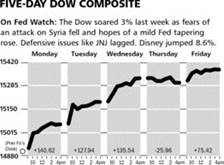

Stocks rallied last week as military options in Syria no longer look likely given the disapproval of the American people and Congress. Additionally, this embarrassing agreement reached with Russia is an admission that the USA will not intervene.

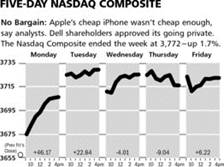

As a result, stocks did well as evidenced by the above graphs. Last week the Dow Jones Industrial Average gained nearly 3% led by our shares of Boeing while the NASDAQ Composite moved higher by 1.7%. The latter’s performance held back by disappointment with Apple’s latest product announcements.

The Market & Economy

As indicated above, last week (and this upcoming week for that matter), was dominated by macro issues concerning military options in Syria. This impacted the price of oil as well as interest rates, and caused markets to focus on matters which are largely unpredictable (look at US policy changes for instance) and subject to change.

The United States after months of saber rattling (along with many of our allies), have now sent a very strong signal that there will be no intervention in Syria, and I dare say anywhere else for the foreseeable future. The stock markets like the absence of war and the uncertainty it brings - at least until something worse happens.

This morning’s action in stocks is very strong to the upside. This comes as President Obama’s preferred favorite to take over the Chairmanship of the Federal Reserve Board has withdrawn his name due to objections from Obama’s own party. Does the phrase “lame duck” mean anything to anyone? Financial markets applaud not only the decision to keep Obama’schoice off the Fed, but also the notion that the President’s power in general, to shape events, is falling as quickly as his poll numbers.

It’s too bad that market commentaries are dominated by politics and worldwide events such as the civil war in Syria, but that is the world we live in and it is not likely to change anytime soon.

Right or wrong, the financial markets view this past weekend’s events as bullish. The rationale is that we now have a higher likelihood of continued dovish monetary policy which has treated stocks so well. Markets are also cheering a lessening in government interference in the economy via edicts emanating from Washington DC. We shall see how long that sentiment lasts, but for now the stock and bond markets love it.

What to Expect This Week

There is a two-day Federal Reserve Open Market Committee meeting which ends Wednesday afternoon. It is expected that the Fed will announce an adjustment to its monthly buying of assets from $85 Billion dollars to just $75 Billion. This is mostly technical as the federal government’s deficit has shrunk to around $800 Billion dollars per year. Thus, the new lower total still offsets COMPLETELY the spending deficit in DC.

In other words, monetary policy is about as loose as it gets. Any looser and we would be out-and-out monetizing our federal deficit with freshly issued pieces of paper whose value someday may be worth very little. This is another reason that buying shares of companies in strong cash generating businesses is a hedge against the long-term implications of this absurd policy which we are now stuck with.

Additionally, this coming weekend Germany holds national elections. The financial markets assume the current government will be given another five years. Any other outcome will introduce more uncertainty into Europe and the global economy.

My view is that once Chancellor Merkel gets another five years the problems in Europe which have been swept under the rug will emerge just as the problems facing the US came out only after last year’s November elections.

Back in the real economic world, the news on the economy remains mixed. Retail sales last week were weak as was industrial production this morning. On the other hand, the USA’s coming energy independence is such a bullish factor that America’s slow-growth economy remains the envy of the world.

A quick look at the weekly Economic Cycle Research Institute’s leading indicators show more of the same. There is no indication of recession and perhaps even a hint of uptick despite the recent jump in interest rates and oil prices.

While the Fed meeting is the big item for the week, the dovish implications of the new Chairman has largely stolen some of that impact in this morning’s trading.

![]()

SYMBOL VOD

Verizon completed the largest bond offering in corporate history last week, which will be partially used to help fund its acquisition of the 45 percent stake in Verizon Wireless that is controlled by Vodafone. The offering was $45 billion, which nearly tripled the size of the previous largest debt sale. There was an enormous appetite for this deal as investors continue to want yield in these current market conditions. This is a positive for shareholders of Vodafone, as any questions about Verizon’s ability to finance the acquisition have been put to rest.

Vodafone continued to trade higher last week, and is at a new 52-week high this morning. We believe this deal will close on schedule, and expect investors will continue to buy up shares of Vodafone as the Company announces its expansion plans in Europe. Vodafone remains a core holding for all of our clients and we are encouraged by the recent announcements.

![]()

SYMBOL: BA

Last week Boeing announced that they are boosting their plane deliveries to Chinese customers by 50 percent this year to meet robust demand for airlines in the country. The Company will now ship more than 120 aircrafts to Chinese airlines, up from 80 planes last year. This is the fourth year in a row that the management team has increased demand estimates for shipments to the region, and we expect the trend to continue for the next several years as the growth of the Chinese economy is spurring more demand for air travel.

Shares of Boeing have been a market leader during the recent rally, and the shares traded at multi-year highs this morning. The growing demand in China and the Company dealing with its lingering issues with the Dreamliner have the stock poised for another move higher. Several analysts on Wall Street raised their estimates last week, and we look for the shares to reach $150 within the next 12 months.

© McIntyre, Freedman & Flynn