Technology stocks are not what they used to be. While a few standout growth firms, notably Facebook andTwitter, capturethe public’s imagination, these are the exceptions, not the rules.

For most tech companies, and tech investors, the world is a slower, less dynamic place than it was before the tech bubble burst in 2000. It’s also a less significant place. At the tech bubble’s peak in 2000, large cap technology companies accounted for 35% of the value of the S&P 500. Today, they account for barely 17% of U.S. market cap.

What happened to the industry, and more importantly, is it a good place to put new money to work? Here are my answers to these two questions.

Q:What happened to the industry?

A: Valuations reached ludicrous levels in 2000 and business slowed. Back in the halcyon days of the late 1990s, tech companies redefined expensive. At the tech bubble’s peak in 2000,the S&P 500 Information Technology Indextraded at 75x trailing earnings. Suffice to say, no matter how good the prospects, few, if any, companies can justify that type of valuation.

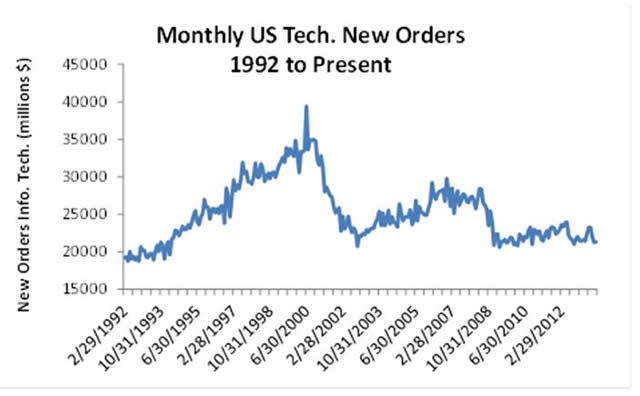

Adding to the sector’s near-death experience: not only were people paying far too much for a dollar of earnings, but some of those dollars never materialized. Between 1995 and the end of 1999, orders for new technology grew at an average pace of more than 8% year-over-year. Unfortunately, that pace was not to be sustained. Between 2004 and 2008, new orders slowed to roughly 4% year-over-year on average. Since 2010 the situation has gotten even worse. Even after exiting the recession, growth in technology new orders has averaged less than 1%, as the chart below shows. To be clear, this is not just a tech problem but reflects a general caution among, and lack of capital spending by, businesses.

A:So is tech a good place to put new money to work?

Q: The irony is that while the sector’s growth is much slower than in the past, tech is probably a more interesting place to invest now. Tech stocks are reasonably priced and typically carry little debt, making the sectorless vulnerable to rising interest rates. Based on the current state of tech orders, the sector, now valued at roughly 16.5x earnings, looks to be trading at around 10% below fair value. Assuming we see some modest pickup in business spending next year, the sector is probably even more undervalued.

While I don’t see a return to the glory days of the late 1990s, the good news is that few expect as much. For that reason, I see value, if not excitement, in the sector and I continue to advocate that investorsoverweight it relative to other sectors.

Sources: Bloomberg

Narrowly focused investments typically exhibit higher volatility. Technology companies may be subject to severe competition and product obsolescence.

© iShares Blog