Absolute Return Letter: A Case of Broken BRICS?

“When written in Chinese, the word ‘crisis’ is composed of two characters. One represents danger and the other represents opportunity.”

John F Kennedy

Whilst many chose to spend August on the beach, a full-blown crisis developed across emerging markets, and the BRICS in particular. The ‘B’ got into trouble with its currency under severe pressure. So did the ‘I’ and the ‘S’, whilst the ‘R’ and the ‘C’ both experienced loads of bad news on the economic front. Not exactly what you have come to expect from the BRICS.

The first seven trading days of September have offered all of these markets some much needed breathing space with EM currencies, bond and equity markets all doing considerably better. It is thus tempting to conclude that this was just another one of those summer hiccups that have become the norm in recent years. I do not buy that argument for one second, though. There are some very sound fundamental reasons why the crisis erupted now, which we will get into a little bit later.

Perhaps most surprisingly, though, the EM crisis didn’t (and still doesn’t) get a huge amount of media coverage. I suspect that, when you come up against a human disaster like the one which is currently unfolding in Syria, a currency crisis tends to be somewhat overlooked. The use of chemical weapons is a much better news story than collapsing foreign exchange rates and, as we all know, the world’s media are so utterly one-dimensional that they can only deal with one crisis at a time.

Now, I am not for a single moment suggesting that what is going on in emerging markets is more important than the unmitigated human tragedy in Syria. Far from it; however, the reality is that the financial system is a cynical beast. It doesn’t really care much about human disasters. Even political crises, however dramatic, tend to have only a passing effect on markets. No, what really matters to the markets is a good old fashioned financial crisis.

Before I go any further, please accept an apology. This letter is late, very late. We try to publish the Absolute Return Letter within the first five days of the month, but there is just too many things going on at the moment. It is also quite a short letter this month. It looks long but, in terms of word count, it is one of the shortest I have ever written. You may actually find that liberating!

My intention this month was to write about some of the effects of changing demographics. I have done a great deal of research on the subject over the summer, but I am not quite ready to share my findings with you. It is a big and complex subject. Changing demographics are like a tsunami. It looks as if everything happens in slow motion but the consequences are dramatic. New research suggests that demographics may even influence the effectiveness of monetary policy, but more about that next month.

Is this a re-run of 1997-98?

When the Asian crisis kicked off in Thailand in July 1997, not many paid attention at first, and even fewer imagined the devastating effect it would have on the entire region. It left deep scars some of which are still visible, hence the question: Is this a re-run of 1997-98? Before I try to answer it, let’s have a quick look at the damage inflicted so far.

Chart 1: Value of selected EM currencies vs. US dollar since January 2013

Source: Wells Fargo, Weekly Economic and Financial Commentary, 30 August 2013.

The debacle in EM currency markets started in late May and has only gained in momentum since (chart 1). You may recall that May 22 was the day Ben Bernanke first signalled the Fed’s intent to gradually wind down the bond purchasing programme, so perhaps we should look to monetary policy for an answer to the unfolding crisis.

Chart 2: Value of EM equity and bond markets since January 2012

Source: Citi Research, Global Economic Outlook and Risks, 2 September 2013.

The Fed has provided oceans of liquidity through its open market operations over the past few years and the markets chose to interpret Bernanke’s statement as if tapering could commence as early as September. With liquidity likely to deteriorate over the next couple of years, it is only logical that investors’ perception of liquidity has changed. Nowhere has seen a bigger influx of speculative capital than Asia, so perhaps we shouldn’t be so surprised to see some of that capital on the move again. What’s more, the sell-off has not been confined to FX markets. EM equity markets (MSCI EMs) and bond markets (EMBI+ EMs) have both suffered quite badly as investors have pulled out of emerging markets (chart 2).

The other half of the liquidity story

Open market operations conducted by central banks are only half the liquidity story, though. The other half is a function of the U.S. dollar being the preferred reserve currency and the primary trading currency of the world. As a result, the U.S. provides liquidity to the rest of the world through its chronic current account deficit. I have written about this in the past (see for example the April 2013 letter and the September 2005 letter) and provided evidence that, when the U.S. drains liquidity from the global punch bowl, whether directly or indirectly, there is usually a hiccup or two somewhere. This latest episode seems to be no exception.

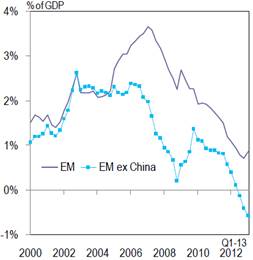

You may say that the U.S. current account hasn’t really improved enough recently to create the type of scenario I am referring to. That is perhaps correct, but the aggregate trade balance of EM economies paints a very different story, suggesting they no longer have access to the liquidity they used to (chart 3).

Chart 3: Trade balance as % of GDP

Source: Citi Research, Global Economic Outlook and Risks, 2 September 2013.

Following the 1997-98 Asian crisis, many countries in the region managed to turn the fiasco into an export led revival, and trade and current account surpluses became the norm in the region rather than the exception. Years of large current account surpluses led to a substantial accumulation of foreign exchange reserves, nowhere more so than in China. Between them, EM economies are estimated to hold in excess of $8 trillion of FX reserves today, providing them with a cushion they could only dream of when the crisis struck in 1997 (chart 4).

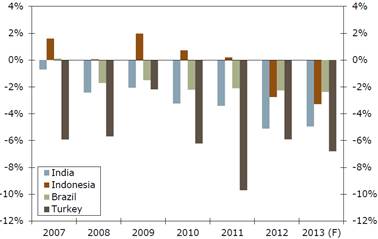

More recently, the current accounts of EM economies (ex. China) have again dipped into the red, suggesting that they are beginning to feel the pain of slow growth in Europe, the U.S. and Japan. India, Indonesia, Brazil and Turkey have all experienced a depreciation of 12% or more in the value of their currency year-to-date when measured against the US dollar and that’s not the only feat they share. They all run a substantial current account deficit (chart 5).

Chart 4: FX reserves in selected Asian countries (USD billion)

Source: Barclays, Different from 1997, 30 August 2013.

Chart 5: Current account balance in selected EM countries (% of GDP)

Source: Wells Fargo, Weekly Economic and Financial Commentary, 30 August 2013.

Markets are being nothing but efficient

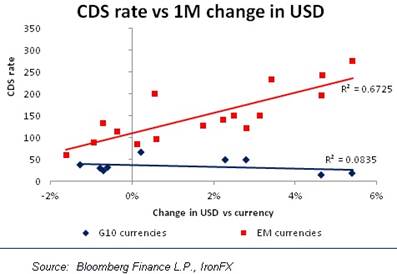

Running a chronic current account deficit is one thing when you are Uncle Sam but something altogether different when you are an EM economy with a mixed track record. If you lose the goodwill of your creditors, borrowing can suddenly become frightfully expensive. Sovereign credit default swap (CDS) rates are a good measure of the perceived risk on sovereign debt. When countries get caught in the type of vicious spiral that many EM countries find themselves in at the moment, you would expect the capital flight to be most severe in the countries that are perceived to be the riskiest, i.e. those trading at the highest CDS rates. Assuming that a weakening currency is a good proxy for capital on the run, you would expect those countries trading at the highest CDS rates to experience the biggest depreciation in the value of their currency, and that is precisely what has happened in the EM space (chart 6).

When a currency depreciates in value, many everyday essentials such as food and energy become more expensive as they are often imported. Consequently, inflation begins to rise. Again, markets have proven remarkably efficient in the sense that those countries already plagued by high inflation have seen the sharpest depreciation in the value of their currency (chart 7).

Chart 6: The correlation between CDS rates and currency values

Chart 7: The correlation between inflation and currency values

The EM credit bubble

Now, where does all of that take us? The combination of stubbornly high inflation and a chronic current account deficit is poison to any economy, let alone EM economies that are more often than not forced to borrow in other currencies than their own. When economic growth in the old world hit a brick wall in 2008, EM economies embarked on a credit induced investment and consumption boom in order to keep the wheels spinning. This has been most noticeable in China where private sector debt has risen by almost 50% between 2008 and 2012, but other EM economies have not exactly been shy about taking on more credit either (chart 8). This means that some of these countries, most noticeably China, will now try to achieve what the rest of us failed so miserably to do – get out of a credit bubble without falling into a severe recession.

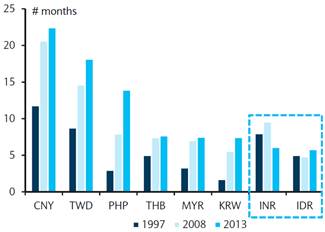

The more optimistic souls amongst us argue that Asian countries have learned from their mistakes in 1997-98 and are much better equipped to deal with a capital flight today. One measure which is often quoted is the ratio of FX reserves-to-average monthly imports which is usually considered to be adequate if it is higher than six months. On that measure there is no question that most countries in Asia are better off today than they were going into the crisis in 1997 (chart 9).

Chart 8: Change in private sector debt (gross, non-financial, % of GDP)

Source: Citi Research, Global Economic Outlook and Risks, 2 September 2013

Chart 9: Import coverage in selected Asian countries

(FX reserves / average monthly imports)

Source: Barclays, Different from 1997, 30 August 2013.

However, there are a number of problems with that argument. First and foremost, not all Asian countries have adequate FX reserves. India and Indonesia look particularly poorly equipped to deal with a prolonged flight of capital. Secondly, there are signs that this crisis is not so much an Asian crisis as it is a broader EM crisis with Brazil, Turkey and South Africa all looking as much at risk as India and Indonesia. Finally, although there is no clear evidence of it yet, with about $5 trillion in FX reserves in the hands of EM economies other than China, who could blame them if some of those reserves were used to protect their currency against a sustained attack from abroad?

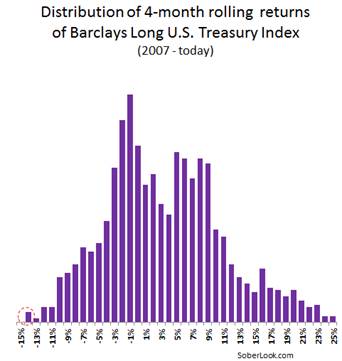

Most of the world’s FX reserves are held in the top four currencies (USD, EUR, JPY and GBP). It is not unthinkable that the recent rise in interest rates in both Europe and the U.S. has at least in part been caused by EM central banks trying to shore up their own currency. And it is even more plausible that, if the rout continues, this could become a much bigger factor; hence the EM currency crisis could find its way into Europe, the U.S. and Japan through the back door. Recent returns on U.S. treasuries are the worst they have been since 2007 (chart 10). If the EM currency crisis deepens, it could quite possibly get a lot nastier. All the perma-bears on inflation could be proven right on U.S. bond yields but for the wrong reasons.

Chart 10: U.S. Treasury returns, 2007-12

Source: Soberlook.com. The leftmost bucket contains five periods that constitute the worst losses on U.S. treasuries since 2007. All five of those periods ended in the past 4 weeks.

I note with some amusement that, during the recent G20 meeting in St. Petersburg, Russian President Putin announced the launch of a $100 billion BRICS rescue fund designed to discourage speculative attacks on one or more of the five BRICS currencies. The move illustrates a few harsh realities, the most important being that a rescue fund of this magnitude is akin to wetting your trousers to stay warm. The effect is likely to last no more than a few minutes.

I also wonder how long China can sit and watch this without taking action? Their currency is actually up slightly against the U.S. dollar year-to-date. The Chinese economy appears to be on life support at the moment (well, at least by their elevated standards) and a strong renminbi vis-à-vis the other Asian currencies is not exactly what they need. If EM currencies continue their slide, a Chinese devaluation cannot be ruled out.

In other words, there are several ways this crisis can escalate. A spill-over into developed markets? Currency wars? Who knows but, whatever happens next, we are certainly not out of the woods yet.

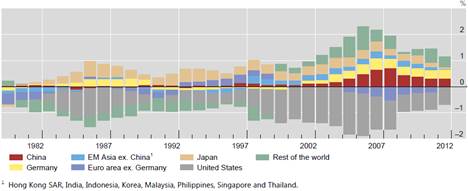

An unbalanced world is becoming more balanced

Despite my concerns, it is not all bad news. Global imbalances, caused to a large degree by misguided principles when dealing with the previous EM crisis in 1997-98 and very much the root cause of recent years’ problems, are slowly correcting themselves. At the peak in 2006, current account imbalances accounted for more than 2% of world GDP. That number has since dropped to just over 1% of world GDP (chart 11). If that trend continues, the world will indeed become a much more stable place, at least in economic terms.

Chart 11: Current account balances (% of world GDP)

Source: BIS Working Paper No. 424, Global and Euro Imbalances

It is time to re-visit the opening question. Is it a re-run of 1997-98? At the moment it is not. It is effectively an echo bubble, created as a consequence of years of easy credit in our part of the world. For now, the crisis is confined to a handful of countries that suffer from either high inflation or a large current account deficit or a combination of both. However, one important lesson learned from the 1997-98 crisis is that the disease can spread very quickly and this time, unlike in 1997-98, higher interest rates could quite possibly do considerable damage to Europe, the U.S. and Japan neither of whom can afford for bond yields to rise much at this precarious stage of the recovery.

Putting that risk into context, it does worry me that our central bankers seem to suffer from battle fatigue whilst our political leaders seem to have somehow and rather foolishly convinced themselves that we are finally out of the woods. The Lehman induced crisis is now firmly behind us, and there is no longer a need for wholesale reforms, or so they seem to think. Perhaps Mark Twain was right when he said that politicians and diapers must be changed often, and for the same reason.

Niels C. Jensen

11 September 2013

© Absolute Return Partners LLP 2013. Registered in England No. OC303480. Authorised and Regulated by the Financial Conduct Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP ( ARP). ARP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

Absolute Return Letter contributors:

|

Niels C. Jensen |

Tel +44 20 8939 2901 |

|

|

Nick Rees |

Tel +44 20 8939 2903 |

|

|

Tricia Ward |

Tel +44 20 8939 2906 |

© Absolute Return Partners