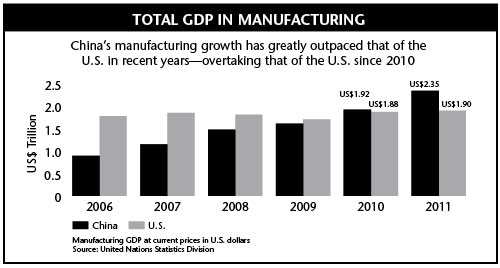

The tiny silver print on the back of my iPhone that states, “Designed in California. Assembled in China,” epitomizes today’s global supply chain. After China ascended into the World Trade Organization in 2001, the country became the world’s hub for manufacturing and assembly. Nine years later, China overtook the United States as the world’s largest manufacturing nation and has continued widening its lead. In 2011, China generated US$2.9 trillion in manufacturing while the U.S. generated only US$2.4 trillion, according to the United Nations.

Despite the numbers, many are predicting the end of China as the world’s top destination for foreign direct investment (FDI) and manufacturing. They argue that higher wages will erode its competitive advantage, forcing firms to relocate to lower cost centers.

If this scenario were really just about low wages, then low wage countries like Kyrgyzstan or the Congo, with minimum wages of less than US$200 per annum, would be magnets for FDI. Yet they are not. While this seems like stating the obvious, it highlights the misunderstood nature of China’s competitiveness. A January 2013 IMF Working Paper, “Chronicle of a Decline Foretold: Has China Reached the Lewis Turning Point?” suggests that China will transition to a labor shortage economy by around 2020. Some point to the plentiful evidence that China has already reached the Lewis Turning Point, a point at which it would move from a vast supply of low-cost workers to a labor shortage economy. Some of these pundits argue that this wage growth and labor shortage will slowly but surely make China less competitive vis-a-vis other lower wage countries in the region.

To be sure, wage growth in China is high and increasing. Minimum wage has gone from approximately US$90 in 2007 to about US$200 per month in 2013, representing an annualized growth rate of roughly 14%. At current wages, companies are finding that it makes sense to replace workers with robots. In fact, some makers of electronics have set up robots across assembly lines in a wide effort to adopt a more automated manufacturing process. Since the cost of robots would be similar worldwide, why would companies continue to manufacture in China? Perhaps location decisions have less to do with wages and more to do with other business considerations. While low wages may be the initial factor driving FDI, research suggests that other factors, such as proximity of supply chain, economies of scale, infrastructure and quality of labor might be more powerful in explaining why firms choose to stay in China.

The arguments of many China bears are predicated on a neoclassical view of the world. In the simplest version, this assumes only one factor of production—labor. Another, perhaps more sophisticated version includes two factors of production—labor and land. Newer models of trade theory suggest that transportation costs, economies of scale and the share of manufacturing in national income may be more relevant factors in driving geographic decisions. These more nuanced and more recent theories suggest manufacturing centers can cluster around pools of skilled labor, transportation networks and economies of scale. And that these clusters have a gravity or momentum that is hard to erode. The idea that investment begets more investment or “agglomeration effects” might be more powerful in driving the marginal investment today. In other words, while companies might have initially invested in China based on its low labor costs, what keeps companies in China are other factors like quality of labor, stable regulatory framework and sound infrastructure.

In a recent presentation by Rosey Hurst, the Founder and Director of Impactt, Ltd., a firm that works with organizations to improve working conditions in their supply chains, she found predictions about the demise of Chinese low-cost manufacturing to be premature. According to Hurst, China remains the number one source of supply for non-food items across most retail sectors, even though competitive advantage for wages eroded. Reasons she cited include:

- Difficulty in moving supply chain clusters because of the capital investment involved in moving

- Lack of know-how and infrastructure outside of China in large-scale

- Labor shortages around the region

- Established relationships: know what to expect from China

Infrastructure

- Political stability

- Civil society development process manages risk of supply chain disruption

Indeed, this is what we are finding on the ground. During a recent trip to Jakarta, I had the opportunity to tour a manufacturing plant. The manager of the plant was a Canadian who had managed plants worldwide, including the United States, China and Indonesia. When I asked him how he would compare wages between China and Indonesia, he said that Chinese wages are at least twice as expensive as that of Indonesia. “But,” he added, “The Chinese worker is at least twice as productive.” While pointing to a piece of heavy equipment imported from Germany, he explained, “It takes expertise to maintain these machines, so we are careful in not having too much mechanization because it could inadvertently create more outage and maintenance costs that we are not equipped to deal with. Because the skill level of the Chinese worker is higher, we can install more machinery, thereby making the Chinese worker more productive.”

In this case, is the average factory worker in China is earning twice as much as his counterpart in Indonesia. But he is also at least twice as productive. In this particular example, the added productivity appears to come from the expertise of the Chinese worker and increased capital expenditures of the China-based plant. While labor can be a simple guide to what is happening in China’s economy, there is more nuance to understanding the country’s growth and productivity than it may suggest. In his landmark paper “Increasing Returns and Economic Geography,” economist Paul Krugman develops a model that shows how a country can endogenously become differentiated into an industrialized core and an agricultural periphery. In order to realize economies of scale while minimizing transport costs, manufacturing firms tend to locate in the region with larger demand, but the location of the demand itself depends on the distribution of manufacturing. Emergence of a core-periphery pattern depends on transportation costs, economies of scale and the share of manufacturing in national income. It seems that the new trade theory as espoused by Krugman may provide a more fitting explanation of current world trade, and why China might continue to remain the world’s largest manufacturer.

More recent views of trade patterns support China’s continued strength in manufacturing. The concept of “economies of agglomeration,” for instance, points out that firms benefit when they develop clusters of manufacturing in a country. Detroit, the “Motor City,” was an early example of this in the U.S., and across China we see similar concentrations of manufacturing industries like textiles in Ningbo, computer parts in Dongguan and ships in Zhuhai. Studies have shown that competing firms benefit from this proximity because it helps foster innovation and the spread of new ideas, while encouraging specialization. Whether these manufacturing clusters develop for historical reasons, by chance, or through policy initiatives, the ability to share pools of labor and technical expertise encourages further growth and investment from both domestic and foreign companies.

Teresa Kong, CFA

Portfolio Manager

Matthews Asia

The views and information discussed in this article are as of the date of publication, are subject to change and may not reflect the writers' current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of any securities or any sectors mentioned herein.

The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Matthews International Capital Management, LLC does not accept any liability for losses either direct or consequential caused by the use of this information.

© Matthews Asia