I have to admit, I had a lot of trouble figuring out where to start this week -- unemployment from last week, post-shutdown observations, exports or sobering observations around expected growth of the US economy and expected implications. It was a Barron’s article, “Slowing to a Crawl” that pushed me to address the latter first. Why? Much of what the article focuses on hit very close to home – the impact of demographics and economic data on our economies. Have no fear, I do go on to address data (and observations that are not politically slanted) around our trade deficit and exports at the State level and conclude with a look at the employment scene.

“Slowing to a Crawl” – Thoughts on How to Monitor If and Where

This weekend, Barron’s ran a story, “Slowing to a Crawl,” that pointed to the actual and projected decline in economic growth for the US – from 3.2% to 1.9%. The article points to growth being dependent, in part, on demographic factors. To start simply, weaker growth means less than expected dollars to the Federal, State and local coffers which can lead to higher taxes, controlled spending or policy change (sounds like all the things the DC crowd can’t agree on). “Tax revenues are likely to fall short of projected levels.” Check those municipal budget assumptions and be ever so cautious about the discount rate used in pension plan assumptions.

Regular readers know our focus has been around economic and demographic data as the drivers of municipal economies. The Barron’s article, in many respects, reinforces this point. The article sites several drivers for its economic growth forecast including population, income, unemployment and labor force participation. While US overall growth will slow, certain States and local economies will prosper while others do not. Some food for thought: 32 States have seen their working age population (18-64) rise from 2011 to 2012 (latest reported actual data), of that group:

- 4 States have seen their Employed as a Percent of Population decline – Arizona, Oregon, Tennessee and Virginia

- 4 States have seen their Labor Underutilization Rate increase -- Delaware, North Dakota, New Jersey and Tennessee

- 4 States have seen their Average Weekly Wages Fall – California, Delaware, Maryland and Nevada

Some insights around income are below when employment is addressed. The point, which regular readers have seen before, is that the underlying data around demographics and economics – drivers of tax rolls, receipts and spending – is more critical than ever as our economic growth downshifts.

Before shifting gears, not to be lost in this debate is the reality that America is resilient and, as John Mauldin recently noted, the future can be rather bright as discovery and ingenuity continue to be alive and well in America. In this vein, a note to DC, we need to be progressive and grow our human capital and intellect to meet the demands of tomorrow.

Exports – Will Our Foreign Follies Hurt US Exports?

Before you read this next bit, please cast aside your political perspective– the focus is not whether I (or you) agree or disagree with decisions made but whether and to what extent those decisions will impact our economy.

It seems the US can’t stop stubbing its toe when it comes to foreign policy – even the NY Times had some interesting articles and commentary over the weekend. In short, seems we Americans are pissing off our allies everywhere (we used to focus on our enemies who generally are not our trading partners). First Edward Snowden caused some issues for us and then the government decided to shut down and threaten to default, royally irritating our foreign creditors and trading partners. Next, after asking our European and Middle East allies to stand with us in addressing the use of chemical weapons in Syria, we changed our position (as Robin Williams once mocked a former President: If you cross this line, we will be forced to act. No, this line …) and caused them serious embarrassment at home. We rankled our Middle East allies by engaging with the Iranians (Saudi Arabia and Israel especially upset). This week culminated with our diplomats being called to embassies in Europe and President Obama receiving not so friendly calls from the German Chancellor and French President. And don’t forget Mexico and our Central American allies were not too please about our alleged spying activities.

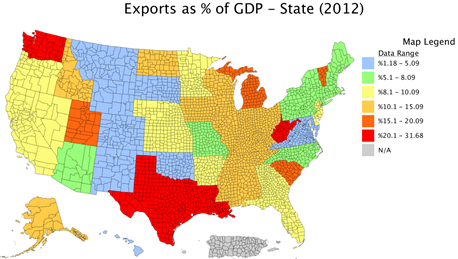

The world is a small place so the question is what impact, if any, will these matters have on our economy and our exports? Each of the States rely on exports for some percentage of their GDP (2012) and 20 States relying on exports for more than 10% of their GDP.

DIVER Analytics, Map Module; US Census Bureau and BLS

This leads to the exports report for August which came out last week. The month on month change was, for the most part, flat with the US trade deficit essentially unchanged. Year on year, the deficit was about 13% less than the shortfall during the same period last year but most of that improvement was the result of shrinking imports of oil and not rising exports. Amongst the States, about half have seen their growth of exports rise from last year (the glass half-full approach) – 24 are not seeing growth.

![]()

DIVER Analytics, Filter Module, US Census Bureau.

All of this leads me back to the question around our foibles with our allies and trading partners. Will our actions impact our State and local economies? Stay tuned and keep an eye on Exports and Employment, especially in those States most reliant on Exports as a Percentage of their GDP.

Employment, Jobs and Confidence

Coming out of the shutdown, we heard that the shutdown had a serious impact on the “recovery” and that it drove Consumer Confidence down. On the former point, I continue to have a very tough time with that one and the data below supports my point. On the latter, I think sentiment, which is the human response to current events, certainly was negative when the folks in DC couldn’t play nice in the sandbox (they will try that again with some new committees to produce a new drama series this winter). Nevertheless, the media and government’s focus around the stock market hitting highs as signs of “all is well” belies the reality articled in the Barron’s article and that our recovery is painfully slow and uneven despite aggressive monetary policy (remember that “tapering” word – smart folks suggest this will occur next Spring at the earliest).

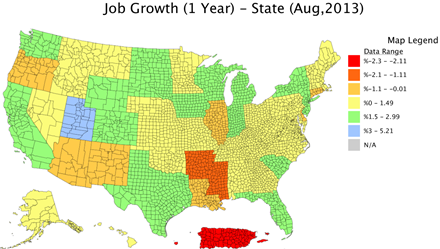

My point about underlying data not being consistent with a good recovery is supported by the August employment data (to avoid being hypocritical, I side-step the pretty bad “First Friday” report – issued the 4th Tuesday of October – and take a closer look at the data from August. The below gives a sense of Job Growth at the State level with greens and blues showing growth greater than 1.5% (you decide if that is an acceptable rate of growth) .

DIVER Analytics, Map Module; US Census Bureau and BLS

Going to the County level and looking a bit deeper, only about one-third of all US counties show growth in the percent of the population employed, the number of people employed and wages.

DIVER Analytics, Filter Module, US Census Bureau., BLS.

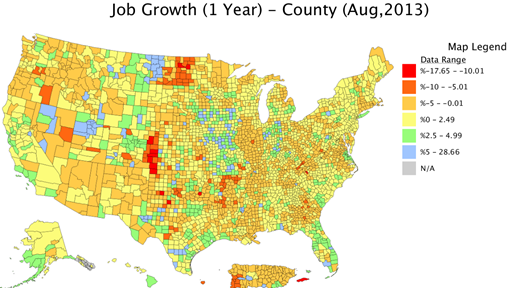

As for actual Job Growth at the County level, a picture is worth a thousand words. Does the actual growth support projections? Check the legend to the right and the details for places of interest to you.

DIVER Analytics, Map Module; US Census Bureau and BLS

Have a great week. May your glass be half full.

Gregg L. Bienstock, Esq.

CEO & Co-Founder, Lumesis, Inc.

Data Released Last Week:

- Weekly Initial and Continued Jobless Claims, State, 10/12/2013

- Exports Total (Monthly), State, Aug 2013

- UPDATED: Affordable Care Act Medicaid Expansion, State, Oct 2013

- Unemployment, County, Aug 2013

- UPDATED: Bankruptcy Filings - Issuers, State, County, 2013

- UPDATED: Default Filings - Issuers, State, County, 2013

© Lumesis