Debt Limit Extended, Fed Policy in the Wings - What to Expect from the Markets

Last night Congress reached an agreement to raise the debt limit and end the 16-day shutdown. After all the acrimony and tense negotiations, the deal passed by a comfortable margin with 81-18 vote in the Senate and 285-144 in the House.

Key details of the deal:

- The government reopens on October 17, 2013.

- Congress will provide spending authority through January 15, 2014 at the same spending level in effect prior to the shutdown.

- The debt ceiling is extended until February 7, 2014.

- Reality check: the real deadline will be sometime in mid-March, according to Goldman Sachs. The agreement allows the U.S. Treasury to utilize bookkeeping strategies known as “extraordinary measures” once the debt limit is breached on February 7th.

The Dates to Look Out For

December 13th – Congress will create another Super Committee to reconcile the differences between the budget outlines passed earlier in the year by the House and Senate.

- Could lead to renewed fiscal headlines amid contentious partisan talks. Expectations are fairly low that both sides can come together to craft a long-term solution to the debt.

- In the end, makeup of the Committee would determine the ultimate success or failure of the outcome. There was only 1 moderate nominated to last year’s Super Committee – signaling failure right from the start.

December 17-18th – After its surprise decision not to taper at the September 18th meeting, the market will look to the December 18th meeting of the Federal Open Market Committee (FOMC) to see if the Federal Reserve will begin tapering.

- The rally in U.S. Treasuries and the U.S. dollar selloff suggest financial markets do not expect the Fed to taper at the December meeting.

January 15th – When the spending authority extension expires and the 2nd round of sequestration is triggered.

- These cuts and reduction in spending growth amount to $89bn in fiscal year 2014, based on economist estimates.

- Both parties would like to replace some of the cuts under sequestration, such as those to defense, but those cuts would need to be replaced with savings from other parts of the budget. There’s little agreement about where the additional savings would come from.

February 7th – At this time last year the Treasury had around $200bn in so-called extraordinary measures. Goldman Sachs estimates assume they will have about the same in early 2014.

- In 2012 and 2013, it took from February 7 until March 15 and March 6, respectively, for the debt subject to the limit to climb by $200bn.

- Goldman Sachs expects Congress will need to raise (or suspend) the debt ceiling again by mid-March of 2014 “the real debt limit.”

Fed Monetary Policy– the Impact of Congress’s Actions on Tapering and the Economy

The Fed stunned the markets by not tapering at the September 18th FOMC meeting. It was presumed the uncertainty of the debt limit was the chief factor. The Fed reiterated it would remain “data dependent.” Congress’s kicking the can down the road prolongs the uncertainty over the debt ceiling into the first quarter of 2014, and therefore the likelihood of Fed tapering.

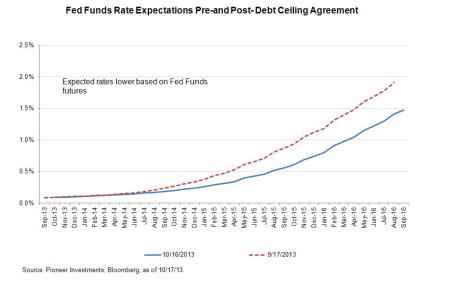

In addition, the government shutdown could have residual effects on business and consumer confidence, and could lead to some weaker macro data in the coming weeks. This should reduce the probability of Fed tapering at the December FOMC meeting. The markets have pushed back the start of the tightening cycle from just one month ago (Chart 1). A month ago, the markets fully priced in a 25bp rate hike on April 2015, but now are expecting one on August 2015.

We may already be seeing some of this residual impact on the U.S. economy. Yesterday’s release of the Fed’s Beige book highlighted an increase in uncertainty due to deadlock over the budget. Employment growth remained modest. The 4-week moving average of jobless claims moved noticeably higher since the start of the government shutdown from a pre-shutdown level of 305k, to a post-shutdown level of 336k. The Labor Department warns that federal workers’ jobless claims are not reflected in total, implying that jobless claims will continue to drift higher in the coming few weeks.

Overall, we believe the U.S. economy is on track to grow by 3% in 2014 and that any delay in tapering is likely to be temporary. We do expect a modest tapering to begin sometime in Q1, either January 29th or March 19th contingent on a satisfactory resolution to the debt limit.

Short Term Market Implications: Currencies, Fixed Income and Equities

Currencies

In the short term, the U.S. dollar bull market is likely on hold. (Read more about that in my Blue Papers The U.S. Dollar: Awaiting the Upcoming Bull Market, and Revisiting the U.S. Dollar Bull Market).

The U.S. dollar should remain under pressure, or at the very least range bound, especially against emerging market and developed nation currencies, as the uncertainty over the longer term debt resolution and potential weak economic data triggered by the government shutdown keeps U.S. monetary policy on hold.

This environment could be a favorable one for higher yielding currency trades such as the Mexican Peso (MXN) to outperform, particularly against lower yielding ones such as the Japanese Yen (JPY). If we get further clarity on U.S. monetary policy, and, more importantly, the debt ceiling, the USD is poised to resume its upward trajectory.

Fixed Income

We expect to see the front end of the U.S. Treasury curve (shorter-dated Treasuries) normalize and stabilize from rates having surged at the prospect of default during the debt ceiling debate. With expectations the Fed may not taper in December, there is increasing risk of 10-year yields trading in a slightly lower but more volatile range of 2.4%-2.9%. Nonetheless, we believe there is a limit to how far long-term yields can rally. We expect stronger U.S. growth in 2014 should trigger the Fed to commence tapering. High yield bonds should perform well in this environment.

Equities

In general, we believe accommodative monetary policy and stable treasury yields may support the year-long equity market rally that we’ve seen continue to year end. With the diminished likelihood of Fed tapering in December, earnings should become the bigger driver of equity markets.

© Pioneer Investments