Q1: Following gold’s large decline in 2013, what are your thoughts on the price of gold going forward?

We believe that gold should stabilize and may firm in price as we head into 2014 given the accommodative and what we believe are even extreme monetary policies seen across the major economies in the world – namely Japan, Europe, and the United States. In the U.S., Janet Yellen’s nomination as the next head of the Federal Reserve could extend the current near zero short-term interest rate environment for some time.

The demand for physical gold also continues to rise. Close to 50% of global gold demand

emanates from India, which is the largest jewelry market in the world, as well as China which is the fastest growing jewelry market globally. Both countries have a large and growing middle class whereby total gold demand through jewelry purchases should continue to outpace, at four to five times the volume, that of the U.S.

It also must be remembered that gold’s price is closely tied to investor sentiment. The current run-up of the equity market has turned investors’ attention to stocks and away from commodities. When commodity prices are advancing as a result of inflation or increased demand, investors often gravitate to gold and we expect that to be the case as a result of accommodative monetary policies. However, the long-term success of the Tocqueville Gold Fund has been attributed to investing in the shares of miners rather than a direct investment in gold.

Q2: What has been the price relationship between gold and the miners since gold peaked in 2011?

Traditionally, the miners trade at 1.5 - 2.0x that of the underlying commodity; although at times the price relationship between gold and the miners can decouple and one may move in the opposite direction from the other. This price movement relationship between the two has been relatively consistent since gold’s peak in 2011.

While gold has declined primarily due to downcast investor sentiment and a robust equity market, the price of miners has fallen for different reasons. The industry is undergoing various structural and operating changes. Miners are attempting to become more efficient; driving down the cost to extract an ounce of gold.

Previously, with gold at much higher price levels, new mine development and acquisitions became the focus. Cost control was often a secondary objective. Today the reverse has occurred and that is a very positive development. Miners are looking to reduce the cost of production and maintain an attractive margin in a much lower price environment for gold. This retrenchment will take time to yield results; but it is a healthy phase that will allow well-managed companies to add shareholder value through better capital allocation.

Q3: With many miners experiencing operating challenges, do you foresee industry consolidation?

We are already starting to see firms rethink how they operate. Some may consider the merger route whereas others may look at joint venture opportunities with companies that have a stronger capital structure. While each company has their own break-even metric, in general the threshold for profitability can be pegged to a price of gold of approximately $1,200-$1,250 per oz. Using that guideline, we believe that about 20% of miners are unprofitable at that price level. These less efficient companies need to further drive their operating costs down, participate in joint ventures, or seek consolidation alternatives.

Within the Fund’s portfolio, we seek to own miners with very capable managements, strong balance sheets, and operating costs at the low end of the spectrum. In fact, we’re seeing quite a few opportunities surface which we believe offer compelling potential for value creation.

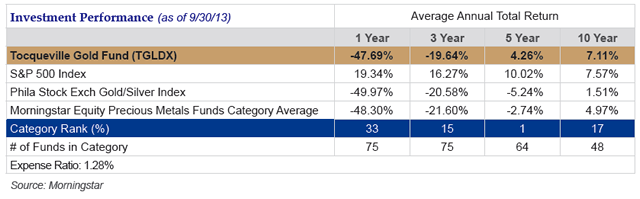

Performance data represents past performance and does not guarantee future performance.

The investment return and principal value of an investment will fluctuate and the investor’s shares, when redeemed, may be worth more or less than their original cost; and current performance may be lower or higher than the performance data quoted. Fund performance current to the most recent month-end may be obtained by visiting our website at http://tocqueville.com/mutual-funds/tocqueville-gold-fund/performance, or by calling 1-800-697- 3863. Total returns assume reinvestment of dividends and capital gains.

The Fund invests in gold, which involves additional risks, such as the possibility for substantial price fluctuations over a short period of time. The Fund also may invest in foreign securities, which involve greater volatility and political, economic and currency risks and differences in accounting methods. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund.

The Philadelphia Stock Exchange Gold/Silver Index (with income) is a good indicator of the performance of the common stock of companies in the gold and silver mining industry. It does not incur fees and expenses. The S&P 500 Index is a market-value weighted index consisting of 500 stocks chosen for market size, liquidity, and industry group representation. Returns are adjusted for the reinvestment of capital gains distributions and income dividends. You cannot invest directly in an index.

Star ratings are based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a fund’s monthly performance (including the effects of sales charges and redemption fees), placing more emphasis on downward variations and rewarding consistent performance. The overall rating is a weighted average of the 3-, 5-, and 10-year (if applicable) returns. 5 stars = top 10% of funds in a category; 4 stars = next 22.5% of funds; 3 stars = middle 35%; 2 stars = next 22.5%; 1 star = bottom 10%. Ratings are subject to change monthly. The Fund received 4 stars for the 3-year period, 5 stars for the 5-year period, and 4 stars for the 10-year period ended 9/30/13 among 75, 64 and 48 Equity Precious Metals Funds, respectively.

Lipper Fund Awards are given to the fund with the highest Lipper Leader for Consistent Return value within each eligible classification over three, five or ten year periods. For a more detailed explanation of the methodology, please review the Lipper Fund Awards 2012 - Methodology document on http://www.lipperweb.com/Awards/FundAwards.aspx. The Precious Metals Lipper Fund Award presented to the Tocqueville Gold Fund (TGLDX) was judged against 19 funds over a 3 year time period and 18 funds over a 5 year time period ending 12/31/12. © 2013, Reuters, All Rights Reserved.

This is not an advertisement or solicitation to subscribe to the Tocqueville Gold Fund, which may only be made by prospectus. Before investing, consider the Fund’s investment objectives, risks, charges and expenses. Contact 1-800-697-3863 or visit www.tocqueville.com/mutual-funds for a prospectus containing this information and other information. Read it carefully before investing.

The Funds are distributed by Tocqueville Securities L.P., which is a registered broker-dealer and member of the Financial Industry Regulatory Authority, Inc. Tocqueville Asset Management L.P., the Funds’ investment advisor, is an affiliate of Tocqueville Securities L.P.

© Tocqueville Asset Management