not just for dollars but for some level of stability in the capital markets.

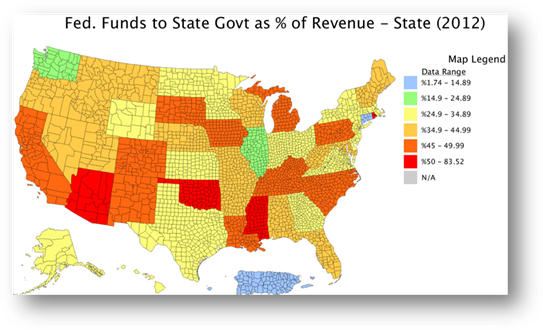

On the former point, how reliant are State governments on the Federal government for revenue? On average, over 38% (I include our definition in the below footnote for complete transparency).

Why should we care? Ask the guy from Michigan!

Damn It Janet

Turning back to the panel on which I spoke. I had suggested to our moderator and any others who were listening that the real need (after pension reform) was to find a catalyst to support economic growth – you know, something to drive job and wage growth. To this end, I turn to the confirmation hearings underway in our nation’s capital for the new Fed Chair and a dinner conversation with a close friend.

It seems to be a foregone conclusion that Janet Yellin will be our next Fed Chair and, at a minimum, she will continue many of the Fed’s current policies. For those that subscribe to the benefits of QE and low rates, the economy will “continue” its recovery (forget the current debate, even at the hearings, around Fed policies benefiting only the rich or those invested in the equity markets). If you subscribe to this view, then perhaps policy continuation will be the catalyst to support economic growth at the State and local level (although I have my sincere doubts and believe these doubts are supported by the marginal economic data we have seen over the past year plus – think job growth, labor force participation, wages, food stamp dependence, pension funded ratios, home values, etc.). In case you have missed some prior commentaries or do not have access to DIVER Analytics :

- Median Home Value for 2012 is lower than it was in 2009 in 32 States

- Job Growth for August 2012 (last data reported) was less than 1% in 28 States

- Labor Force declined between August 2012 and August 2011 in 21 States

Despite the data (just the facts), my dinner companion opined otherwise. “Damn it Janet” (name the film) was his cry as he extolled her to go further than Big Ben to stoke inflation. Why? Inflation (resulting from easy money) will help drive spending and lending which will help improve tax receipts at current tax rates. It will also, while interest rates stay low for as long as the eye can see, promote more folks to buy homes. The discussion ensued. For those that know me well, you may be surprised that I have a close friend with such views and that I would go so far as to have Friday night dinner with him. Diversity of perspective is important (we can’t watch the same news channel – CNN, MSNBC or Fox -- and expect to really know what is on) along with the fact that he is an outstanding connoisseur of wine.

In this regard, I certainly don’t profess to know the answer and have heard very intelligent (and some not so intelligent) people argue their points. The fact is that we do need a catalyst to promote growth.

Quick Update

Recently, the DIVER platform introduced a new Issuer Profile, a place to quickly access all information we have for virtually every municipal issuer. This Profile page will continue to be enhanced over the coming months. The DIVER Municipal Bond report (available for all 1.4+ million muni bonds) was also enhanced to include Hospital Obligor Data.

Off to Chicago and Cincinnati this week.

Have a great week.

Gregg L. Bienstock

CEO & Co-Founder, Lumesis, Inc.

Data Released Last Week:

- Property Tax Paid, Median (3 Year), County, 2010 - 2012

- Prop. Tax Paid as % of Home Value (3 Year), County, 2010 – 2012

- Median Home Value (3 Year), County, 2010 – 2012

- Weekly Initial and Continued Jobless Claims, State, 11/02/2013

- Foreclosures, State, County, Oct 2013

- Exports Total (Monthly), State, Sep 2013

Total Federal funds received directly from the Federal government as percent of the total revenue of the State primary government. Percentages are calculated using data reported by each State's CAFR, the NASBO State Expenditure Report, and the Recovery Act Transparency Board. US value is represented as the median of all states' Federal Funds as % of Revenue.

© Lumesis