Stocks finished higher last week, but August was a down month as worries about monetary policy including who will lead the Federal Reserve next year, along with the confusion surrounding the Obama administration’s Syria decisions have put a damper on things for now.

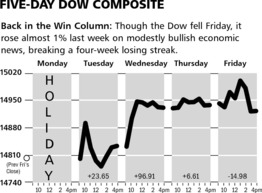

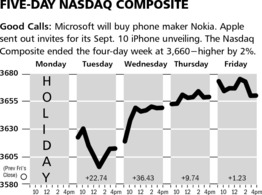

As the charts above illustrate, last week saw the Dow Jones Industrial Average gain .75% while the NASDAQ Composite jumped by nearly 2%.

The Markets & Economy

August is a traditionally down month for stock prices and this year proved no exception, but it was hardly a big decline and the volume was very low. Events in the Middle-East lit a fire under the global oil market and even caused a rebound in gold, but overall were a negative for the stock market.

Perversely, the consensus of the financial media continues to be that the economy is improving to a point which justifies the Federal Reserve Board announcing a change in its quantitative easing policy next week when they meet. I think the reality is simply this: The monthly budget deficit in the United States has fallen from over one TRILLION dollars annually to simply around 700 Billion dollars. Thus the need for the Fed to buy up newly-issued U S sovereign debt is similarly reduced.

Accordingly, the policy needed to change if only for technical reasons. Do not let all the happy talk about the economy confuse your minds. The economy is growing today at the same lackluster rate that we have seen for years. There are many reasons to expect this growth rate to suffer in the near-term, as interest rates have moved quite a bit higher as have oil prices. Consumer sentiment measures have remained ok, but actual retail sales have been light as witnessed by the many retail sales warnings announced in the past several weeks.

Of course, all of these debates come together once a month when the Bureau of Labor Statistics releases the monthly report on non-farm payroll job creation. This happened last Friday and the “official” unemployment rate dropped to 7.3% even as the number of people in the country working fell by over 100,000. Only the government and economists can really make any sense out of this nonsense.

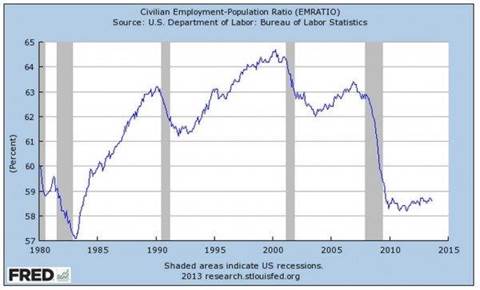

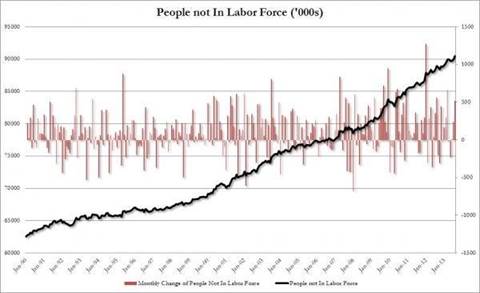

As pictured in the graphs below, the very important participation rate fell to a 35 year low. Some NINETY million Americans are simply not counted as existing for purposes of calculating the available labor pool. America still has fewer jobs today in the economy then back in 2008, before the recession. Somehow these dreary reports are being manipulated by the financial media into the myth that the economy is doing well and likely to improve.

My take is that we have heard this improvement story for four years and the numbers are what they are - Dismal.

Corporate profits, on the other hand, are doing pretty well. Productivity is much higher, and this means companies are reticent to hire new workers unless it means higher sales. Higher sales are not coming easy in an economy which on a nominal basis remains near recessionary levels (historically speaking).

What this continues to mean to us as investors is good news. While society at large is waiting for better (that means different) economic policies to take hold, the combination of zero interest rates and high productivity levels are creating strong corporate profits resulting in higher dividends, buybacks and mergers (see our comments on Vodafone below).

Consequently, the mini-taper to be announced next week is not enough to upset the apple cart. Politicians and monetary authorities know the truth: The economy is barely holding its head above water. Any success the economy has had is due to stabilization (not resurgence) in the housing sector and because of our new-found energy independence. Neither is changing anytime soon. Without tax cuts on income and investment, which are not forthcoming with the present mixed government in Washington DC, a more robust growth rate for our economy is simply not in the cards. If anything the next few quarters could be disappointing.

Change, though, might be coming. Australia just installed a new tax-cut government over the weekend and Norway has finally had enough of the Socialists and is poised in elections this week to throw them out of power.

What to Expect This Week

It seems that Syria will dominate the news until Friday. This includes an address to the nation tomorrow night from President Obama. The Senate will consider the matter this week with the House picking it up next week. We have to look forward to another week of speeches, but no final decisions.

Additionally, on Friday the government updates on Retail Sales for August, which by all accounts were disappointing along with “back to school” sales. By the end of the week, though, the markets will be on hold as next week is a Federal Reserve Board meeting affair along with the final vote on Syria from the House of Representatives.

![]()

VODAFONE

SYMBOL: VOD

Shares of Vodafone have rallied recently after Verizon announced that they are paying $130 billion for the 45 percent stake in Verizon Wireless that Vodafone owned. This deal had been rumored for years, and Vodafone’s management made the right decision to sell its stake given the current robust valuation of Verizon Wireless. We have been buying shares of Vodafonefor our clients over the past year in expectation of this deal, and we look forward to holding on to these shares going forward.

Under the terms of the deal, Vodafone shareholders will receive about $4.85 per ADR in cash, and about $12.20 in Verizon common stock per ADR. Vodafone plans to hold on to $46 billion in cash after the transaction to help strengthen its balance sheet, make further acquisitions and significant increases in future dividends to shareholders. We believe this is the ideal way for management to distribute the proceeds to investors, while strengthening the financial position of the Company.

We believe that shareholders of Vodafone are the big winners in this deal as Verizon is paying a handsome price for the Verizon Wireless stake. Also since announcing this deal, it has been rumored that AT&T might have an interest in acquiring the rest of Vodafone, which would be an added bonus to shareholders.

Shares of Vodafone are 30 percent higher this year, and we took little risk to achieve these returns for our investors. We expect that remaining Vodafone shareholders will be further rewarded by management primarily through higher dividend payouts. We believe shares of Vodafone will trend higher until this deal in completed.

SYMBOL: MSFT

We have recently been purchasing shares of Microsoft for both our dividend and growth account clients, as the Company has been making numerous announcements over the past several months. Without question Microsoft is a cheap stock, but we believe that with the recent developments shares of Microsoft are ready for a significant upward move.

First of all, Microsoft announced that embattled CEO Steve Ballmer will be retiring within the next year, which is a clear positive for shareholders as Ballmer’s strategic missteps have hurt the Company for the past decade. Secondly, last week Microsoft announced that they are purchasing the mobile handset business of Nokia for about $7 billion, that led to the most recent sell-off, which we believe represents a great buying opportunity.

With Ballmer out at Microsoft, we expect significant positive changes at the Company and for investors. The Company should be able to recruit a top-notch CEO that values shareholders’ interests first and foremost. The Company has more than $72 billion in cash on its balance sheet, which could be used to buy back its shares or significantly increase its dividend. Also, we would not be surprised if this Nokia handset acquisition will lead to the Company splitting up into multiple smaller companies, which we feel will lead to a much higher enterprise value.

Much like buying Vodafone shares about a year ago, we believe the investors in Microsoft will be rewarded over the next 12 months. There is limited downside to the shares at these prices, and the news flow should only improve despite the slowdown in the PC market. We believe the sum-of-parts valuation of Microsoft is about $45 per share, and expect to see the shares trade there within the next 12 months.

© McIntyre, Freedman & Flynn