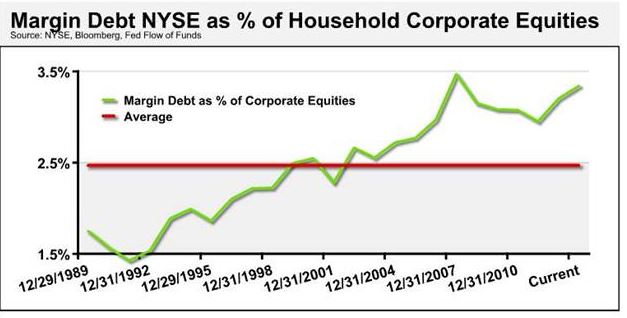

As the damage to sentiment that was brought about by the Washington “Drama Club,” a somewhat cautious number has come about. On October 21, 2013, the Wall Street Journal had an article detailing margin debt hitting new highs which counteracts some of the investor sentiment numbers that are detailed by several sources. To get a better understanding, we ran the margin debt as a percentage of corporate equities over the last 25 years.

Over the given timeframe, the average percentage of margin debt to household and nonprofit equities held on the Fed Flow of Funds report averaged 2.47%. The current standing, which is delayed a bit since the Fed Flow of Funds report has at least a quarter lag to it, shows that at current levels we are approaching 3.34%. The high was set at the end of 2007 when it hit 3.47%. To be fair about these numbers, we used year-end which would also not reveal seasonal patterns and makes the numbers more susceptible to deviations; however, the severity of the recent move is a bit problematic for several reasons.

1. The sentiment numbers that we monitor all point to over cautiousness at worst and tepid optimism at best. From fund manager surveys to individual investor sentiment to consumer sentiment numbers, all are pointing to a pragmatic investor that appeared to be dormant prior to the Washington, D.C. drama.

2. There is an immense amount of liquidity in the system, so the drawing of margin could be a bit suspect; however, ultimately, the degree of the run-up should cause a bit of pause for thought in the short run.

The earnings coming in also fuel a bit of this consternation as so far they have dropped Q4 estimates on the S&P 500 roughly 0.72%, according to Factset. This too has to be taken with a grain of salt in that only 20% of the companies have reported. According to Factset, 69% of companies have reported earnings above estimates, which is lower than the average of 73% over the last four years. Revenue shows roughly the same drop as 53% of companies have beaten revenue estimates so far this quarter, lower than the four-year average of 59%.

Our long-term perspective still remains intact for a multitude of reasons:

· The Federal Reserve is still accommodating

· Increased net worth and liquidity remain strong

· Earnings are still growing as is corporate cash

· An extreme amount of cash is in the banking system

· The contrarian aspect of broad-based sentiment numbers still point to economic growth.

It is too early to get overly worked up about the earnings quarter, but if “actions speak louder than words” with regard to the margin measure, then the earnings reports, coupled with the margin debt expansion, should at least give pause for thought.

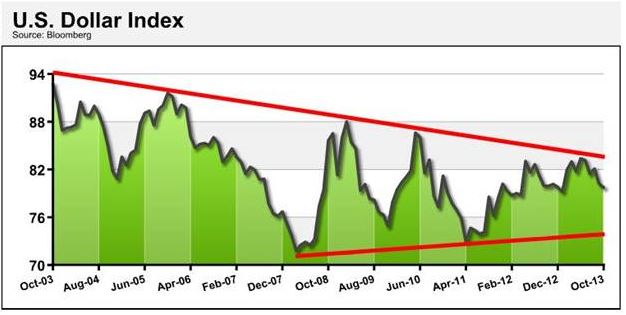

For areas where there isn’t such exuberance, consider some of the emerging markets, which have been beaten up for a multitude of reasons. One large reason is the value of the U.S. dollar, which has caused turmoil in almost all emerging markets. It also appears as though the U.S. trade-weighted dollar is settling into a long-term flag pattern, which traditionally denotes a breakout or breakdown.

Though it appears as one of the more over-weighted trades as denoted by fund manager surveys is a rally in the U.S. dollar, it appears we might be in for a little downward trading range. When the dollar weakens, emerging market equities tend to outperform developing market equities. We also find that allocations to emerging markets from global fund managers are sitting at lows not seen since 2001. From March 2001 to March 2004, the MSCI Emerging Market equity index returned a total of 61.7% while the S&P 500 had a total return of 1.35%. We would not expect similar returns, but with select emerging markets, namely China and Korea with possible early entry of India and select Asian emerging markets, now might be an opportune time to review tolerance ranges for existing assets and rebalance.

© Advisors Asset Management