Nowhere to Hide: Navigating Rising Rate Risk in High-Yield Markets

Summary

Over the past few years, investors have flocked to high-yield credit, many believing it a good way to mitigate their interest rate risk as well as capture additional yield. However, they may not realize the level of rate risk that has followed them. High-yield indices, negatively correlated to five-year Treasury bond yields over the past 15 years, have been positively correlated for the past year. This means that investors with passive high-yield exposure may face greater-than-anticipated risk of price declines should interest rates move higher. Bond managers who are actively engaged in individual security selection and duration management will be better positioned to enhance risk-adjusted returns and capital preservation, in our view.

Rising Rate Risk

High-yield credit markets have attracted a flood of investment in recent years. It’s not hard to see why: In a low-interest-rate environment, many investors naturally will seek the higher yield typically offered by speculative-grade credit. The additional income generated from higher-yielding bonds is often considered a cushion against interest rate volatility, as well. However, yields and interest rates have a unique relationship in high-yield markets, a fact that many investors may not fully appreciate.

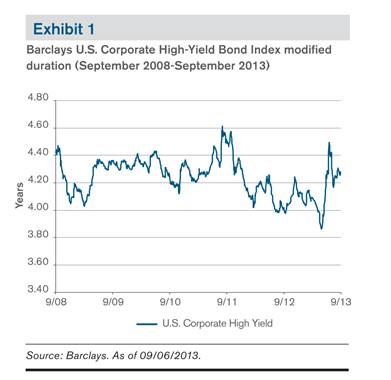

An example: Beginning in May 2013, as speculation grew that the Federal Reserve would begin to taper its quantitative easing program, longer-term U.S. Treasury yields rose. At the same time, the Barclays U.S. Corporate High-Yield Bond Index’s modified duration, a measure of its sensitivity to interest rate changes, increased sharply (Exhibit 1).

The main reason is that many high-yield bonds are callable — that is, they include an option that allows the issuer to terminate the bond before its maturity date, and issuers typically will do so if they believe they can issue new debt at cheaper rates. That possibility becomes more remote as interest rates rise, and as a result many bonds that had been trading to a call date will begin trading to their maturity dates.

This lengthens duration, or a bond’s sensitivity to interest rate changes. Worse, rate sensitivity increases as interest rates are rising, not an ideal situation from an investor standpoint.

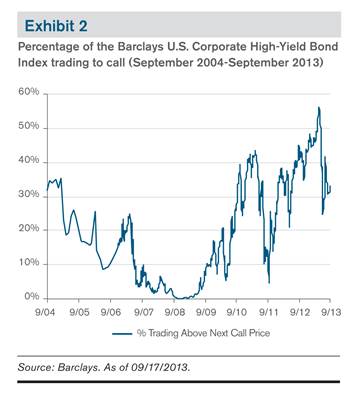

At this point, more than 90% of the bonds in the Barclays U.S. Corporate High-Yield Bond Index are callable, as declining interest rates over the past few years have encouraged a majority of debt issuers to seek the option of refinancing at lower rates. The key reason duration surged in June 2013 was because more than half of the callable bonds in the index were trading to call immediately prior to the jump in interest rates, as illustrated in Exhibit 2.

Increased Treasury Correlation

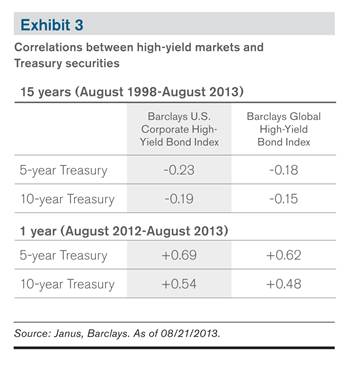

High-yield indices, negatively correlated to five-year Treasury bond yields over the past 15 years, have been positively correlated for the past year (Exhibit 3). It goes without saying that investors typically do not invest in high-yield credit in order to gain correlation with the Treasury market. In our view, this suggests that high-yield investors may be exposed to a greater-than-anticipated risk of price declines should interest rates move higher.

Of course, interest rates are not the only factor in whether a bond trades to call. In late summer 2011, despite the fact that interest rates were falling, the percentage of yield-to-call bonds dropped to near zero (Exhibit 2). This was because high-yield bond markets sold off, resulting in higher yields. In other words, despite lower interest rates, high-yield issuers became less likely to be able to refinance their outstanding debt at lower cost.

Given current market conditions, we believe that a 75-basis-point (bp) increase in five-year Treasury rates and a 100-bp widening in high-yield credit spreads, or vice versa, would be enough to cause a similar wave of callable high-yield bonds to revert to trading to maturity, driving the percentage of yield-to-call bonds back to the below-10% level seen in 2011. This potentially would expose many investors to unexpected duration extension at the worst possible time.

Know Your Risks

This does not mean that investors should avoid high-yield investments. We still believe that there are great opportunities in high-yield credit markets. In general, companies are in their best fiscal shape in decades. Management teams have made great strides toward deleveraging corporate balance sheets and improving credit profiles since the 2007-2009 recession, and credit default risk has dropped to very low levels.

However, interest rates, held artificially low for years by central bank intervention, appear poised to rebound. We are not sure that many of the investors who have flocked to high-yield markets in the past few years fully appreciate the level of interest rate risk they now may face. In our view, buying high-yield bonds purely in search of beta, or more-volatile moves and potentially higher return than less-risky investments, is a mistake — especially now, given the market’s rich valuations and increasing duration risk. Certain issuers also tend to be more exposed to interest rate risk, and the performance of their bonds will reflect this.

The bottom line: in our view, investors should understand and accept the level of rate risk in their high-yield investments or craft a strategy to manage around it.

We believe that an experienced, active bond manager can help in analyzing the likelihood that a particular bond will be called, and whether its price accurately reflects its potential risks. Bottom-up, individual security selection can help uncover bonds that are likely to benefit from their issuer’s improving credit profile and fundamentals, no matter what interest rates do, in our view.

Supplemental: Explanation of Trading to Call

When a bond is trading to a call date rather than its maturity date, it behaves like a bond with shorter maturity and lower duration.

To understand market dynamics, let’s consider a simplified example: a hypothetical 7% coupon bond paying interest once per year, maturing in 10 years but callable at $100 par in one year’s time.

If the prevailing interest rate is 5%, the issuing company will be motivated to call its 7% debt and reissue at the lower prevailing interest rate. The market understands this motivation and will price the bond as though it has one year left to maturity, referred to as “trading to call.” Assuming the bond is to be called in one year, one can apply a discount of the current interest rate, 5%, to the anticipated cash flow from a 7% coupon ($7 plus the return of our principal of $100) for a total of $107. Discounting this cash flow by 5% implies the bond is worth $101.90 today, which is what an investor would pay to earn a 5% return for the next year.

If the prevailing rate increased to 8%, the issuer would be disinclined to call its existing debt because new issuance would be more expensive. Now, instead of receiving $107 in one year, the investor would receive a stream of $7 cash flows each year for nine years, followed by a $107 payment at the end of the 10th year. The bond’s maturity would have extended significantly, and its overall sensitivity to interest rate changes would be greater as well. Discounting all of these cash flows at the now prevailing 8% interest rate, the investment is now worth $93.29.

Please consider the charges, risks, expenses and investment objectives carefully before investing. For a prospectus or, if available, a summary prospectus containing this and other information, please call Janus at 877.33JANUS (52687) or download the file from janus.com/info. Read it carefully before you invest or send money.

Investing involves market risk. Investment return and value will fluctuate, and it is possible to lose money by investing.

Bonds in a portfolio are typically intended to provide income and/or diversification. In general, the bond market is volatile. Bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Statements in this piece that reflect projections or expectations of future financial or economic performance of a mutual fund or strategy and of the markets in general and statements of a fund’s plans and objectives for future operations are forward-looking statements. Actual results or events may differ materially from those projected, estimated, assumed or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to the other factors noted with such forward-looking statements, include general economic conditions such as inflation, recession and interest rates.

U.S. Treasury securities are direct debt obligations issued by the U.S. Government. With government bonds, the investor is a creditor of the government. Treasury Bills and U.S. Government Bonds are guaranteed by the full faith and credit of the United States government, are generally considered to be free of credit risk and typically carry lower yields than other securities. Bonds in a portfolio are typically intended to provide income and/or diversification. In general, the bond market is volatile. Bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Duration measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates, all else being equal.

Barclays U.S Corporate High-Yield Bond Index is composed of fixed-rate, publicly issued, non-investment grade debt. The Barclays Global High-Yield Index provides a broad-based measure of the global high-yield fixed income markets. It represents a union of the Barclays U.S. High-Yield, Pan-European High-Yield, U.S. Emerging Markets High-Yield, CMBS High-Yield, and Pan-European Emerging Markets High-Yield indices.

The views expressed are those of the authors as of September 2013. They do not necessarily reflect the views of other Janus portfolio managers or other persons in Janus’ organization. These views are subject to change at any time based on market and other conditions, and Janus disclaims any responsibility to update such views. No forecasts can be guaranteed. These views may not be relied upon as investment advice or as an indication of trading intent on behalf of any Janus fund.

In preparing this document, Janus has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources.

Janus Distributors LLC (09/13)

C-0913-46527 09-30-15 188-15-26313 09-13

© Janus Capital Group