Key Points

- Investors often need to look through near-term noise to make good decisions. Uncertainty and volatility are currently elevated but in the background the economy is showing signs of picking up speed. Those willing to brave some bumps should benefit in the longer term from the improving economy.

- The potential for military action in Syria has dominated discussion in Washington but attention will soon turn toward budget and debt ceiling issues. Down the street, the most anticipated Fed meeting in quite some time is next week, with some tapering of its quantitative easing program expected.

- Japan is facing a decision on a tax hike while still pursuing quantitative easing, while Europe faces some near-term events that could increase volatility. China seems to be reverting to some old habits that could cause near term gains while papering over longer-term concerns.

Often it's the unknown that can have the most impact on markets in the short term. Syria has grabbed the attention of traders and politicians alike. But it's not the only uncertainty factor at play presently. Fed tapering, Washington's debt and budget deadlines, which are growing more concerning, the second round of sequester cuts, and concern over the implementation of the Affordable Care Act (ACA) have created a somewhat uncomfortable environment that makes it easy to sit on the sidelines. But as the latest rally shows, some of that sidelined money comes quickly back into stocks the moment momentum appears to be turning. The "wall of worry" is intact and one of the key reasons we remain optimistic beyond any near-term volatility.

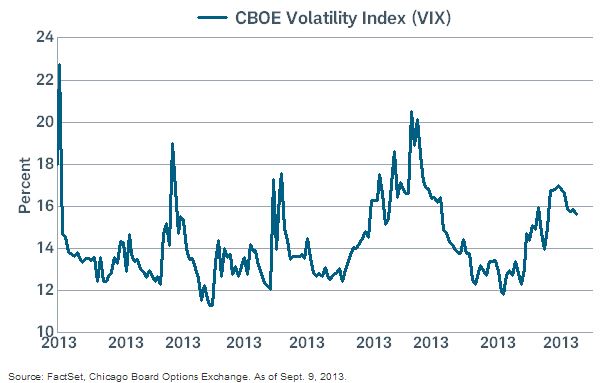

Volatility indicates increased uncertainty

In our last edition of this publication, we recommended that investors consider delaying any lump sum equity purchases for a few weeks as we believed the potential for near-term selling was elevated. But the 4.6% correction throughout August brought sentiment and technical conditions back to more reasonable levels and we see opportunities being created to put money to work given our view that the current uncertainty is more short-term in nature … and the market is a discounting mechanism Tension regarding Syria has eased slightly, a debt and budget deal is possible without a government shutdown although the parties seem to be digging in their heels, the Fed will likely take great pains not to hurt the economy as they lightly tap on the monetary brakes, and some compromises will possibly be reached with regard to the ACA.

Economy showing signs of picking up

With some investors' attention diverted to fiscal and other macro concerns, the economy is showing signs of stealthy acceleration. We've seen a surge in major merger and acquisition activity, indicating rising confidence by executives. This is a key factor as business investment has been lagging what would be expected at this stage in the cycle. There is pent-up demand that could result in a surge in capital spending over the next year or so. Companies have put off investing as they waited for a more certain economic environment and, as a result, now have aging equipment and antiquated technology that needs to be upgraded in order to compete globally. We believe this will be a major catalyst of the next leg up in stocks.

We're already seeing something similar occur on the consumer side of the economy as August auto sales rose to an annualized level of roughly 16 million vehicles; a rate not seen since before the financial crisis. With the average age of autos on the road nearly 11 years according to AutoNation, which is historically high, consumers are playing catch up from sitting on the sidelines over the past several years.

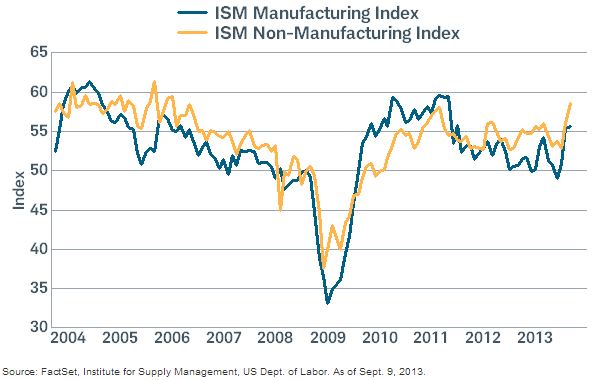

This Institute of Supply Management (ISM) also added fuel to the economic improvement fire as the Manufacturing Index showed a surprising move higher to 55.7 from 55.4, while the new orders component of the survey jumped to 63.2 from 58.3, indicating future improvement. Additionally, the ISM Non-Manufacturing Index, which measures sentiment in the services side of the economy, rose to a robust 58.6 from 56.0 as the employment component posted a 57.0 reading, up from 53.2, while new orders rose to 60.2 from 57.7.

Manufacturing and services showing signs of expansion

And much attention continues to be paid to the jobs market. The most recent labor report showed a decidedly mixed picture as the unemployment rate fell to 7.3% from 7.4%, while 169,000 jobs were added. Disappointingly, and proving the point of revisions, the previous months were revised lower. Although the latest jobs report was weaker than expected, the more leading jobs indicators are improving markedly; notably the continuing drop in initial unemployment claims. Their four-week moving average is now back to pre-Great Recession levels.

Focus on the Fed

Job growth is under the microscope more than usual since it's a key determinant of Fed policy decisions. Anxiety around the potential for a reduction in the pace of asset purchases by the Fed has been somewhat surprising to us. Getting back to a more normal monetary environment is both healthy and desirable; extreme stimulus cannot last forever, and the sooner they start to normalize, the more gradual they can likely be during the process. Tapering due to an improving economy, which appears to be the case, should be cheered, not feared, and the minimal initial approach will likely have minimal impact on the economy.

Meanwhile, Washington has been focused on Syria, but fiscal deadlines are approaching that have to be addressed. The debt ceiling needs to be dealt with by the middle of October according to the Treasury Department, and the negotiations are likely to be contentious, resulting in some more near-term volatility. In the end, we believe a deal will get done without lasting damage…and then they can move on to the budget and ACA fights that are also just around the corner.

Japan likely to "out-QE" the developed world

Budget issues aren't just an American problem of course. An important deadline looms for Japan on the decision to proceed with an increase in the consumption tax starting in April 2014. Prime Minister Abe has delayed the decision several times, awaiting evidence the economy is strong enough to withstand the hike.

Economic data has been mixed recently in Japan, with the first reading of second quarter gross domestic product (GDP) in August falling short of estimates. But the revision in September positively surprised at a 3.8% quarter-over-quarter annual rate, on top of a 4.1% gain in the first quarter. Importantly, capital spending gained an impressive 5.1%, surpassing expectations of a decline, and was the first increase since the fourth quarter of 2011. Abe has now targeted the October 1st Tankan report, where businesses give their outlooks for production, hiring, and capital spending, among other factors, to finalize the tax decision.

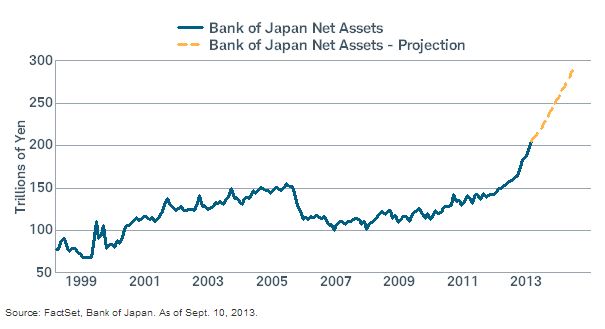

Looking further out, Japan's economy is likely to receive the largest injection of liquidity over the next year among large economies. The Bank of Japan (BoJ) has announced asset purchases at an annual pace of 60-70 trillion yen ($600-700 billion), and this would trounce the first year hit to the economy of the rise in the sales tax, estimated by economists to be roughly 5-10 trillion yen. Additionally, the BoJ said it will consider further monetary easing if the tax hike results in downside risks to the economy; and Abe's administration is openly discussing a 2 trillion yen fiscal stimulus.

The math may indicate a net positive for Japan, although that too is in question, but the bigger concern is the impact of the tax hike on the psyches and pocketbooks of consumers and businesses. Japan is navigating in uncharted waters; trying to break the grip of deflation, while also facing an unfavorable debt profile and demographic outlook. Some believe the tax decision is a lose/lose proposition; halting domestic confidence to spend and invest if the tax hike proceeds as scheduled, while hitting investor confidence that Abe is serious about fiscal improvement if it does not.

While nascent, we are encouraged by the capital spending rise in the GDP report, as well as a continued increase in the jobs-to-applicants ratio, indicating the potential for both job and wage increases in the future. Wage gains are holdouts thus far and are important for a sustainable recovery, as a weaker yen and rise in inflation cuts into discretionary consumer spending, as we discuss in our Japan article.

Bank of Japan just getting started

We believe it is a good time to consider Japanese stocks on a currency-hedged basis. The BoJ has reaccelerated asset purchases in recent weeks, with much more yet to come. We believe Japan's economic recovery is sustainable, even if the full tax hike takes effect, as the Japanese government is indicating the willingness to do whatever it takes to revive the nation. The likelihood of a weak yen reduces returns for US investors, resulting in the attractiveness of hedging currency exposure.

Europe could enter a volatile period

Many believe the calm in the eurozone is about to end, with unpopular issues pushed out until after elections in the German state of Bavaria on September 15, and the German general election on September 22. We agree that we could be entering a more volatile period in the eurozone due to continued issues with Greece's bailout program and political uncertainty in Italy. The biggest source of market volatility is likely the threat of a collapse of the Italian government, which could continue into mid-October. However, we don't believe panic will set in, due in large part to the European Central Bank's Outright Monetary Transactions (OMT) program, a strong commitment by most policymakers to the euro, and the likelihood that a new Italian government would differ little from the current one.

Eurozone stocks appear to offer opportunity

We believe volatility in eurozone stocks is likely to be a buying opportunity, as a fair amount of bad news has likely already been priced in, and earnings and valuations are depressed. Read more in our Europe article.

China: short-term gain but long-term pain

The Chinese government started the year by indicating a willingness to pursue reforms and crack down on speculation in an effort to transition the Chinese economy away from its reliance on debt-led construction. Heading into the annual planning session in November, more reforms are likely to be announced. Reports of a new free trade zone in Shanghai to expand opportunities in industries from shipping, banking, insurance and health care, as well as looser capital controls, illustrate potential reforms.

On the surface, these reforms could be long-term positives for China's economy, but the reality is likely to change slowly. In fact, in the near-term, the government appears to have reversed its position of short-term pain for long-term gain in response to their near-mistake of a liquidity crunch in the banking system in June. In its place is more of the same old economic model of debt issuance and construction of infrastructure and property; deepening the imbalances and increasing the risks for the future.

Additionally, despite an announced desire to target speculation from the shadow banking system and excess factory capacity, little has changed. As a result, economic growth in the near term is likely to accelerate. Banks appear to have the ability to delay the day of reckoning, as two "bad banks," or asset management companies (AMCs) of the past have filed for initial public offerings; potentially to raise capital that could be used to bailout the financial system.

The near-term rally in Chinese and emerging market stocks that we discussed in our last Perspective appears likely to continue due to the combination of the Chinese government's willingness to do whatever it takes to achieve economic stabilization, as well as oversold market technical conditions. We still believe emerging markets will underperform developed markets over the next 12-24 months due to overhanging secular issues, but the near-term cyclical rally could be quite fierce. Read more international at www.schwab.com/oninternational.

So what?

Cutting through the near-term noise is critical to achieving long-term investment objectives. We see improvement in the US economy and pockets of international recovery and even strength. Remember, when concern is elevated, investment opportunities often appear.

Important Disclosures

The MSCI EMU (European Economic and Monetary Union) Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of countries within EMU. The MSCI EMU Index consists of the following 11 developed market country indices: Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Portugal, and Spain.

The S&P 500 Composite Index® is a market capitalization-weighted index of 500 of the most widely-held U.S. companies in the industrial, transportation, utility, and financial sectors.

The Chicago Board of Exchange (CBOE) Volatility Index (VIX)is an index which provides a general indication on the expected level of implied volatility in the US market over the next 30 days.

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Institute for Supply Management (ISM) Non-manufacturing Index is an index based on surveys of more than 400 non-manufacturing firms by the Institute of Supply Management. The ISM Non-manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Labor Report is a monthly report compiling a set of surveys in an attempt to monitor the labor market. The Employment Situation Report, released by the Bureau of Labor Statistics, by the U.S. Department of Labor, consists of:

• The unemployment rate—the number of unemployed workers expressed as a percentage of the labor force.

• Non-farm payroll employment - the number of employees working in U.S. business or government. This includes either full-time or part-time employees.

• Average workweek - the average number of hours per week worked in the non-farm sector.

• Average hourly earnings—the average basic hourly rate for major industries.

Initial Jobless Claims is a measure of the number of jobless claims filed by individuals seeking to receive state jobless benefits reported on a weekly basis.

Real Gross Domestic Product (GDP) is an inflation-adjusted measure that reflects the value of all goods and services produced in a given year, expressed in base-year prices.

Indexes are unmanaged, do not incur fees or expenses and cannot be invested in directly.

Past performance is no guarantee of future results.

Investing in sectors may involve a greater degree of risk than investments with broader diversification.

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

© Charles Schwab