Underwriters Lose No Time Pumping Out New Shares after Labor Day

Float Research: Fund Flows Swing Wildly for Third Consecutive Month

The monthly flows of Mutual Fund and ETF volatility continued as a roller coaster trend was apparent in the last three months. Read this investor insight by Minyi Chen, CFA, Chief Operating Officer of TrimTabs Investment Research and Portfolio Manager of AdvisorShares TrimTabs Float Shrink ETF (NYSE Arca: TTFS) to learn about the variable trend flows.

Fund Flows Swing Wildly for Third Consecutive Month. Investors Bail on U.S. Equities, Continue to Snap Up Foreign Equities, and Continue to Sell Bonds.

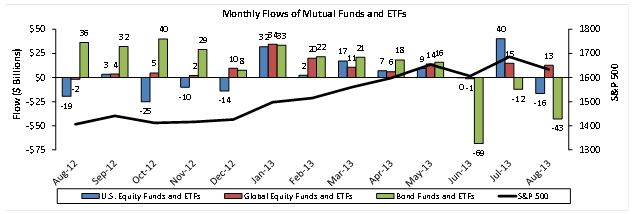

A quick glance at the graph below shows how wildly fund flows have been swinging since Federal Reserve Chairman Ben Bernanke’s hint about “tapering” in late May. We have never measured such volatility since we began tracking fund flows in the mid-1990s.

Source: TrimTabs Investment Research

U.S. equity MFs and ETFs were virtually ignored in June, but then investors poured a record $40.2 billion into them in July. This inflow was partially reversed in August, when they redeemed $16.5 billion. The wild swings were likely the result of hedge funds making and then unwinding an ill-timed bullish bet on U.S. equities. U.S. equity ETFs—which are heavily traded by institutions—issued a record $31.8 billion in July and then redeemed $15.3 billion in August.

Buying of offshore stocks has been much steadier. Global equity MFs and ETFs issued $14.9 billion in July and $12.6 billion in August, and inflows were fairly evenly distributed among MFs and ETFs. These inflows occurred even though the average global equity fund (+1.9%) underperformed the average U.S. equity fund (+2.8%) in this period. We think contrarians should consider underweighting or avoiding offshore stocks.

What contrarians may want to consider buying are bonds. Redemptions from bond MFs and ETFs peaked at $68.6 billion in June, subsided to $12.1 billion in July, and picked up again to $42.9 billion in August. The redemptions in June and August were the highest on record. Fund flows tend to be good contrary indicators when they reach extreme levels, and the selling this summer certainly qualifies as extreme.

Corporate Actions Mostly Favorable for Stocks. New Offering Calendar Continues Its Late Summer Snooze. Volume of New Stock Buybacks Tops $30 Billion for Seven Consecutive Months.

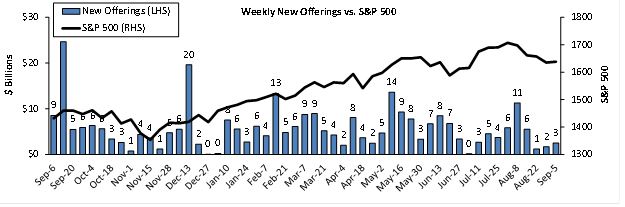

We wrote in the TrimTabs Weekly Liquidity Review released Sunday that our demand-side indicators turned more favorable for stocks. Supply-side indicators are also favorable, partly for seasonal reasons.

The new offering calendar will likely be slow this week, which is positive for stock prices. All else being equal, the fewer new shares underwriters sell, the more money Wall Street intermediaries have left to buy existing shares. Only $2.9 billion in new shares came to market in the previous two weeks, and this week’s pace is unlikely to be any higher than $3 billion. A $400 million convertible for Liberty Interactive was the lone deal that priced Friday and Tuesday, and Dealogic reports that $1.7 billion is on deck for later this week, led by follow-ons for LinkedIn ($1.2 billion) and Hain Celestial Group ($350 million) expected Wednesday.

Source: TrimTabs Investment Research

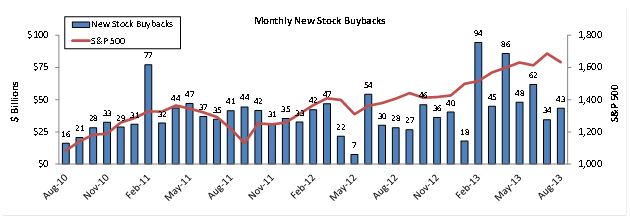

Another positive longer-term signal is that the volume of new stock buybacks is holding up well. Buyback volume has historically had a high positive correlation with the S&P 500. Buybacks have exceeded $30 billion for seven consecutive months. While the volume fell to a six-month low of $34.5 billion in July, it rebounded to $43.4 billion in August.

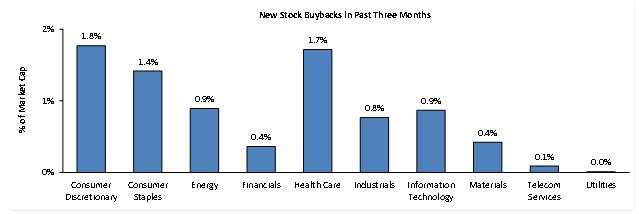

Buyback announcements in the past three months were highest in Consumer Discretionary, Consumer Staples, and Health Care. Buybacks have been particularly broad based lately in Consumer Discretionary, which is a key reason we are overweight the sector in our Sector Model Portfolio. Viacom ($10.0 billion), CBS ($5.1 billion), 21st Century Fox ($4.0 billion), and Time Warner Cable ($2.4 billion) all rolled out big repurchases in the past six weeks.

This communication is a publication of TrimTabs Asset Management. It should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. Information presented does not involve the rendering of personalized investment advice. Content should not be construed as an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein. Performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing performance returns. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Past performance may not be indicative of future results. Therefore, no investor should assume that the future performance of any specific investment or investment strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions, may materially alter the performance of an investor’s portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor’s portfolio.

© AdvisorShares