Weak Credit Growth Main Reason for Lackluster Economic Recovery

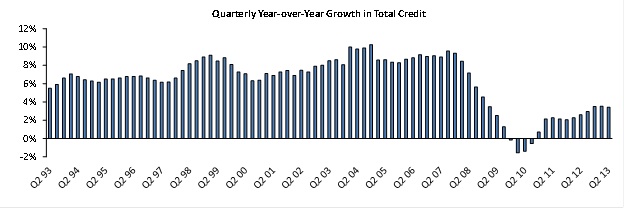

Growth in Total Credit Stays below 4% Year-Over-Year since End of Last Recession

The U.S. economy is a credit-based economy. Economic expansion is fueled mostly by borrowing and consuming rather than saving and investing. A continuous expansion of credit is needed for the economy to grow. The main reason the economic recovery has been so lackluster is that credit growth has remained weak despite the Federal Reserve's continuing liquidity injections.

In the past six decades, total credit as measured by the Fed's Z.1 (Flow of Funds Accounts) increased at an average rate of 7.6% year-over-year. Before Q4 2009, it never decreased on a year-over-year basis. Amid the financial crisis, it decreased on a year-over-year basis for four consecutive quarters from Q4 2009 through Q3 2010. Year-over-year growth has been positive in every quarter since that time, but the average increase has been only 2.5%, and it has stayed below 4%.

We doubt economic growth will accelerate significantly until total credit expands more rapidly. The Fed can print all the money it wants, but it cannot control where the money goes. Much of the money it prints is being channeled into financial speculation rather than lending in the real economy. Unless credit growth picks up, economic growth will be weak at best.

Source: Federal Reserve

Fund Flows Swing Wildly for Fourth Consecutive Month as Fed Contemplates "Tapering." U.S. Equity Funds Get $14.3 Billion in September, Nearly Reversing Outflow of $17.7 Billion in August.

Fund flows have swung wildly for the fourth consecutive month as the Federal Reserve contemplates scaling back the pace of its money printing.

The flows of U.S. equity exchange-traded funds have been most volatile. After issuing $31.8 billion in July, they redeemed $15.3 billion in August and then issued $16.7 billion in September. While we have no way to know for sure, these shifts are likely due to hedge fund positioning. As usual, ETF investors have been poor market timers, which is why we pay such careful attention to them as a contrary indicator.

U.S. equity funds as a whole—mutual funds as well as ETFs—have issued $14.3 billion in September, reversing most of the outflow of $17.7 billion in August. This month's inflow is solid but nowhere close to a record.

Offshore stocks have been disproportionately favored this month. Global equity MFs and ETFs have issued $23.8 billion, which is the fifth-highest inflow in any month on record. As is often the case, flows are following performance. The average global equity fund (+4.3%) has outperformed the average U.S. equity fund (+1.8%) since the start of August.

All equity MFs and ETFs have issued $38.0 billion in September, the eighth-highest inflow on record. Note that seven of the ten largest inflows occurred either in 2000 or 2013. The enthusiasm of fund investors for equities this month should make contrarians nervous.

Finally, outflows from bond funds stopped this month as bonds delivered positive performance. After redeeming $37.4 billion in August, bond MFs and ETFs have issued $1.7 billion in September. Bond MFs took in a hefty $8.1 billion on the past five trading days, suggesting the bond rally may lose steam over the near term.

This communication is a publication of TrimTabs Asset Management. It should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. Information presented does not involve the rendering of personalized investment advice. Content should not be construed as an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein. Performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing performance returns. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Past performance may not be indicative of future results. Therefore, no investor should assume that the future performance of any specific investment or investment strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions, may materially alter the performance of an investor’s portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor’s portfolio.

© AdvisorShares