The old adage is that “generals always fight the last war.” By that measure, the United States has successfully addressed most ofthe threats that precipitated the 2008 financial crisis. The problem is that while policy makers have spent the past five years putting out the fires from the last crisis, they’ve done less to prepare for the next:a retirement crisis.

But before highlightingthe future risks to the US economy, let me take a step back and remark on what has improved since the time of the Lehman bankruptcy.

Back then, the global economy was facing the prospects of another Great Depression. That scenario was thankfully avoided, and the US financial system – the proximate cause of the crisis – is in much better shape than it was in 2008, asLarry Fink recently pointed out. Leverage levels are considerably lower and we have seen a regulatory overhaul that has left US financial institutions better capitalized and less risky. In other words, the risk of another imminent financial system crisis has likely abated.

Unfortunately, given the global economy’saging populationand slowing growth, there are two major issues that foretell a coming retirement funding crisis.

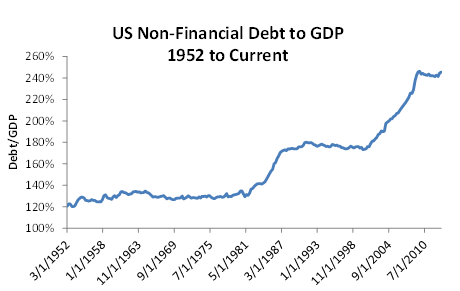

1. Government debt levels remain elevated, a troubling prospect considering that the US government has failed to address entitlement reform and an aging population will put increasing demands on state coffers. As a result of softening the blow to the household sector during the last financial crisis, most governments, and specifically the US government,have levered up their own balance sheets. US federal debt outstanding – which excludes debt held by the social security trust fund – has climbed by approximately $6.5 trillion since the Lehman bankruptcy. As a result, US non-financial debt is actually $7 trillion higher than it was five years ago. This means that, as the chart below shows, despite the “deleveraging” of the past five years, US non-financial debt now stands at 245% of gross domestic product (GDP), compared to 225% in the second quarter of 2008.

Source: Bloomberg

2. US household savings are inadequate to fund an increasingly lengthy retirement. Amid surging government debt and an aging population, future retirees may have to fund more of their retirement themselves. Unfortunately, the post-crisis savings surge predicted by many pundits has yet to materialize, and most US households can no longer look forward to a private sector pension.

The good news is that while the recovery has impressed few, it has been much better than the alternative we were all facing five years ago, and there is still time to avoid, or at least mitigate, the pending retirement crisis. The bad news is that, following five years of post-crisis reform fatigue, neither the government nor US households are showing much inclination to do so.

© iShares Blog