Default is unlikely, but there is more at stake

In a recent publication, (Investing through the Washington Mess…) we outlined some of the dynamics at play regarding the ongoing debt limit debate in Washington. Latest developments notwithstanding, it is important to understand two key points:

• A default is very unlikely, and

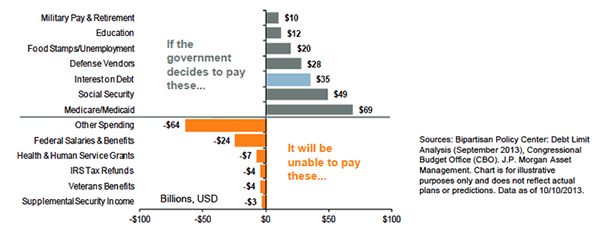

• If the debt ceiling is not raised, simple prioritization to avoid default by continuing to pay interest would still inflict severe damage on the economy and markets, and could result in a credit rating action

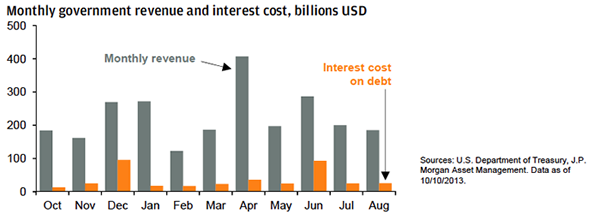

Current revenues are enough to cover U.S. debt interest…

Monthly government revenues are indeed enough to cover interest payments required on outstanding U.S. Treasury Debt.

…but ‘prioritization’ would result in real economic pain.

Prioritizing spending to avoid default is playing with fire; with monthly budget deficits of between 3% and 5% of monthly GDP, a prolonged period of balanced budget operations could deal a heavy blow to the economy.

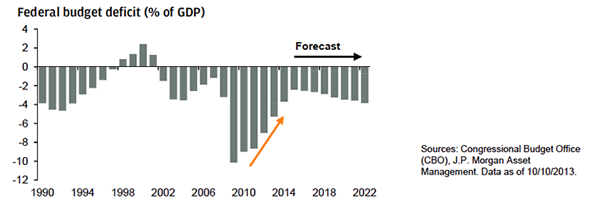

The U.S. has made strong progress on deficit reduction…

Importantly, the ongoing economic recovery and some spending restraint have resulted in a rapid decline in the U.S. budget deficits. This should provide some encouragement to those who most vehemently oppose raising the debt ceiling.

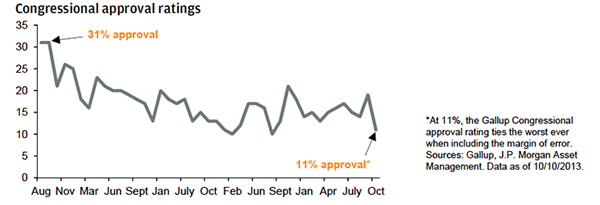

…and nobody wins politically until a deal is reached.

Politicians are human beings too. And while some members of Congress come from “safe zone” districts that are likely to re-elect them no matter the outcome of the debt dealings, in the end it stands to reason that cooler heads will prevail as Congressional approval ratings have again plunged to record lows.

While the situation is unnerving and certainly unpleasant to watch, a default on U.S. debt seems highly unlikely.

We believe investors are best suited to weather the storm with the support of a sturdy, well-balanced portfolio

Any performance quoted is past performance and is not a guarantee of future results.

Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal or tax advice. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Reference to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

J.P. Morgan Asset Management does not predict outcomes of any political events, nor do we voice firm-wide opinions on any political candidates.

J.P. Morgan Asset Management is the marketing name for the asset management business of JPMorgan Chase & Co., and its affiliates worldwide.

JPMorgan Distribution Services, Inc., member FINRA/SIPC

MI-MB-DefaultUnlikely_Oct2013

© JPMorgan Chase & Co., October 2013

© J.P. Morgan Funds