The decision of the European Central Bank (ECB) last week to cut its main refinancing rate from 0.5% to 0.25% and the marginal lending facility from 1.00% to 0.75% is too little and too late -- and virtually irrelevant to financial markets. The decision came after published data showed the eurozone headline consumer price index slowing to 0.7% year-on-year in October. Of course the equity markets rallied temporarily in a knee-jerk reaction to the ECB’s move, but by the end of the day most of the gains were lost.

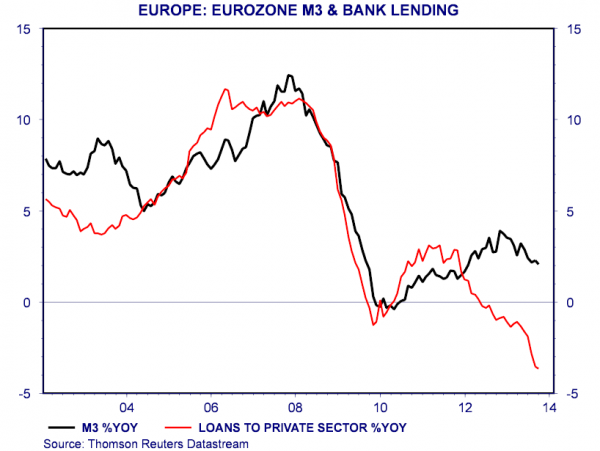

The problem is that if households and firms are not borrowing at current, already low rates, lowering them by one quarter is not likely to change their attitudes or behaviour. Amazingly, commentators still continue to refer to monetary conditions in the euro-area as easy or accommodative. This is based on the naive notion that if rates are low, money must be plentiful. But the reality is that broad money (M3) is growing at just 2.1% (in September) and bank loans are declining at a frightening -3.7% year-on-year. Interest rates are low, but money is tight. It is the demand for funds that has collapsed. In these circumstances, domestic spending is bound to be very weak, and the euro-area economy risks sliding inexorably towards deflation.

In contrast to the US Federal Reserve or the Bank of England, which have expanded their balance sheets by means of QE (or asset purchases) to offset the reluctance of commercial banks to expand lending and grow the money supply, the ECB has recently been allowing its balance sheet to shrink from EUR 3 trillion at the end of 2012 to EUR 2.3 trillion on Nov. 4.

The authorities, incredibly, see no harm in allowing this contractionary trend to remain in place. This is a result of the mistaken Bundesbank philosophy that bond purchases by the ECB will somehow threaten hyper-inflation, even though much of the euro-area private sector is deleveraging and shrinking their balance sheets. The blunt truth is that when the private sector is repairing its balance sheets, it is very difficult to promote economic expansion. In times like this the ECB needs to expand its balance sheet to offset the balance sheet shrinkage elsewhere in the system. Yet the ECB is doing the exact opposite!

In addition, Mario Draghi, ECB president, made some ludicrous boasts in his news-conference yesterday. “The eurozone has fundamentals that are probably the strongest in the world,” he claimed, citing:

- The lowest aggregate budget deficit (for the combined eurozone) i.e., a small primary surplus of +0.7% of GDP compared with a deficit of 6% to 7% in the US and 8% in Japan.

- The highest current account surplus.

- The lowest inflation.

“This doesn’t translate automatically into a galloping recovery but gives the fundamentals on which you can pursue the right economic policies,” Draghi said. “Structural reforms are the necessary and sufficient conditions for this to happen. In the absence of that (structural reforms) we are going to stay here for quite a long time.”

This is completely absurd!

- The euro-area budget surplus is a sign that excessive austerity is being imposed across the euro-area, and that fiscal expansion is emphatically not being used to help the recovery.

- The current account surplus is mainly due to the stagnation/recession in the euro-area, the collapse of domestic demand and consequently of imports, especially in the periphery.

- The low inflation – soon to be deflation in my view – is also a symptom of inadequate domestic demand, and spending is only going to weaken further.

The language of the ECB is becoming like the Orwellian big brother’s Newspeak from the novel Nineteen Eighty-Four — a controlled language created by the state as a tool to limit free thought. The ECB’s language derives from a small clique or theocracy who believe that there is only one solution to the world’s problems — eliminate the budget deficit through endless austerity.

But as the gradual recoveries in the US and the UK demonstrate, central bank policies need to be expansionary — oriented to help with the repair of private sector balance sheets first — and only later do policymakers need to turn to address the public sector deficit. Restoring fiscal balance will be much easier once the private sector is growing again, but the ECB’s policy is constricting that recovery.

Chart data as of Nov. 8, 2013.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

|

NOT FDIC INSURED |

MAY LOSE VALUE |

NO BANK GUARANTEE |

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is a US distributor for retail mutual funds, exchange-traded funds, institutional money market funds and unit investment trusts. Van Kampen Funds Inc. is a sponsor of unit investment trusts. Both entities are wholly owned, indirect subsidiaries of Invesco Ltd.

© 2013 Invesco Ltd. All rights reserved.