Bank Reform: Europe's Slow and Steady Progress Continues

When Spain’s real estate bubble burst in 2008, the country went into a recession. The country was returning to growth in 2010, just in time to be taken down by the continent’s emerging banking and sovereign debt crisis.

Since then, concerns about the stability of European banks have been at the center of the Eurozone’s malaise. The crisis revealed one of the central contradictions of the European project -- a continent-wide currency without a continent-wide banking authority or continent-wide fiscal policies.

The catch-phrase for the immediate policy response of European governments was “austerity.” Despite fierce resistance from the public in the peripheral countries of Greece, Portugal, Spain, and Ireland, and in the languishing larger economies of France and Italy, austerity went forward primarily via the route of drastic cuts to bloated public service sectors. We argue that over-staffed government payrolls have created many impediments to entrepreneurial growth in Europe, and that economic and job growth will be benefitted by reducing bureaucratic red tape.

Despite public opposition and the skepticism of some economists, there is growing evidence that cutting government payrolls has had positive effects. The poster-child for austerity is Latvia, which instituted stringent spending reductions and government reforms. Latvia exited recession in 2010, and in grew at a 4.4 percent annualized rate in the second quarter of 2013. The same trend is showing in the troubled periphery:

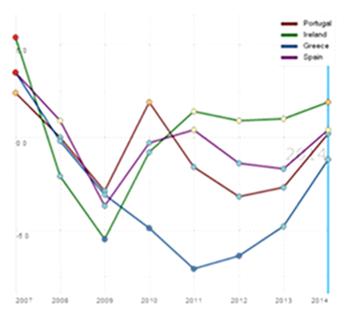

GDP Growth: Europe’s Periphery Lifting Out of Recession

Source: OECD

Spain, Portugal, and Ireland are exiting recession, and even Greece is set to do so soon. This can’t come soon enough for Europe’s unemployed; the Eurozone’s unemployment rate stands at 12 percent, which is high, but Spain’s, for example, is still at 26 percent.

Bank Reform Is the Critical Next Step

Austerity has done some of the job -- as have falling labor costs -- but up till now, political constraints have prevented Europe from dealing with its under-capitalized banks in a fashion coherent enough to reassure observers.

Under the stewardship of Mario “Whatever It Takes” Draghi, president of the European Central Bank (ECB), gradual progress is being made towards the establishment of a truly credible Eurozone banking regulatory regime. Until banks are forced to expose the problems hidden in their balance sheets, they won’t be able to start lending again -- and as we noted above, it’s lending that is the link between the current abundant liquidity and the growth of the real economy.

Now the ECB is poised to take over the role of regulator for systemically important European banks, rather than relegating this task to Balkanized national financial authorities. Previous “stress tests” performed on European banks are widely perceived to have failed to uncover problems because they were performed by national regulators. Now the ECB will perform some much more stringent tests ahead of its official assumption of the watchdog role.

National Backstops, But No German Money For Failing Banks

Mr Draghi, being interviewed on Bloomberg, also assured listeners that he has commitments from European leaders for the establishment of “adequate national backstops” -- funds in place on a national level for the recapitalization of failing banks, and systems for the unwinding of failed ones. This has been noted by analysts as a continuing weak point of Europe’s banking regulation -- insufficient funds for recapitalization and the lack of a transparent mechanism to deal with failed institutions.

Germany, the Eurozone’s undisputed leader, has resisted any use of funds from the European Stability Mechanism to directly recapitalize failing banks. And since this opposition is shared both by Angela Merkel’s Christian Democratic Union, and by the Social Democrats with whom she’s forming a coalition government, German resistance may not fade any time soon. Mr Draghi will have to continue to navigate these political shoals.

Nevertheless, we are encouraged by what we see in Europe. The current program in Europe has worked, helping gradually pull the continent out of recession, cutting bloated bureaucracies (and we say this with due acknowledgement that much deeper reforms in labor markets, and other deregulation, are also needed). Slowly but surely, a regulatory regime is taking shape that may be able to deal adequately with Europe’s sick banks. Should progress continue on the European banking front, we see even more hope for European growth to strengthen.

© Guild Investment Management