Absolute Return Letter: Heads or tails?

“Once one starts to think about it, it is hard to think about anything else.”

Robert Lucas, Economist and Nobel Laureate, on economic development in emerging economies.

Demographics captivate me. There are around 7.1 billion of us occupying planet earth today, going to 10 billion by 2050. I often think about how good old mother earth will cope with the additional 3 billion people we are projected to produce between now and 2050. More people translate into increased pressure on already scarce resources, but that is only part of the story and a story well covered by now.

From an investment point of view, it is more interesting that over 150 million people from around the world join the middle classes each year. The Brookings Institution reckons that about 2 billion people can be classified as middle class today. By 2030, Asia alone will be the home of 3 billion middle class people, and the global middle classes will be approaching 5 billion, 90% of whom will come from countries we today consider EM economies. In other words, less than 20 years from now, Asia will have 10 times more middle class citizens than North America and 5 times more than Europe. When we entered the new millennium not many years ago, 1 in 6 middle class people came from the United States. By 2030, only 1 in 25 will be American (see here). Meanwhile, in Latin America, the middle classes have grown by 50% over the past decade and now account for 30% of the population (see details here).

You can define ‘middle class’ in more than one way, but let’s not get hung up on details. The important consideration here is the sheer magnitude of this demographic shift and the effect it will have on pretty much everything. Rising living standards imply more money available for iPhones and package tour holidays, but it also entails increased consumption of fat and sugar and thus growing obesity problems. Over 300 million people worldwide are now classified as clinically obese, a function of the changing eating habits and exacerbated by increasingly sedentary lifestyles. In China alone, well over 100 million people are now considered obese, and half of them are children.

Growth of the middle classes is not the only thing to consider, though. Just as EM economies will produce armies of middle class people, our part of the world will become noticeably older. Worldwide, the population of over 65s is growing at 3.3% per annum compared with 1.1% growth overall. And vanity seems to prosper amongst those who are turning grey. The global market for anti-ageing products is worth an estimated $262 billion this year and is expected to reach $340-350 billion by 2018.

For all these reasons I find demographics intriguing. Yet there is one more reason why I can’t take my eyes off the subject. When speaking to people in our industry about it, I usually come up against what I call ‘polite interest’ which I usually interpret as utter disinterest. It is not that everyone can’t see that this seismic shift is going to have significant impact longer term. Yet the majority seems to think that it won’t really have any meaningful impact for the foreseeable future. From an investment point of view that is ideal, because it means that the changes to come are not yet fully priced in.

In short, we have two very powerful dynamics at work. We have the tailwinds created by the growing middle classes in EM economies, and we have the headwinds from the greying of the boomers in the old world. Which ones will prevail? Heads or tails? That is what this month’s Absolute Return Letter is about.

The greying baby boomers

Let’s begin with the easier one – how ageing affects the economy and financial markets. Chart 1 provides a simple illustration of the age-wise distribution of the U.S. population. The baby boomers are easily identifiable as the hump in the middle of the chart. In 2000, the biggest cohort was the 35-40 year olds. Today, almost 14 years later, the biggest cohort is the 50-55 year olds.

Chart 1: U.S. population by age and sex, 2010 v. 2000

Source: U.S. Census Bureau

We all know intuitively that our spending and savings patterns change as we get older. The daily school run is replaced by the occasional visit to the local GP. The trekking trip in the Himalayas becomes a cruise on the Nile. The Skoda becomes an Audi (and then a Skoda again), but is any of this actually significant enough that one can measure it on economic growth and returns on stocks and bonds?

In 2012, Robert Arnott and Denis Chaves published what I believe to be the largest study ever conducted on the effect on economic growth, stock and bond market returns from changes in age distribution (you can find the study here).

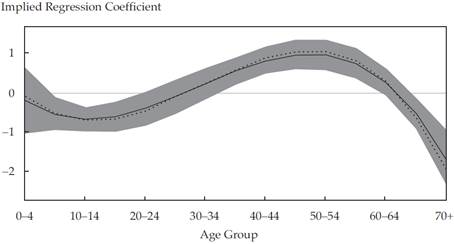

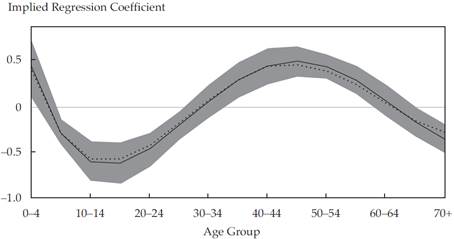

Charts 2a-c are taken from Arnott’s & Chaves’ paper and deserve close inspection as the results are highly significant; however, I need to explain how to read the charts. Arnott and Chaves used 60 years of data across more than 100 countries. The objective was to assess whether changes in the age-wise composition of the population has a significant effect on equity and bond returns and/or on economic growth. Returns were measured as excess returns over cash in order to adjust for the fact that the risk-free rate of return is vastly different across markets and time.

Let’s take a closer look at chart 2a. The chart peaks at around 1% for the 50-54 age cadre, meaning that a 1% higher concentration of 50-54 olds would lead to an increase in annual excess equity returns of approximately 1%. Likewise a 1% higher concentration of the 70+ age cadre would lead to a decrease in annual excess equity returns of about 2%.

Chart 2a: Equity returns vs. demographic shares

Chart 2b: Bond returns vs. demographic shares

Chart 2c: GDP growth vs. demographic shares

Source: Demographic Changes, Financial Markets, and the Economy, Robert Arnott and Denis Chaves, Financial Analysts Journal, Volume 68 No. 1, 2012.

Arnott and Chaves sum up their findings better than I could hope to do:

“Children are not immediately helpful to GDP. They do not contribute to it, nor do they help stock and bond market returns in any meaningful way; their parents are likely disinvesting to pay their support. Young adults are the driving force in GDP growth; they are the sources of innovation and entrepreneurial spirit. But they are not yet investing; they are overspending against their future human capital. Middle-aged adults are the engine for capital market returns; they are in their prime for income, savings, and investments. And senior citizens contribute to neither GDP growth nor stock and bond market returns; they disinvest to buy goods and services that they no longer produce.”

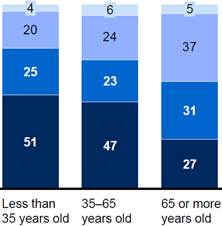

Given the large number of boomers knocking on the 70+ door, these findings should not be ignored. In another study from 2012, McKinsey Global Institute found that U.S. households reduce their exposure to equities in a meaningful way as they grow older, supporting Arnott’s and Chaves’ conclusion that large cohorts of 70+ year olds is bad news for equity returns (chart 3). We know that U.S. baby boomers own 60% of the nation’s wealth and account for 40% of its consumer spending, so their effect on the economy and financial markets shouldn’t come as a surprise.

Chart 3: U.S. households’ asset allocation by age cohort

Source: The impact of demographic shifts on financial markets, McKinsey Global Institute June 2012

Note: The numbers exclude retirement assets.

In a very interesting paper from 2011 (which you can find here), the Federal Reserve Bank of San Francisco found a powerful relationship between the age distribution of the U.S. population and equity market valuation, measured as the price-to-earnings ratio. Using what they call the M/O ratio – which measures the middle-aged cohort (those 40-49 years old) to the old-age cohort (those 60-69 years old) – they predict falling equity valuations out to the mid-2020s where the U.S. P/E ratio should bottom out at 8-9 times earnings. Valuations are then projected to rise again gradually (chart 4). The FRBSF study found that the M/O ratio explains about 60% of the change in equity valuations over the past 60 years which suggest quite a potent relationship.

Chart 4: Projected equity valuations from demographic trends

Source: Federal Reserve Bank of San Francisco, Economic Letter 2011-26

I will rest my ‘old age’ case here. I believe there is both ample and powerful evidence that the greying of the baby boomer (which, in my case, is actually thinning as much as greying) could quite possibly create significant headwinds for ‘old world’ financial markets in the years to come. Having said that, the fact that a study is statistically significant (which both of the above are) does not necessarily imply that it can be trusted to accurately predict the future. More about this in the conclusion later. Perhaps I should also note that my observations are not particularly pointed at the U.S. situation. I have used U.S. centric papers to support my arguments but only because the topic is much better researched in the U.S. than it is elsewhere. In many ways, the problem is much bigger in Europe and Japan.

The effectiveness of monetary policy is at risk

Before I go to the other side of the story, allow me to briefly mention a recently published IMF paper called Shock from Graying: Is the Demographic Shift Weakening Monetary Policy Effectiveness, which you can find here. The paper concludes that there is a strong link between the old-age dependency ratio1 and the effect of monetary policy on inflation and unemployment. I quote:

“The results reveal that a graying society, as measured by the old-age dependency ratio, exerts a negative (in absolute terms) statistically significant long-run impact on the effectiveness of monetary policy. All else being equal, an increase in the old-age dependency ratio of one point lowers (in absolute terms) the cumulative impact of a monetary policy shock on inflation and unemployment by 0.10 percentage points and 0.35 percentage points, respectively. The corresponding maximum impact of monetary policy is lowered by 0.01 percentage points and 0.02 percentage points. These estimates thus imply, when taken at face value, quite a strong negative long-run effect of the ageing of the population on the effectiveness of monetary policy. This is particularly significant when linked to, for instance, the projected 10 point rise in the old-age dependency ratio in Germany over the next decade.”

The implication of this is that monetary policy may have to change as the greying of society intensifies. Perhaps the solution is simply bigger moves in policy rates. 50 bps may become the new 25 bps. Maybe new and altogether different policy tools will have to be introduced. Nobody really knows because the IMF’s findings are very recent and probably not fully digested yet. For most EM economies this won’t be an issue because wealth is not skewed towards the older generations which quite conveniently brings me to the next part of my story – the outlook for EM economies which, in most cases, are characterised by an age profile very different from that of the more advanced economies.

Headwinds for some will be tailwinds for others

The oldest country in the world today, at least when measured in demographic terms, is Japan with an old-age dependency ratio just over 40 (you can check the old-age dependency ratio of your country here). At the other end of the range you find mostly Middle Eastern and African countries with ratios well below 10. Generally speaking, when the working age population grows faster than the broad population, demographics become a tailwind as far as economic growth is concerned. Hence, what is likely to become a significant headwind for advanced economies in terms of economic growth, will almost certainly become a tailwind for most EM economies.

However, that doesn’t necessarily mean that EM equity and bond returns will prove attractive. Let’s re-visit charts 2a and 2b which suggest that a ‘surplus’ of younger cohorts is a negative for equity and bond returns respectively. Now, I would not for one moment suggest that returns on EM equities and bonds are likely to disappoint for this reason alone, but it does highlight a potential challenge that those markets are facing. In order to deliver what the growing middle classes of those countries will expect, enormous investments shall be required and that is likely to drive up interest rates which may in turn hold equities back somewhat.

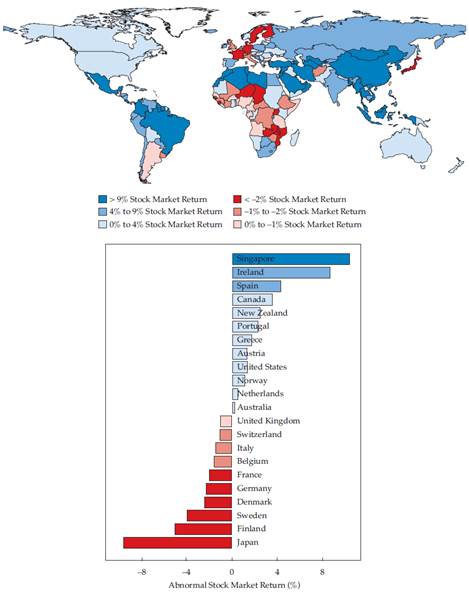

Rob Arnott and Denis Chaves concluded their groundbreaking study by projecting how the changing demographics may affect economic growth, equity and bond returns in every corner of the world (chart 5). I have only included the equity chart here, but you can find them all if you follow the link provided previously. Several observations stand out. First and foremost, with only a limited number of exemptions, equity returns are likely to be relatively modest over the next several years – in particular when viewing projected returns on a market-cap weighted basis.

Secondly, it is not simply a question of ‘old’ versus ‘new’ world. Some EM economies, in particular in Africa, do not come out as well as one might have expected, and some advanced economies do surprisingly well. Thirdly, within Europe, countries around the Mediterranean, often portrayed as the old people’s home of Europe, do relatively well compared to many countries further north. The Nordic countries fare particularly poorly.

Chart 5: Projected stock market returns, 2011-2020 (annualised)

Source: Demographic Changes, Financial Markets, and the Economy, Robert Arnott and Denis Chaves, Financial Analysts Journal, Volume 68 No. 1, 2012.

Note: Forecasts using changes in demographic shares.

Concluding remarks

Most of the observations and conclusions in this letter are based on regression analyses of historical data. In a rapidly changing and increasingly global economy, can one realistically expect behavioural patterns of yesteryear to be repeated? That is a question to which there is no obvious answer. Only time can tell.

This implies that one needs to interpret the output with care. One example: With few exceptions, the largest companies in the world today are truly global and much less dependent on their home market than they were previously. The fact that Switzerland, and with it most of Europe, will age rapidly over the next 15 years will mean much less to Nestle now than would have been the case 20 or 30 years ago. One therefore needs to look not only at each and every country in terms of where it is in demographic food chain, but also at the constituents making up the local stock market.

One also needs to put the U.S. predicament into perspective. As noted earlier, most of the observations made above are based on U.S. data for one simple reason; the U.S. is simply better researched than the rest of the world. This is not good news as far as Europe and Japan are concerned, both of which are burdened with an age profile much longer in the tooth than that of the United States. Germany, the largest economy in Europe, will have an old-age dependency ratio in excess of 50 by 2030. The same ratio in the U.S. will be a more manageable 37. (Let’s not even talk about Japan’s situation. They will be out of business by then unless drastic measures are taken.)

One should also spare a thought for the echo boomers. Have another look at chart 1. We discussed the hump in the middle of the chart and attributed it to the baby boomers. Further down the same chart you will find another hump. That’s the children of the baby boomers – also known as the echo boomers. Those countries with large populations of echo boomers, of which the United States is a prominent example, are likely to find that the echo boomers could quite possibly offset a not insignificant part of the negative effect from the baby boomers growing old and tired. As F. Scott Fitzgerald wrote in The Great Gatsby: “There are only the pursued, the pursuing, the busy and the tired.”

One final note: It is a poorly kept secret that economic growth in EM economies in recent years has been driven primarily by exports. The recent slowdown across most EM economies (which I discussed in last month’s Absolute Return Letter) is a reflection of the simple fact that exports to Europe in particular have deteriorated. As their middle classes gain increased traction, domestic consumption will become gradually more important to these countries, but it may also become important to us.

In a region full of old people, Europe must figure out what these people will want to buy, because that is the only way we can maintain economic growth and thus pay for a decent sunset for our elderly. Ironically, if we get this right, years of running external deficits could be replaced by an extended period of unusually favourable conditions for our export industries as we meet the needs of the ever rising number of affluent consumers across emerging markets.

Niels C. Jensen

8 October 2013

© Absolute Return Partners LLP 2013. Registered in England No. OC303480. Authorised and Regulated by the Financial Conduct Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP ( ARP). ARP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

1The old age dependency ratio is measured as the ratio of people aged 65 or older to the working age population (15-64 years old).

© Absolute Return Partners