Macro Themes: 2H13

U.S.

- The Fed will be late in removing monetary accommodation as the economy strengthens.

- Consumers will be strong contributors to economic growth.

- Political uncertainty, and its impact on markets and the economy, is declining.

GLOBAL

- As austerity wanes, Europe is poised for growth.

- A resurgent Japan will have a positive impact on global markets.

- Improving global growth and continued ample liquidity should help emerging market assets stabilize.

OUTLOOK

- Highly accommodative monetary policy has depressed real sovereign yields and distorted valuations across fixed income. As such, security selection is vital.

- Market returns will depend on the developed world’s ability to maintain economic momentum despite softness in many emerging market economies.

Brave New World

“And if ever, by some unlucky chance, anything unpleasant should somehow happen…there is always soma, delicious soma, half a gramme for a half-holiday, a gramme for a week-end, two grammes for a trip to the gorgeous East, three for a dark eternity on the moon…”

— Aldous Huxley, Brave New World

If the monotony of high school lulled you into a catatonic state the semester you were supposed to read Brave New World, here’s the CliffsNotes summary of what you missed. Aldous Huxley imagined a futuristic utopia in which the government promotes economic and emotional stability through the plentiful use of a soporific opiate called “soma”. Soma allows the mind to take a holiday from worldly problems via a gram, or two or three. Imagine the chaos into which this fictional world would descend were the government to abandon its role as pharmacist to the masses.

A world free from the monetary equivalent of soma is the one we now find ourselves contemplating. Since 2008, the lulling effects of easy monetary policy have promoted stability — until May of this year, when investors started to panic about the potential tapering of the Federal Reserve’s asset-purchase program. The prospect of less quantitative easing and higher real interest rates has re-awakened the yield curve and made the duration component of fixed income return really start to sting. But as investors continue to fear the after-effects of tapering and the eventual unwinding of zero interest rate policy in the United States, can’t we feel good about a world ready to wean itself from extraordinary support?

From a thematic standpoint, we think so. What’s more, it’s important to keep in mind that our brave new world will be defined by less support, not a complete cessation of it.

U.S.: Tapering Does Not Herald the End of Monetary Accommodation

Our belief is the Federal Reserve — under Ben Bernanke or any of the candidates likely to succeed him — will be slow to remove monetary accommodation in response to the strengthening economy, though the Fed’s data dependence will be real and likely increase volatility as the end of the current bond-buying program draws near. Despite the fact that the U.S. employment picture is brightening and points to a September taper, the anticipation of which has been a key driver of near-term volatility, we need to remember that the path of short-term interest rates differs from that of tapering decisions. We believe tapering has been priced in already; the asymmetric risk now lies more toward the front end of the curve. Inflationary pressures remain benign, and median Fed forecasts for front-end rates by the end of 2015 actually have been revised down. Thus, the Fed is still reinforcing an underlying dovishness as it relates to the front end of the curve. While Larry Summers has emerged as the frontrunner to succeed Bernanke, all of the viable candidates for the job — which include Janet Yellen and Don Kohn in addition to Summers — would be expected to maintain the Fed’s zero interest rate policy for quite some time.

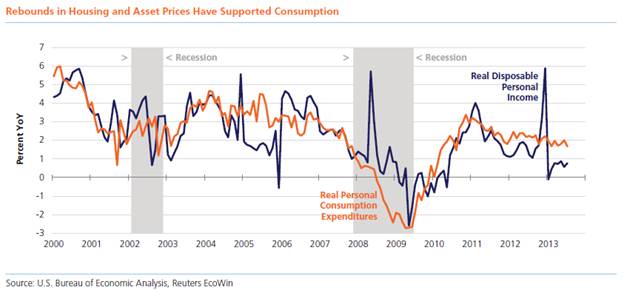

We continue to have a positive outlook on the strengthening U.S. economic picture that has brought the Fed to the point of tapering sooner rather than later. We think U.S. consumers will be a robust source of economic growth, supported by continued improvement in housing and asset prices. Consumption growth, however, has been slow to transmit to other sectors of the economy; this transmission remains key to a self-sustaining recovery. Improvement in the labor market has helped drive personal income growth to levels at which we have already seen strong consumption growth, making the overall trajectory seem more sustainable than it has appeared in recent years. Consumer balance sheets have been strengthened by the recovering housing market and to a certain extent by recovering financial asset returns.

In our view, another positive factor is that U.S. political uncertainty, and its impact on the markets and the economy, are in decline. Fiscal tightening will continue at a prudent pace despite the lack of a “grand bargain”; the related economic drag will not trump private-sector strength or easy monetary policy. U.S. second quarter GDP has been revised up to 2.5%, from 1.8%, and the fiscal headwinds seem on track to ease in the third and fourth quarters, painting an increasingly positive GDP picture. October is still the likely binding deadline for the debt ceiling, and noise is beginning to ramp up on this front. However, we expect the same pattern as before — brinksmanship ultimately followed by a compromise in which both political parties extract some benefit.

Global: Europe and Japan Poised to Contribute to Growth

Another political tailwind helping the global economic outlook is emanating from Europe. Europe’s era of austerity is winding down, setting the stage for positive economic growth in the troubled currency union. Political willingness to implement new belt-tightening measures has faded, while the European Central Bank’s (ECB) appreciation of easy monetary policy has increased with intra-region economic convergence. Bank deleveraging will continue to inhibit growth, but even the slow progress toward banking union is bolstering financial system stability.

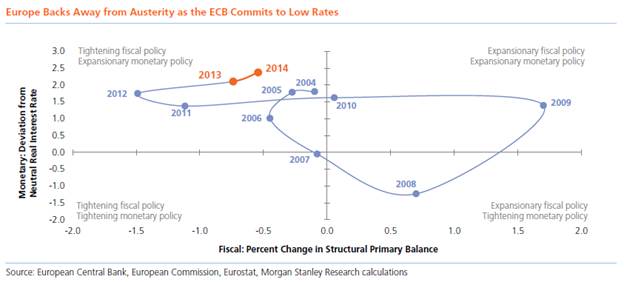

As the graph below illustrates, Europe has moved from fiscal policy tightening toward a more moderate stance. The overall picture seems to be more supportive of growth, if more ambiguous for sovereign credit fundamentals over the short term. While the return to positive economic growth could promote upward pressure on interest rates, we must keep in mind that the ECB recently gave forward guidance that rates would stay low for a long time, much as the Fed did two years ago.

Though mitigated by idiosyncratic weakness in China, Japan will continue to have a positive impact on the global economy through monetary policy and reform. The Bank of Japan’s purchase activity will continue to bolster asset prices, and the government’s commitment to structural reform paired with fiscal stimulus will ensure that Japan’s expansion does not come solely at the expense of its trade competitors. Shinzo Abe’s majority in Japan’s upper legislative house enables him to focus on the economic front and is driving positive longer-term growth and inflation expectations.

Outlook: Environment Is Improving, but Caution Is Warranted

In summary, the U.S. economy will strengthen and the effects of fiscal drag will diminish, Europe will move away from austerity to a more growth-oriented trajectory, and Japan will bolster markets with its three-pronged approach to reverse long-entrenched deflationary pressures. While idiosyncratic weakness in China, higher developed market interest rates and weaker commodity prices have been a drag on emerging markets, improving global growth and easy monetary policy worldwide create a supportive environment for emerging market assets to find stability despite fundamental challenges.

Despite this supportive backdrop, investors must exercise caution. As the Fed inches closer to withdrawing its daily dose of balance sheet expansion, markets will become increasingly wary of the assumptions that guided them during this great monetary accommodation. Extremely accommodative monetary policy has contributed to financial repression by depressing the real yields of sovereign bonds. Continuation of this trend, alongside a reduction of tail risks, has richened valuations of a wide variety of assets. Security selection will be increasingly important given the full valuations of many financial assets. The recent interest rate selloff illustrated that broad “risk-on/risk-off” correlations are no longer reliable. As we move further into this long, slow recovery, expect assets to become increasingly differentiated rather than being swept along the lulling, common tide of Fed liquidity.

As we imagine a world free from the anomalous effects of monetary soma, it is critical to focus on real economic outcomes lest we get too caught up in the market’s taper tantrums. Fixed income returns ultimately will depend on the market’s judgment of whether the developed world can maintain economic momentum despite softness in a number of emerging market economies. It is our belief that this momentum will be maintained. Furthermore, we also expect inflationary pressures to remain subdued. As such, we believe that the recent and dramatic increase in ten-year U.S. treasury rates to near 3% represents the vast majority of any upward movement we are likely to see in the near term. Further interest rate volatility is likely to be focused asymmetrically on short-dated instruments, which are more heavily influenced by the expected timing of Fed interest rate hikes. These influences should exert flattening pressure on the yield curve, with short-term rates rising in a fairly pronounced fashion while ten-year rates drift only modestly higher.

In this environment, absolute returns in fixed income securities are likely to be modest but positive, further increasing the importance of security selection. In the near term, sectors of the bond market tied to the developed economies are likely to outperform those more closely linked to emerging economies. Corporate bonds issued in both the U.S. and Europe should prove well-supported. Price swings resulting from such factors as fear-induced volatility will impact market prices and at times distort valuations dramatically; such moments, however, create opportunities for those investors with a disciplined focus on their economic convictions.

This commentary has been prepared by ING Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors. Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 6365