Dear Reader,

SAY IT ISN’T SO

InvestmentNews headline … “Ex-J.P. Morgan broker: Firm pushed house funds.” The story went on to report:

“Claims reps didn’t get commission on trades of outside funds. A former J.P. Morgan broker has filed an arbitration claim alleging that the bank’s securities unit encouraged sales of proprietary funds by withholding commissions from brokers on trades of outside funds….

“Mr. Tchan also claimed that the bank brokerage used financial planning software to direct clients into proprietary products… Mr. Tchan claims that a few weeks after he complained about the supervisory system last fall, his direct supervisor and a compliance official confronted him about switches he made from proprietary stock mutual funds into nonproprietary bond funds.”

YOU REALLY DON’T NEED TO KNOW BUT …

From my friend Peter:

- A snail takes 115 days to travel a mile (makes me feel good!).

- The great horned owl is the only animal that eats skunk (no accounting for taste).

- A pigeon’s feathers weigh more than its bones (there’s my weight problem).

- Cats can’t taste sweet things (but they do like mice).

- The average lifespan of an American dollar bill is eighteen months (not in my pocket).

- An Armadillo CAN be housebroken (so if you’re looking for a replacement for your dog…).

- Glass is the only substance known to get stronger the longer it’s under water.

- If you have at least 5/8 of a torn dollar bill, it can be redeemed at full value (as long as it’s before 18 months).

- A rattlesnake can bite you up to an hour after it’s dead (hot dog!)

- There are 2,598,960 possible hands in a five-card poker game (well, that explains it).

- Telephone poles in Uganda and Kenya are much higher, to allow for the height of giraffes (and they appreciate it).

- The average human sheds 40 pounds of skin in a lifetime (I wonder if I can speed it up?)

KEEP IT IN MIND

On occasion I’ve had a client respond to my belief that investment returns will be relatively modest with, “But I need x%!” As tactfully as I can, I respond, “The markets don’t give a damn.” Tough medicine, but planning on reality is likely to be a lot safer than planning on the pot of gold at the end of the rainbow. Or as Margaret Mitchell ( Gone With the Wind ) wrote, “Life is under no obligation to give us what we expect.”

WOW!

The DailyGalaxy reports that researchers from the University of Central Lancashire report the discovery of a “large quasar group” (LQG) with a mass two billion times that of the sun and it’s BIG – it “would take 4 billion years to cross at the speed of light.”

IRASCIBLE

“Irascible investing legend John Bogle…” That’s how on wall street introduced its story on Jack and his comments regarding target-date mutual funds. At the 25th annual Morningstar Investment conference he said, “… I think target-date funds have too narrow a mandate. You have to think about your entire target-date environment.” The article went on to say, “Bogle’s contrarian perspective casts doubt on a retirement product employed by a significant portion of the investing public. Target-date funds have grown in popularity, especially among younger investors, and these funds now hold 13% of total 401(k) assets, according to a recent analysis by the Employee Benefit Research Institute and the Investment Company Institute.”

I have no ideas why Jack’s comments are contrarian as any competent planner knows it’s the investor’s entire financial picture that counts (e.g., Social Security, pensions, part-time work), not just investments, especially not just the portion in their retirement plan. If stating the obvious, i.e., beware of target date funds, makes Jack irascible, I say “go for it”!

NEW SPEAK

In George Orwell’s NineteenEighty-Four the totalitarian regime in control of the government developed “Newspeak,” a fictional language designed to limit free thought. For example, Crimethink is the Newspeak word for thought crime (thoughts that are unorthodox or outside the official government platform) and joy camp was a forced labor camp. So when I read about Rep. Ann Wagner introducing a bill that would stop the Department of Labor from proposing fiduciary regulations until 60 days after the SEC issues its fiduciary proposal and calling it “ the Retail Investor Protection Act,” Newspeak immediately came to mind. As it seems the SEC fiduciary proposal issue date may be “never,” it’s a very Machiavellian way of killing the fiduciary movement.

GOING MAINSTREAM

I’ve written on a few occasions about 3D printing in past NewsLetters. Now, according to the research firm Gartner, 3D printing is going mainstream. PC Today quotes the firm’s research director opining, “The hype leads many people to think the technology is some years away when it is available now and is affordable to most enterprises.” Stick with me and I’ll keep you ahead of the curve.

OUCH!

The “Tax Attractiveness Index” was developed by two German economists and was designed to reflect a country’s tax environment. According to a story in Forbes, the index is based on an evaluation of 100 countries over a period from 2005 through 2009. How did the U.S. fair? The article’s headline says it all. “U.S. Tax System Ranks 94th out of 100 – Right Below Zimbabwe.” http://www.forbes.com/sites/robertwood/2013/07/12/u-s-tax-system-ranks-94th-out-of-100-right- below-zimbabwe/.

PET PEEVE

For years Deena and I had been listed (along with many friends from around the country) on the Worth magazine Top Planner list. Then a few years ago everyone we knew (including us) disappeared, only to be replaced almost exclusively by brokers from national brokerage firms. We never could quite figure out what had happened. Now, thanks to a recent piece in “The Prudent Investment Adviser Rules” by the Watkins Firm, an Atlanta law firm, we know. We didn’t pay!

All advisers want favorable publicity, but these so-called “best of the best” lists raise a number of potential problems. “Barron’s” publishes a number of these lists. “Barron’s” disclosure that only those advisors who pay a fee are eligible for inclusion on their lists raises a number of issues for advisors named to such lists. The omission of industry leaders such as Harold Evensky, Ross Levin and Louis Stanasolovich speaks volumes to investment and financial planning professionals, but not so to the readers of “Barron’s” who might rely on such lists in choosing a financial adviser.

I CAN SURE RELATE

The following was a lament on Gizmodo.

“I have absolutely no idea how I’m going to explain to my future kids what life was like before the Internet. Those stories of a pre-YouTube, pre-Wikipedia, pre-Google, pre-iPhone, pre-iPad day will be the modern day equivalent of my parents’ stories about walking a mile to school barefoot in the snow with two barrels of water and a fresh chicken attached to a stick going uphill there and uphill back.

“It’s crazy to think that people—actual people with actual brains—did things like keep an encyclopedia set on their bookshelf to look things up or used paper maps. We were so crazy.” http://gizmodo.com/what-we-did-before-the-internet-749948264. Of course the author forgot to add that it was snowing on the way to school, 100 degrees on the way home and uphill both ways.

THE BEST OF TIMES

From my friend Fran, this is for any of you who grew up (or remember) the 50’s and can relate to the Gizmodo lament. For you, it’s a must see. http://www.youtube.com/watch_popup?v=sDc0ID6PJeg&feature=youtu.be

SOBERING

PRODUCTIVITY?

Doesn’t look like it. According to Flurry Analytics, consumers now spend more than two and a half hours per day using mobile devices. Here’s the main usage:

|

Games |

- 32% |

|

|

- 18% |

|

Entertainment |

- 8% |

|

Social networking |

- 8% |

SPARKLE & SHINE

In case you missed it, the jewelry designer Roberto Coin (Deena’s favorite) now offers women’s shoes with 18-karat white gold, diamonds and emeralds for only $4,980.

THE NEED FOR SPEED

Moving from really big to really small numbers, Money ran an ad for CDW touting its High Performance Computing. It seems it’s critical when a one-millisecond trading advantage can be worth $100 million to a major brokerage firm. So far the fastest trade was 124 microseconds. Keep that in mind next time you decide to day trade.

WHO KNEW?

Speaking of big, Reader’sDigest reports “They Outdo Outer Space.” It seems that the number of permutations within a deck of cards is 8 X 1067. That means there are more combinations than stars in the Milky Way!

THE BIG BOYS

Institutional Investors recently ran a list of America’s Top Money Managers and while perusing the list I realized we have relationships with quite a few. Our current universe includes #1 (Blackrock), #6 (JP Morgan), #10 (Goldman), #25 (Natixis), and #30 (DFA). At different times we’ve also used #2, #4, #5, #17, #20, and #28. I’ll let you know when we one day make the list on our own. It may take a while as #100 (Teachers Retirement System of Texas) manages just over $47 billion. In the interim it’s nice to know we are big enough to access and leverage the talents of these “big boys.”

GET A JOB

If you know a law student (or student-to-be), let him or her know about “Law Jobs: By The Numbers.” It allows you to determine a law school’s graduate employment rate. You can even customize the search criteria (e.g., full-time/part-time; Bar passage required).

http://educatingtomorrowslawyers.du.edu/law-jobs

WHO DO YOU LISTEN TO?

Money magazine quizzed its readers and asked “Who has been your most influential money advisor?” It found:

24% - Broker or financial planner 19% - Parent

11% - TV host/financial author

Needless to say, I’m rooting for 100% financial planners.

GOOD NEWS

After the graphs I posted earlier I thought you’d like some good news, so here it is …. We’re still here!!

For centuries, going back at least to the Mayans, Nostradamus, and Isaac Newton, predictions about the end of the world have flourished. If you’d like to see “All of the Failed Predictions of When the World Will End,” check out this cool infographic from the design firm Accurat.

http://www.popsci.com/science/article/2013-07/centurys-worth-times-world-didnt-end-infographic

CAVEAT EMPTOR

I just finished listening to a lecture as part of my continuing education requirement to maintain my Accredited Investment Fiduciary (AIF) designation. Most disturbing was a discussion regarding misleading marketing in the 401K universe. As outrageous as some of the stories were, nothing compares to the position some firms take if, despite all of their efforts, they are found to be ERISA fiduciaries. Below is one of the examples provided in the lecture:

If you’re responsible for a pension plan, you better be sure you know whose pocketbook is at risk if there is a problem. If you’re not careful, it’s likely to be yours.

DISRUPTIVE

I’ve written a few times about 3D printing and it seems the technology is indeed likely to result in major business disruptions. According to Gartner (an information technology research and advisory company providing technology related insights to CIOs and senior IT), “3D printing is disrupting the design, prototyping, and manufacturing process in a variety of industries.” As reported in PCToday, “If your enterprise isn’t already testing the technology as a way to improve product design and prototyping, it’s time to start.” It turns out the future is here, now.

PRETTY EXCITING

I’ve been involved in the development of the CFP (Certified Financial Planner) designation for decades, so it’s exciting to see how far it’s gone. Here’s the latest: to date, the CFP Board has recognized 343 programs, with another 51 currently in development. Of the active programs, 177 grant certificates to students, 112 confer undergraduate degrees, and 54 are graduate-level offerings, including five doctoral programs.

LISTEN TO THE LAUREATE

As readers of my NewsLetter know (probably all too well) one of my major soap box issues is the low return environment I believe investors will be living in for decades. As a result we believe that a major focus of planning needs to be the management of expenses. So, I was pleased to see Nobel Laureate Professor Sharpe’s conclusion in a recent FinancialAnalystJournal article, “The Arithmetic of Investment Expenses.” Comparing the impact of expenses on an investor’s standard of living by comparing terminal wealth for investing in different funds with different expense ratios he found “…those who choose low-cost investments could have a standard of living throughout retirement more than 20% higher than that of a comparable investment in high-cost investments.” Expenses matter!!

FINGERS CROSSED

JPMorgan’s Dimon predicts strong U.S. economy ahead

JPMorgan Chase CEO Jamie Dimon says the U.S. economy is well on the way to recovery. Despite the possibility of interest rates rising and volatility occurring as a result of the normalization of interest-rate policy, Dimon says the economy will continue to grow and thrive.

Source: CNBC

I’LL KNOW WE’RE BIG WHEN…

I recently saw a headline in the Wall Street Journal that read “Glencore Takes a $7.7 Billion Charge.” I’ll know we’re a really big firm when we can write off $7.7 billion and not bat an eyelash. Of course the market reacted strongly; the stock dropped a “whopping” 1.6%. Hey, what’s a billion here or there? I just love Wall Street.

NOT ALL THIEVES ARE STUPID

Here are some pretty sobering stories. Thanks to Burt for this. Fore warned is fore armed.

- Some people left their car in the long-term parking at San Jose while away, and someone broke into the car. Using the information on the car's registration in the glove compartment, they drove the car to the owner’s home in Pebble Beach and robbed it. So I guess if we are going to leave the car in long-term parking, we should NOT leave the registration/insurance cards in it, nor the remote garage door opener.

- Someone had a car broken into while at a football game. The car was parked on the green which was adjacent to the football stadium and specially allotted to football fans. Things stolen from the car included a garage door remote control, some money, and a GPS which had been prominently mounted on the dashboard. When the victims got home, they found that their house had been ransacked and just about everything worth anything had been stolen. The thieves had used the GPS to guide them to the house. They then used the garage remote control to open the garage door and gain entry to the house. The thieves knew the owners were at the football game, they knew what time the game was scheduled to finish, and so they knew how much time they had to clean out the house. Something to consider if you have a GPS — don’t put your home address in it… Put a nearby address (like a store or gas station) so you can still find your way home if you need to, but no one else would know where you live if your GPS were stolen.

- This lady’s handbag, containing her cell phone, was stolen. Twenty minutes later when she called her husband from a pay phone telling him what had happened, he said, “I received your text asking about our PIN and I replied a little while ago.” When they rushed down to the bank, the bank staff told them all the money already had been withdrawn. The thief had actually used the stolen cell phone to text “hubby” in the contact list and got a hold of the PIN. Within 20 minutes he had withdrawn all the money from the bank account. When sensitive info is being requested through texts, CONFIRM by calling back. [Josh say’s that most banks have a limit so it’s likely only to apply up to $500, depending on the bank]

- A lady went grocery shopping at a local mall and left her purse sitting in the child’s seat of the cart while she reached something on a shelf… wait until you read the WHOLE story! Her wallet was stolen, and she reported it to the store personnel. After returning home, she received a phone call from the Mall Security to say that they had her wallet and that although there was no money in it, it did still hold her personal papers. She immediately went to pick up her wallet, only to be told by Mall Security that they had not called her. By the time she returned home again, her house had been broken into and burglarized. The thieves knew that by calling and saying they were Mall Security, they could lure her out of her house long enough for them to burglarize it.

DID YOU KNOW?

I didn’t until I got a note with a whole list of “The Top 10” from my friend Peter.

- The U.S. didn’t even make the list for drinking; Italy was #1, followed by Spain, France, and Mexico.

- We also didn’t make the list for longest lived. Andorra (wherever that is) was #1 at 83½, followed by San Marino, Japan, and Singapore (80.7).

- We even missed the most coffee drinking. Finland was first at 1,686 cups per capita followed by Denmark and Norway (I assume it’s hot coffee. It’s COLD up there). France was #10 at 831 cups.

- We just barely made the Top 10 in chocolate consumption coming in at #10, less than 1/2 the consumption of #1 Switzerland.

- We did however make #3 in most ice cream consumption at 33 pints per capita, following New Zealand and Australia at #1 (44.3 pints).

- Finally, we are #1 with “Most airports” at 14,695. To my surprise Brazil was #2 with 3,365.

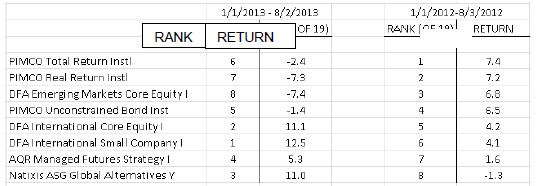

WHAT A DIFFERENCE A YEAR MAKES

Occasionally I get asked why we don’t fire “underperformers.” Well, in early August I was reviewing our manager year-to-date performance and decided to see how some compared to their prior year performance. Here’s what I found:

Had an investor used some of the four top performers from 2012 to invest equally in 2013, the 2013 return would have been -4.6% versus +2.7% had they invested equally in all eight funds. Had they used the four worst performers in 2012 to invest in 2013, the return would have been +10%. Buying yesterday’s hot fund and firing yesterday’s underperformer usually results in buying high and selling low.

MUST READ

If you’ve been reading my NewsLetter for long, you know that I consider Jason Zweig, personal finance columnist at the WallStreetJournal, to be among the best of the best. His recent column “The Intelligent Investor: Saving Investors From Themselves,” is an excellent example of why I think so highly of Jason. Here’s a snippet from the column, but I encourage you to follow the link and read the whole story.

I was once asked, at a journalism conference, how I defined my job. I said: My job is to write the exact same thing between 50 and 100 times a year in such a way that neither my editors nor my readers will ever think I am repeating myself.

That’s because good advice rarely changes, while markets change constantly. The temptation to pander is almost irresistible. And while people need good advice, what they want is advice that sounds good.

The advice that sounds the best in the short run is always the most dangerous in the long run. Everyone wants the secret, the key, the roadmap to the primrose path that leads to El Dorado: the magical low-risk, high-return investment that can double your money in no time. Everyone wants to chase the returns of whatever has been hottest and to shun whatever has gone cold. Most financial journalism, like most of Wall Street itself, is dedicated to a basic principle of marketing: When the ducks quack, feed ’em.…

My role is also to remind them constantly that knowing what not to do is much more important than what to do. Approximately 99% of the time, the single most important thing investors should do is absolutely nothing.

http://blogs.wsj.com/moneybeat/2013/06/28/the-intelligent-investor-saving-investors-from-themselves/

LAWS

If you’ve ever wondered how the world works, here are a few Laws to help guide you:

- Supermarket Law – As soon as you get in the shortest line, the cashier will have to call for help.

- Variation Law (related to Supermarket Law) – If you change lanes, the one you were in will always move faster. I hate to think about how many times I’ve tested and proven these laws to be true.

- Law of Probability – The probability of being watched is directly proportional to the stupidity of your act.

- Law of the Result – When you try to prove to someone that a machine won’t work, it will.

- Law of Physical Appearance – If the clothes fit, they’re ugly.

AND MORE LAWS

According to Reader’s Digest, these are for real!

- Missouri – It’s illegal to drive with an uncaged bear. Phew! I feel safer already.

- Connecticut – It’s illegal to call a pickle a “pickle” if it doesn’t bounce. Of course, that begs the question

– how high?

- Nevada – It’s illegal to wage war against Nevada citizens. I guess it’s okay to wage against other states’ citizens.

EVEN MORE “THE FUTURE IS HERE”

Below is a picture of the Tesla (electric car) factory where 160 robots are hard at work. As the picture really doesn’t capture the jaw dropping reality, take a look at the video.

http://www.slashgear.com/tesla-model-s-factory-tour-shows-elon-musks-robot-army-17290737/

COOL SITES

I get a constant barrage of emails suggesting links to interesting sites. Here are a few worth checking out.

- Cool Ride – http://www.youtube.com/watch_popup?v=KcuDdPo0WZk

- When Geeks & Engineers Get Together – https://www.facebook.com/photo.php?v=1408483329373078&set=vb.206177085133&type=2&theater

- Best of Times (for old fogies like me) – http://www.youtube.com/watch_popup?v=sDc0ID6PJeg&feature=youtu.be

- My Shoes – http://www.youtube.com/embed/SolGBZ2f6L0

- Landfillharmonic Orchestra – http://www.youtube.com/watch_popup?v=UJrSUHK9Luw

- Night Sky – http://newswatch.nationalgeographic.com/2013/06/11/new-night-sky-timelapse-video-stars- and-storms-vie-for-attention/

- Onze helden zijn terug! – http://www.youtube.com/watch?v=a6W2ZMpsxhg&feature=player_embedded

- How Does He Do It? – http://www.flixxy.com/worlds-fastest-magician.htm

- A Store Front in Berlin – http://www.youtube.com/watch_popup?v=XVTga6GmbGw&vq=medium#t=74

DR. FIELDS COMES THROUGH AGAIN

CHILDREN ARE QUICK

TEACHER: Why are you late?

STUDENT: Class started before I got here.

I’m surprised one of my PhD students hasn’t tried that.

TEACHER: Glenn, how do you spell “crocodile?” GLENN: K-R-O-K-O-D-I-A-L.

TEACHER: No, that's wrong.

GLENN: Maybe it is wrong, but you asked me how I spell it. I wish I’d thought of that years ago.

TEACHER: Donald, what is the chemical formula for water? DONALD: H I J K L M N O.

TEACHER: What are you talking about? DONALD: Yesterday you said it’s H to O.

TEACHER: Millie, give me a sentence starting with “I.” MILLIE: I is…

TEACHER: No, Millie… Always say, “I am.”

MILLIE: All right… “I am the ninth letter of the alphabet.”

TEACHER: George Washington not only chopped down his father’s cherry tree, but also admitted it. Now, Louie, do you know why his father didn’t punish him?

LOUIS: Because George still had the axe in his hand… …A Wise Dad.

TEACHER: Now, Simon, tell me frankly, do you say prayers before eating? SIMON: No sir, I don’t have to. My Mum is a good cook.

There’s no point in wasting a good prayer.

TEACHER: Clyde, your composition on “My Dog” is exactly the same as your brother’s. Did you copy his?

CLYDE: No, sir. It’s the same dog.

TEACHER: Harold, what do you call a person who keeps on talking when people are no longer interested?

HAROLD: A teacher.

And I didn’t even pick the name of the student.

I’M SHOCKED

Unfortunately, I’m really not shocked, but the results are sobering. According to a survey of Wall Street employees by the law firm Labaton Sucharow:

“In this second annual survey of the US financial services sector, we uncovered astonishing data about the state of our markets and, notably, an abject decline in the three forces that, individually and together, have the power to serve as safety nets for the economy: individual integrity, leadership and corporate culture.” Highlights from the survey include:

- 25% said they would engage in insider trading if they could make $10 million, if they felt they could get away with it.

- Of younger employees, 38% would do so.

- 29% felt that success in the industry required unethical or illegal behavior.

- 26% said their comp structure incentivizes unethical or illegal behavior.

- 40% felt they have been rewarded for ethically troubling actions.

- 31% felt they had been penalized for refusing to engage in such behaviors.

Don’t forget to ask for a copy of the Committee for the Fiduciary Standard Fiduciary Oath if you, your friends, or your firm are ever considering employing a non-fiduciary financial advisor (i.e., a broker). Let us know if you’d like a copy ([email protected]).

TRAVELING?

If you’re headed up north and want to relax, check out “1862 Seasons on Main” in Stockbridge, Mass. Recently opened by friends of E&K, here’s how they describe it:

It is a beautifully fully restored INN which is a 150 year old home at 47 Main Street in Stockbridge (the town that Norman Rockwell lived in his last 25 years) and rates a 100% EXCELLENT rating on Trip Advisor (be sure and check out the video).

We have made some wonderful additions since the video came out, such as adding a four-hole putting green out back, a massage room right near the bedrooms, a seven reclining seat entertainment center with a 70-inch flat screen TV and an old fashioned pool table and popcorn machine. We loan out kayaks, lawn chairs, ice chests, and blankets for the famous Tanglewood performances. We are getting well known for our completely served elegant full breakfasts, served on fine china in our dining room. We host ice cream socials every night after the shows. From 4-6 p.m. daily we have complimentary cocktail hours with wine, beer, cheese, fruit, nuts, sweets, etc. There is free tennis across the street, with walking and bike trails outside our door and two live theatres two blocks away. There are shopping discounts in town (two blocks away) for our patrons. Six restaurants are within walking distance. Delicious local chocolates and fresh baked rugelach are available upon arrival, and other pastries are baked from scratch daily. Nightly turn down service is available. All bedrooms have a private bath. We have free washer/dryers in house for our guests’ use. Fresh coffee, juice, and water are available 24/7. We provide the daily local newspaper. Free private and street parking is available for our guests. Work out mats, yoga mats, umbrellas, and any special dietary needs are covered.

We’re sold and hope to visit there in the not too distant future. Maybe we’ll see you there.

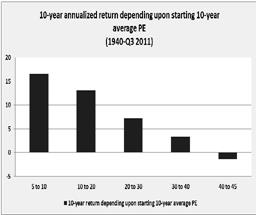

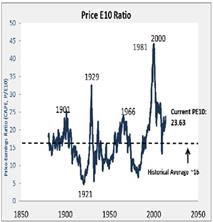

MORE ON BONDS

It’s no surprise that interest rates are historically low and there’s risk to bond values if (or more realistically, when) yields move up. As a result there is widespread concern regarding bond allocations with some commentators recommending the complete elimination of bond investments. I don’t have the room in the NewsLetter needed to go into any detail about why this is a seriously BAD recommendation (if you’d like to drop me a note or call, we can chat in depth) but in a JournalofIndexes article, “Taking a Long View of Bond Performance,” Professor Craig Iraelsen does a good job of framing reality.

His conclusion, “Completely avoiding any asset class in a diversified portfolio amounts to a guess that it will underperform and that another asset class will outperform. Building prudent portfolio is not [Craig’s emphasis] about guessing and timing, it’s about broad diversification. A broadly diversified portfolio is naturally insulated not completely, but largely – from the normal swings in performance among its various components. The “underperformance” of one or several of its ingredients will not sink the performance of the overall portfolio.” Well said!

APROPOS OF NOTHING…

…but I thought it interesting. From gizmodo.com via Zite (an iPad App) “What are the Most Famous Brands from Each State?” Not sure how I feel about Florida’s “most famous.”

http://gizmodo.com/what-the-most-famous-brands-are-from-each-state-568455852

THE REST OF THE WORLD

We’re occasionally asked why we have significant international allocations. There are lots of reasons, but the following statistics from a Tiburon research study explains a good deal of the “why.”

Worldwide Consumers by Country

|

China |

20% |

|

India |

17% |

|

U.S. |

5% |

|

Brazil & Indonesia |

3% (each) |

|

Everyone else |

52% |

We’re not alone. For example, Citigroup has a presence in 160 countries, up 100 since 2003.

A NEW WORLD

The Journal of Indexes recently noted a few items that highlight how topsy-turvy our investment universe has become:

- MSCI (“MSCI is a leading provider of investment decision support tools to around 7,500 clients worldwide” and the manager of the primary international indexes) reclassified Greece as an emerging market. I wonder what Aristotle would say about that? “Vanguard suffered net outflows in June, marking the first time in nearly 20 years that the firm had investors pull more money out than they put in…”

I HAD TO SHARE

The online WallStreetJournal recently ran a story “Advisor couples who live, work together – For many people, the idea of working alongside a spouse is, well… it’s just too much time together. Still, some financial advisers have found the perfect business partner is the one they go home with at the end of the day.” As Deena and I were one of the three couples listed (and the other two are friends) it was pretty cool, so I can’t help but share.

“Evensky & Katz Wealth Management, Coral Gables, Fla. and Lubbock, Texas, nearly $800 million in assets under management. First comes financial planning, then comes marriage. When Ms. Katz joined Mr. Evensky’s Florida-based firm in 1990, their relationship was purely professional. When he flew to Illinois to offer Ms. Katz support when her mother was dying, she “began to see him in a different way.” They were married in 1991. …Advice for working with a spouse, ‘Make sure you really like each other,’ says Ms. Katz. ‘It's double the work’ of a regular marriage, ‘because you see each other in all environments and all situations.’ Do they plan to retire at the same time? ‘Yes,’ says Mr. Evensky, ‘which is never.’”

While I’m bragging, why stop? In the 15th Anniversary Issue of Investment News covering the moments that have shaped the financial advice industry was a story “…about the most influential advisors of the last 15 years.” Touted as among “15 transformational advisors,” my partner Deena and I were proud to be included in the list. Also, we were recently notified that we have received the Financial Planning Association “Heart of Financial Planning Award.” This award recognizes “professionals who engage in extraordinary work, contributing and giving back to the planning community and public through financial planning.”

As always, I hope you have enjoyed the NewsLetter. Please drop me a note or give me a call (305 448-8882 x235) if there are any of these tid bits (or anything else) about which you’d like to chat. If you’re not currently on my NewsLetter email list or you have a friend who would like to be added, just text EVENSKYKATZ to 22828.

Cordially yours,

Harold Evensky, CFP®, AIF® President

© Evensky & Katz

© Evensky & Katz / Foldes Financial Wealth Management