Dear Fellow Investors:

Will the US economy grow in an above-average way in the next ten to twenty years or do we need to resign ourselves to an era of anemic economic growth? Two pieces of information came out this week, adding to existing information on the subject and speak to this core debate in the US stock market. The first piece was called “Slowing to a Crawl” by Jonathan Laing from Barron’s. It argued that economic growth rates in the US could be significantly below the average of the last fifty years and was based on research from two JP Morgan economists:

Future productivity trends are far more difficult to forecast than demographics, but recent trends in the former don't offer much room for optimism. In a report entitled "U.S. Future Isn't What It Used To Be: Potential Growth Falls Below 2%," JPMorgan economists Michael Feroli and Robert Mellman recently pointed out that over the past three years, nonfarm labor productivity increased at only a 0.7% annual pace. This compares with the post-World War II average annual boost to gross domestic product of 2.3% and the 2.9% average yearly rise for the decade ending in 2005 when the burgeoning of the Internet and e-commerce sent output per man-hour into overdrive.

The second piece was the release of the Federal Reserve Board’s latest research on the Household Debt Service Ratio. It included some improvements in the analysis of the data and showed the lowest and most favorable debt service ratio that has existed in the US since the beginning of 1980. As the graph below shows, households in the US are living the farthest inside their means in decades and farther than in the early 1980’s and 1990’s during other very difficult stretches in the economy. Above-average economic growth followed in the next five to ten years when we moved from very low household debt service to higher levels.

Source: Bloomberg

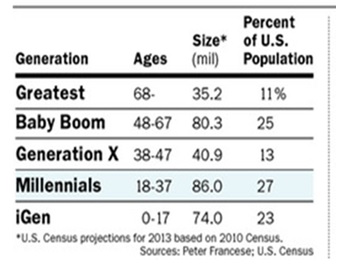

Among the existing information are the current demographics of the US as shown below. The last time we had the largest population group centered like this was the early 1980s.

The largest population group in the US is centered around 28 years of age. This is important because the average American marries at 28 years of age. Since the average person marries later in life than prior decades and many “normal” behaviors were postponed from 2007-2011, stock market participants assume that they never will. We believe most asset allocators assume that this is a secular phenomenon, best represented by a recent Time magazine cover call called “The Child-Free Life.” In it they argued, based on the last five years of data, that this might be the first generation of Americans which make no attempt to replace themselves in our population!

Messer’s Feroli and Mellman, the JP Morgan economists, argue that you have to be more productive and/or have significantly more people to grow like we have in the past. They show that in the last five years we’ve been neither productive nor fruitful and that the immigration environment won’t make up the difference like it did in the 1990’s and early 2000’s. Those who like to extrapolate recent trends into longer trends come to the same conclusion. They seem to think the US economy isn’t going to grow fast enough to draw existing unemployed people back to work or draw in those who have dropped out of the workforce. These are important discussions for the long-duration common stock owner because we are looking at the next ten to twenty years of underlying economic activity.

Let me expose Smead Capital Management’s bias. We believe that the financial meltdown of five years ago has colored the attitudes and analysis of most potential common stock owners and market strategists. Extrapolating the last five years is like driving by looking in the rearview mirror. You can see what you came through, but it does little to improve personal safety. Therefore, we assume it is better to look at similar points in history and look for the rhymes, as Mark Twain once said.

We believe this is completely analogous to 1973-74 and the early 1980’s. The deep recession and lack of confidence triggered by the Watergate hearings caused young adults to postpone all kinds of “normal” behaviors in 1974-76. The US economy hit 10% unemployment in 1981-82 after another oil shock (1979) which was accompanied by virulent inflation and the largest population group lodged in the peak marrying age of 23 years. Many of my college friends couldn’t find 40-hour per week jobs until two years after graduating in 1980. Two recessions in three years and 20% interest rates for business loans will cause circumstances of that kind. I remember that the popular press found every naysayer out there who argued the US was never going to be the world’s economic powerhouse and most thought Japan was prepared to take our place.

How do you position yourself as a long-duration common stock owner vis-à-vis this debate? First, we contend that you have to understand what motivates people, and that can depend on which side of this debate you sit. If you believe the US has seen its best days, you seek more opportunities outside our borders (emerging stocks/bonds, commodities like oil, gold, etc.). You also are willing to pay up for success in the anemic environment. We believe this explains all the heavy momentum interest in those companies which produce spectacular sales gains.

Second, check where all the money is. If asset allocators are mostly betting on a bright picture of the economy and have loads of consumer and homebuilding confidence, bet they are wrong. We don’t believe this is the situation today. It seems to us that most wide asset allocators have more of their assets in bonds, international/emerging equities and commodity-related investments than they do in a positive view of the US economy’s future. We use doomsday visions based on the recent past (rearview mirror) as a reason to get more excited about the next five years (along with Time magazine covers).

To summarize, we like addicted customer base consumer discretionary companies and financial services companies which could benefit the most, in our opinion, from a ten-year rebound in the US economy. Higher consumer confidence and higher interest rates should be our friend. We like the following stocks in our portfolio for the long term, based on this under-appreciated demographic trend. Among individual equity names we like EBay (EBAY) as echo-boomers marry, have babies and buy houses and cars. Better blue-collar and trade employment would be great for consumer confidence. Next, we like Gannett (GCI). Their 43 network-affiliated TV stations 84 daily newspapers should provide the auto dealers loads of advertising outlets. Lastly, we like the major banks like JP Morgan (JPM), Bank of America (BAC) and Wells Fargo (WFC). If the echo-boomers surprise everyone and replace themselves in the next ten years, these banks will get better interest rate spreads and provide the loans to buy houses and vehicles which fit two car seats.

Warm Regards,

William Smead

The information contained in this missive represents SCM's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.

© Smead Capital Management