Intermodal Transportation: Finding Value in a Growing Segment of the Transportation Industry

Intermodal Transportation: Finding Value in a Growing Segment of the Transportation Industry

As intrinsic value based investors, we view growth as a potential source of value for shareholders; however, we are careful not to overpay for it. Intermodal shipping is one of the fastest growing modes of domestic freight transportation, and also an area where we have found two companies trading below our estimates of their respective intrinsic values.

Intermodal shipping is the movement of a single shipment by more than one method of transportation. For this discussion, we are referring to rail intermodal, which involves moving freight by rail for the long-haul portion of the trip and by truckload to and from an intermodal terminal.

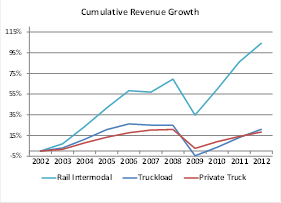

Source: Wolfe Research

Cost Advantages

Intermodal shipments have a cost advantage relative to truckload-only deliveries on shipments traveling long distances. The distance traveled by an intermodal shipment is typically greater than 500 miles, allowing rail labor and fuel efficiencies to more than offset the additional miles the shipment must travel to and from rail terminals. One train can carry up to 300 or more containers, which is equivalent to the same number of truckloads. As a result, less labor and fuel are needed per ton of freight moved on the rail portion of the journey. Transporting freight on a train carrying 300 containers is three-to-four times more fuel-efficient and far less labor-intensive than moving the equivalent amount of freight via hundreds of truckloads.1

Intermodal has grown more rapidly than truckload over the last 10 years as higher fuel prices increased the cost advantage of long-haul rail relative to truckload while better and more predictable service levels addressed the primary barrier to using the lower cost service.

Source: ATA U.S. Freight Transportation Forecast to 2024

Opportunity to Gain Market Share

We believe the trends creating this modal shift are likely to persist and intermodal will continue to take share from truckload for the foreseeable future. The size of the opportunity is large. In 2012, the size of the domestic truckload2 industry was around $600 billion in revenue compared to the domestic intermodal industry of under $15 billion.3 Due to the size of the respective modes, intermodal does not need to take much share from truckload to create meaningful volume growth for the providers of intermodal services. U.S. railroad management teams have cited opportunities to double or triple the current size of the domestic intermodal industry from share shift alone. These management teams have been acting accordingly by investing billions of dollars on new intermodal terminals, tracks, and tunnels. These investments are critical to maintaining and improving service levels. Improved services levels and on-time performance have been vital to persuading shippers to shift to intermodal in recent years. Maintaining this level of service will be important to achieving further share gains.

Pricing Power

We anticipate further market share gains for intermodal and an improvement in pricing power over the next several years as accelerating inflationary pressures negatively impact truckload competitors. Drivers, equipment, and maintenance represent close to half of a truckload provider’s cost structure. Progressively more onerous emissions regulations are increasing the cost of engines and trucks while the pool of qualified drivers is shrinking due to new methods of measuring driver safety. A shrinking pool of drivers in an industry that suffers from 100% turnover threatens to increase labor expenses. Finally, regulatory changes implemented in July 2013 will further restrict the number of hours per week a driver may be on the road. These changes are likely to further reduce driver and equipment productivity. Truckload carriers have been hesitant to increase pricing enough to offset these cost pressures and we believe this lack of pricing power is unsustainable. In a recent issue of Transport Topics the president of one of the largest truckload providers states a truck carrier should generate a 10% operating margin, but laments that the industry average is currently 2%. These margins make it difficult for carriers to justify investing the $50 billion necessary to return the industry’s aging fleet to its historical average age.4 In our opinion, truckload pricing needs to increase materially to justify such a large re-investment in the fleet. Material price increases by truckload carriers should only enhance the relative position of intermodal.

HUBG and PACR – Poised to Benefit

We believe Hub Group, Inc. (HUBG) and Pacer International, Inc. (PACR) are two companies poised to benefit from these industry trends. Both companies derive a significant percentage of their operating income from intermodal marketing services. The primary role of an intermodal marketing company (IMC) is to manage the movement of intermodal containers throughout the entire journey. Hub Group and Pacer hold strong competitive positions as two of the four largest IMCs. Size is important to an IMC due to advantages of scale as well as cost and service benefits that emanate from being an important partner to the rails. As a result, the top four IMCs represent roughly 70% of the domestic intermodal marketing industry5. We find this industry structure appealing.

In our opinion, the current share prices of Hub Group and Pacer do not fully reflect the long-term earnings power of the businesses. First, the businesses are well-positioned in an industry that provides attractive opportunities to reinvest cash flow. And given the relatively low capital intensity of their business models, the companies should generate sufficient cash to reinvest in the business and still have additional cash available to allocate opportunistically to share repurchases, dividends, and acquisitions. Second, we believe operating margins are likely to expand due to improved pricing power and, in the case of Pacer, improved results from underperforming business segments. Third, both companies have solid balance sheets providing financial flexibility and the ability to navigate cyclical downturns. All of these factors lead us to long-term earnings projections and intrinsic value estimates indicating attractive investment opportunities with an acceptable margin of safety.

The views expressed are those of the analyst as of September 2013, are subject to change, and may differ from the views of other portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice.

1 Sources: Association of American Railroads, Wolfe Research

2Includes both for-hire truckload services and private trucking fleets

3Source: ATA Freight Transportation Forecast to 2024

4Bearth, Daniel P. “Carriers Say Profit Growth is Limited by Rising Costs, Slow Gains in Demand” Transport Topics July 22, 2013: A3-A4. Print.

5Source: Wolfe Research

© Diamond Hill Investments

© Diamond Hill Capital Management