Despite a mediocre August jobs report, we still expect the Federal Reserve to announce a slowing of the pace of bond purchases when it meets next week. One reason for this view is that Fed officials care more about the level of the unemployment rate than the pace of job creation. We often write that monetary policy is about “gaps” not growth: the Fed is trying to reduce spare capacity in the economy, not bring about a rapid expansion per se. This is why the Fed’s guidance about the funds rate and quantitative easing (QE) are both expressed in terms of the unemployment rate, not the pace of job creation. So although the employment report disappointed markets, the decline in the unemployment rate to a new cycle low of 7.3% probably has more bearing on the outcome of the FOMC meeting.

That being said, many observers worry that the unemployment rate overstates the health of the labor market because many people have simply stopped looking for work. This shows up in the data as a decline in the labor force participation rate (LFPR)—the percent of the working age population that is currently engaged in the job market (i.e. working or looking for work). The decline in the LFPR is an important issue for the economy, but it’s not central to our Fed call for two reasons.

First, Fed officials have continued to stress the importance of the unemployment rate despite possible flaws. San Francisco Fed President Williams made this argument in a speech this week:

“There are reasons to worry that the unemployment rate could now be understating just how weak the labor market is … So should we stop using the unemployment rate as our primary yardstick of the state of the labor market in favor of the employment-to-population ratio? My answer is no. Although the unemployment rate is by no means a perfect measure of labor market conditions, the employment-to-population ratio blurs structural and cyclical influences. That makes it a problematic gauge of the state of the labor market for monetary policy purposes … the preponderance of evidence indicates that the unemployment rate remains the best overall summary statistic.”

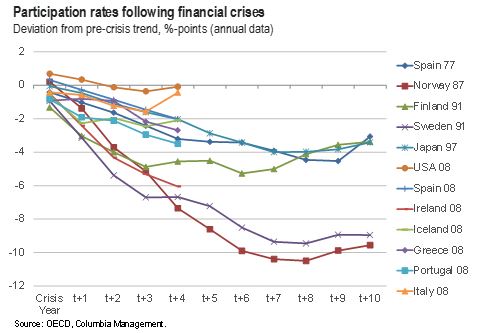

Second, the history of financial crises suggests a swift recovery in the LFPR is unlikely. The reason for our view on this topic is pretty simple: this is the pattern we observe following other financial crises. The chart shows changes in LFPRs following 12 major financial crises (defined as deviations from trend in the 10 years prior to the crisis). The first few are the so-called OECD Big Five financial crises. The remaining seven are from the 2008 downturn.

On average, participation rates are 3.4 percentage points lower than the pre-crisis trend four years after the crisis. In the U.S. today, the LFPR is about 3 percentage points lower than the level in 2007—in the ballpark of the other examples through history. If we assume a falling trend for the U.S. (as we have in the chart), the decline in the LFPR actually looks small on a comparative basis.

In other countries with financial crises, participation rates took a very long time to stabilize. In the Big Five sample, they remained below pre-crisis trends for more than 10 years after the crisis year. Judging by history, our base case for the U.S. would be that the participation rate will stabilize only gradually over the next couple of years. A sharp rebound in the LFPR—which would have a major impact on the outlook for the Fed—appears unlikely.

*Organisation for Economic Co-operation and Development

Disclosure

The views expressed are as of 9/9/13, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

There are risks associated with fixed income investments, including credit risk, interest rate risk and prepayment and extension risk. In general, bond prices rise when interest rates fall and vice versa. This effect is more pronounced for longer-term securities.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2013 Columbia Management Investment Advisers, LLC. All rights reserved. 726228