Background on the Stalemate

Congress has been dealing with two separate but related issues: whether to extend federal spending authority to cover day-to-day operations, and whether to raise the debt ceiling later this month, to allow for the issuance of debt and funding of current obligations. Obviously, Congress failed to meet the deadline for the first item, resulting in a partial shutdown of government services since October 1. As reported by the press, the stalemate stems from House Republicans' efforts to delay implementation of the Affordable Care Act (ACA) within the funding bill, which have met with resistance from Senate Democrats.

Short-Term Shutdown: Annoying but Less Scary

The shutdown affects many areas of government and is expected to result in the furlough of up to 800,000 federal workers. Despite the scary headlines, however, most economists believe that the economic impact of a brief shutdown—lasting no more than a week or two—would be limited. Should the shutdown drag on, the impact would grow, particularly if it hurts consumer confidence and results in lower spending and investment.

Although political predictions are unreliable, we think the shutdown will be brief as most voters strongly oppose shuttering the government in order to delay the ACA. We suspect that, as time wears on, negative public sentiment will increase and force centrist politicians from both parties to negotiate an end to the stalemate. In our view, the likely solution will be a bill that the Senate originally proposed—i.e., a "continuing resolution" that provides for funding and does not delay the ACA.

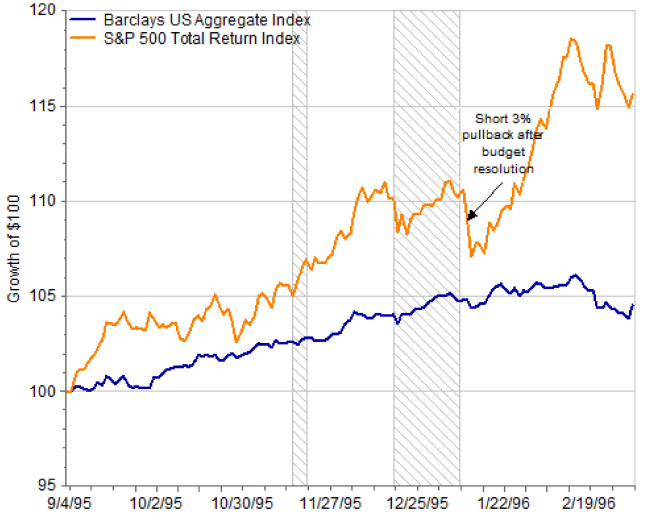

Fortunately, historical government shutdowns have not been particularly negative for markets. The last one (the longest since the 1970s) took place during the Clinton administration, and both equity and bond markets actually moved higher during that period (see display). While the ultimate market impact remains to be seen, we do take comfort in the fact that the markets have not overreacted on the downside to past historical government shutdowns. Accordingly, while we do anticipate equity volatility staying somewhat elevated, we favor maintaining assets allocations in line with long-term objectives.

MARKETS LARGELY SHRUGGED OFF THE LAST SHUTDOWN

(HIGHLIGHTED REGION)

FactSet. For illustrative purposes only. Indexes are unmanaged and are not available for direct investment. Unless otherwise indicated, returns reflect reinvestment of dividends and distributions. Investing entails risks, including possible loss of principal.

Debt Ceiling Debate: The Larger Threat

A bigger issue, however, is the looming debt ceiling deadline. Unlike the shutdown, the failure to raise the debt ceiling would hamper the U.S. Treasury's ability to issue debt to fund its obligations, which could result in technical default if interest on debt is not paid on time. The implications, obviously, could be much more severe for interest rates and the broader economy.

The path to resolving the debt ceiling issue is hard to predict and could depend on how the shutdown is resolved. If the shutdown continues toward the debt ceiling deadline, public anger could intensify. With an eye toward the 2014 mid-term elections, members of Congress may soften hardline positions sooner rather than later—particularly in light of polls suggesting that Republicans would be assigned more blame for the impasse. There is also a possibility that both the debt ceiling and shutdown could be resolved at the same time as part of an agreement, which would be a big relief for the market. On the other hand, a stalemate could actually harden current positions, making resolution more difficult. We believe this is a less likely scenario.

Overall, while the situation appears precarious, we believe it poses less of a threat than the 2011 debt ceiling debate which caused markets to decline 20% and the U.S. government to lose its AAA credit rating from Standard & Poor's. At that time, the government was running large deficits and the markets were concerned that sharp budget cuts would harm an already fragile economy. In the current case, global growth has picked up significantly and the United States' improving deficit picture suggests potential public support to pursue a deal.

Focus on Fundamentals

Regardless of the noise coming from Washington, we believe it's important that investors focus on the economy, which continues to recover steadily. While market volatility could increase, we believe any such increase will likely be short-lived as the economic implications of both the shutdown and debt ceiling debate (barring a default, which in our opinion, is very unlikely) should not be too meaningful. This means that short-term market fluctuations could provide opportunity to buy into stocks at attractive prices. Moreover, the additional uncertainty could make it more likely that the Federal Reserve holds off on "tapering" until we get through some of these issues—which would likely be another positive for most financial assets.

© Neuberger Bergman