For most of the summer, the speculation was out there. How would it end? (BTW – DVR users – no spoiler alert necessary for this article.) Which main characters, if any, would survive? TV chat boards were filled with nervousness and lots of guesses.

As the 9/29 airing of the last episode of the AMC hit, Breaking Bad, approached, the uncertainty increased. Would the ending be as unsatisfying as some of the past big TV hits (like the open-ended Sopranos or Lost, or the more recent Dexter )?

Last night we found out, and so far all the talk has agreed with my own impression – that this was the best finale we’ve seen in a very long time – or perhaps ever. So, if you haven’t fired up your DVR yet to catch the recording or if you were planning to watch one of the repeat broadcasts, watch it tonight. The rest of us can only keep mum so long in response to your pleas of “Don’t tell me, I haven’t watched it yet.”

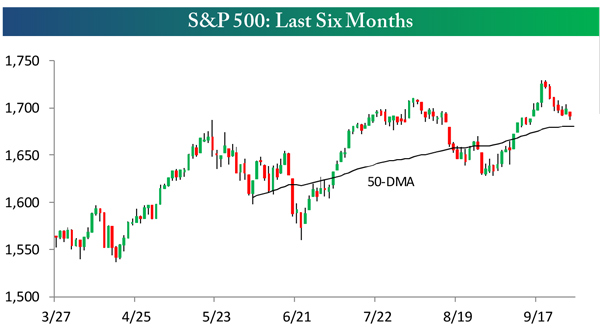

Of course, the same guessing games and uncertainty are still pervading the stock and bond markets. First, it was “Would they or wouldn’t they…taper that is?” Stocks sold off from an all-time high on August 2nd as the world waited for an answer. When the answer came, a relief rally ensued, and yet another all-time new high was registered by the stock indexes on September 18th.

Yet as we had warned in my September 16th commentary, the second half of September has not been forgiving – even when stocks have registered YTD gains, as was the case this year. Right on cue they began to fall after the 18th, and they have been falling almost ever since. Talk about Breaking Bad. When the market opened today, the Dow was quickly down over 170 points!

Source: Bespoke Investment Group

This week the blame for the latest tumble is not the Federal Reserve and its tapering, but rather the public debt dispute between the Democrat controlled White House and Senate, and the Republican controlled House of Representatives. As the voters recently rubber stamped the divided government in elections less than a year ago, I suspect the divide merely reflects the ever deepening chasm between the polarized views of the American people rather than simply that our elected officials are incompetent.

All sides say they want a solution. As when I urged caution suggesting we believe Federal Reserve Chairman Bernanke on the timing of tapering when most critics were arguing that a change in policy was a certainty, I would suggest we take the parties in the latest dispute at their word. This has happened before. The debt ceilings, the failure of the Senate to pass a budget, the need for yet another continuing resolution to keep the government funded – all this has occurred many times in our past.

Sometimes (17 times since 1977, to be exact), it has even led to a “shutdown,” but last I checked we still have a government and, yes, it (and the debt) is bigger than ever. And it does not matter which party controls the Presidency, although Republican presidents have been forced to live with a shutdown by Congress more times than their Democratic counterparts.

These shutdowns have usually lasted about three days, with the longest going 21 days. That was back in 1995. And the S&P 500 index fell 3.7%. But Medicare, Medicaid, Obamacare, the President’s and Congress’ salaries, the armed services and about 59% of the civilian government employees continue. And, of course, taxes are still due and collected.

So in this day and age a shutdown is not really a shutdown. And more importantly, when the shutdown or the debt crisis du jour is finally put to rest, the stock market gains can be substantial. In the 1995-96 shutdown, the S&P gained 10.5% in just the month after the shutdown. While the 14% lost by the Dow in the debt ceiling fight of 2011 took five months to recover, the 400 points lost to the “Fiscal Cliff” negotiations of 2012 were recovered in the first couple days of 2013.

There is, however, uncertainty looming over the markets from other quarters as well. Economic reports which had been unexpectedly better immediately after the Fed decision on the 18th, turned very sour last week. Of the 22 economic indicators released last week, only four exceeded expectations and sixteen disappointed.

At the same time, earnings reporting season for the third quarter will begin in a week or so. While broker revisions have been slightly negative, that has been the case for most of the 2009-2013 recovery and so you can’t read much into that. The real reports could provide a diversion to the political uncertainty or they could reinforce the market pessimism that seems rampant.

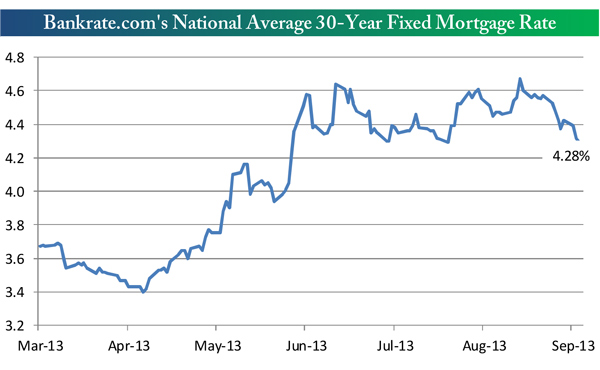

Finally, interest (and mortgage) rates continue to improve, gas prices have fallen, sentiment has moved away from overly optimistic levels, and the stock market indexes are no longer in the overbought territory that concerned us back on the 16th.

Source: Bespoke Investment Group

Perhaps the seasonal signals will provide the tie breaker and some guidance. October is normally a month in which the market changes direction. If it is headed higher, it can reverse and fall, and conversely, if it is falling, it can be a month of redemption as we move into the usually strong fourth quarter.

Normally the change in direction occurs around the middle of the month (right about the time of the debt limit deadline). It appears that stocks will be falling into that time period and that may be when prices begin to improve if history is any guide. But if a swoon does occur, it may turn around even quicker as October, like September, tends (60%-70% of the time) to be a positive month for stocks when the market is up YTD, and also when September has had a positive return.

So where does this leave us? It places us pretty much where we have been through most of this summer – looking for a short-term downturn in an on-going bull market. Yes, this time it looks like a greater than 5% fall may occur, but a settlement and an end to the uncertainty could instantly change that.

For that reason, it is once again probably a good time to invest in actively managed strategies that endeavor to keep you on the right side of the market and can react to the changing economic and political environment. Investing in such managed accounts is not the same as simply investing in the stock and bond markets. That decision does not bring with it the defensive tool kit that is included with an actively managed strategy.

Besides, if you put off investing, isn’t that the same as donning a market timer’s hat and trying to decide when to invest or not. When has that ever worked for you?

Here’s my conclusion of this riddle within a riddle: Use your gray matter and don’t be blue, turn things over to an automatic mechanism and, like the remote control to your garage, one touch will open doors for you (and I said I wouldn’t spoil it).

All the best,

Jerry

© Flexible Plan Investments