A very quiet week for stocks as earnings season kicked into high gear at last.

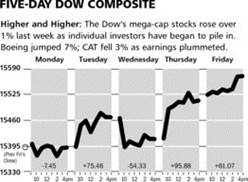

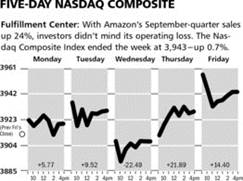

As the charts above illustrate, both the Dow Jones Industrial Average and the NASDAQ Composite finished higher last week by around one percent. Corporate news via earnings reports was mostly positive, but once again certain themes are evident. The most important of these is lack of revenue growth. From that you should glean - that despite all the happy talk coming from the likes of Warren Buffet etc… this economy just is not growing. That means lack of income growth, lack of consumer confidence and also lack of Federal Reserve Board tapering.

The Markets & Economy

Last week saw the government release a rather weak September employment report. While the monthly number itself was a disappointment with a gain of just 148,000 non-farm jobs created, the real troublesome part was the total lack of momentum in the job creation numbers over the past six months. In fact, given what will be a very bad number for October job creation has dropped down a notch from the rate of the first six months of the year which wasn’t impressive to begin with. To make matters worse, this tepid growth relies upon part-time jobs and a declining participation rate. With over 90 million Americans no longer counted in the workforce these statistics continue to amount to nothing more than “putting lipstick on a pig”.

When you put this together with the change of leadership coming to the Federal ReserveBoard as Janet Yellen takes over as Chairman in January, the financial press has now concluded that tapering will be put off until next spring. I have news for you, when we get to next spring and the economy is still in a sub 2% growth area, the taper talk will be put off again.

This change in policy expectations and downshift in the economy has brought about a little rally in bond prices, which of course makes stocks more attractive as dividends continue to move higher and financial engineering strategies continue to dominate the news. Thus the paradox will continue (which was finally discussed this week in Barron’s ) as to how this slow-growth economy is benefiting the investor class. This will continue. It is a shame that so many investors were frightened out of the market over the past few years.

I would be remiss if I didn’t note that the absolute fiasco known as Obamacare is also impacting consumer and business confidence. If one can believe the press, there are perhaps millions of people being dropped from their current health care coverage without currently being able to sign up or know what the cost of the new program will be.

Even the Democrats in Congress are now talking about a delay. This is very odd since they just all voted, without exception, not to delay the implementation a few weeks ago and in the process created the government shutdown for which civil servants not only received back pay but unemployment benefits as well. Only in America.

What to Expect This Week

The Federal Reserve Board concludes a two-day meeting Wednesday afternoon. As reasoned above, I do not expect anything to come of this but the commentary, and the attention which Wall Street gives will provide a nice sideshow.

Tonight, after the bell, Apple will report its earnings, but given last week’s various product announcements I hardly expect investors to look forward and not backwards, but there could be some volatility for the day traders.

Finally, as earnings continue to roll in, the investment background will continue to be swayed by the continuing failure of the Obamacare roll out. Should a delay start to become priced into stock prices, that should serve as a positive wild card for the stock market and perhaps for those in shock as they survey their own circumstances given the changes they face.

The chart next page from the Economic Cycle Research Institute continues to show that the economy is neither gaining momentum nor falling apart. More of the same and that is very good news for stock prices in general.

![]()

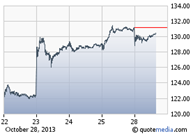

SYMBOL: BA

Boeing reported stronger than expected third-quarter earnings results, and raised its profit guidance for the full year. The Company earned $1.80 per share, compared to consensus estimates of $1.55, and revenues rose by 11 percent to $22.13 billion. Management also raised its earnings-per-share guidance to a range of $6.50 to $6.65, which should also prove conservative as sales momentum continues to accelerate. The Company’s backlog of orders also rose to a record high of $344 billion.

Demand for new commercial airplanes is growing by leaps and bounds as the newer aircrafts are much more fuel efficient and low interest rates have allowed airlines to step up their purchasing. Commercial plane sales rose 15 percent, as profits experienced a 40 percent jump from this quarter last year. This is causing management to raise its production across several major product lines, which should drive profit growth for the next several years.

Even though the 787 has been in the headlines for some minor manufacturing glitches, demand for the aircraft remains robust. Boeing stated they are boosting production of the 787 from 10 per month by the end of this year, to 12 per month by the end of 2016 and 14 per month by the end of the decade. The Company has sold more than one hundred and thirty 787’s this year, which is close to doublingestimates, and currently has a backlog of 890 planes that have been ordered but not delivered.

Boeing is in the sweet spot of this business cycle, and currently has the best products to meet their customers growing demands. We believe we are still fairly early in the aircraft upgrade cycle and growth should remain strong for the next several years. Boeing has been a market leader for the past year and we don’t expect that to change. We look for earnings estimates to continue to climb at Boeing, which we believe will lead to a $160 share price within the next 12 months.

![]()

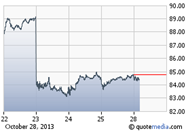

SYMBOL: CAT

Caterpillar reported disappointing third-quarter earnings results last week and brought down full-year profit guidance. Revenues fell by 18 percent from last year to $13.4 billion, as the Company earned $1.45 per share. Management now expects the Company will earn $5.50 per share this year, and profits will likely be flat next year. We expect we are near the bottom of this cycle for Caterpillar’s business, and any improvement in the global economy will be great news for shareholders.

While the mining division continues to suffer at Caterpillar, especially considering the Company’s recent acquisitions, there were some bright spots in the quarter. The domestic construction market continues to improve, which is allowing the Company to clear up any inventory issues. Also, management continues to cut costs by laying off another 3000 workers this quarter, and we expect a further reduction in the cost structure at Caterpillar in coming months.

Shares of Caterpillar did trade lower following this report, but only gave up the recent gains the shares had experienced the last couple of weeks. We look for the news from the Company to improve in coming months which should bring back investors’ interest in the Company. Caterpillar will be a much leaner company when improving business conditions in the global mining and construction industries take hold. The valuation is extremely conservative, and we are looking for the shares to climb back over $100 within the next 12 months.

SYMBOL: AKAM

Akamai reported strong third-quarter earnings results last week, but told investors that they had to renegotiate its pricing policy with its largest customer that could affect profits going forward. Earnings per share rose 65 percent from last year to $0.50 per share, which is a couple cents better than consensus estimates. Revenues also grew by 15 percent, and management did give guidance for the next quarter that was in-line with Wall Street’s estimates.

Even though demand for Akamai’s services is strong for the foreseeable future, Wall Street tends to obsess about pricing issues at the firm. As with most technology companies, prices large customers pay for its service decrease over time, but strong demand adds more customers which allows the company to grow its top and bottom lines. Customers from banks to sports leagues to large media conglomerates have to spend on Akamai’s products to increase the speed and improve the abilities of their websites. We believe Wall Street is overestimating the impact this will have on Akamai’s business, and are encouraged that management authorized a new $750 million stock repurchase plan.

Every sell-off has been a buying opportunity for Akamai shareholders since we became investors in the Company. We believe the selling is over-done, and are expecting the price to snap back in the near-term. This quarter does not change our long-term view of Akamai, and we believe the shares will still reach $60 within the next 12 months. We also would not be surprised if a larger tech company might be looking to take advantage of this sell-off by acquiring Akamai.

© McIntyre, Freedman & Flynn