Executive Summary

- “Good” economic news in developed markets has been overshadowed lately by the “bad” (burgeoning Asian currency crisis) and the “ugly” (Syria).

- Unwinding central bank support from the markets will be arduous; it is already contributing to destabilization of certain emerging market currencies.

- News out of Washington this autumn — tapering, Fed leadership and the debt ceiling — has the potential to add volatility and uncertainty.

- The U.S. equity market has been the place to be this year, but diversification remains key.

As we have previously reported, getting back to “normal” will not be easy. But let’s start with some “good” news out of the developed markets. For second quarter 2013, Europe posted positive economic growth for the first time in seven quarters; the U.S. saw GDP growth revised sharply higher to 2.5%, from 1.7%; and data out of Japan suggest its economic growth will be revised to more than 4%, from 2.6%.

In the current environment, however, the “bad” and “ugly” always seem to be lurking nearby. The bad is represented by the 1997-style currency crisis brewing in India, Indonesia and Thailand. The ugly is Syria’s use of chemical weapons on its own citizens and the likely U.S. military response. The U.S. is being pulled kicking and screaming to a highly unpredictable crisis with unknown outcomes

and fallout, and any intervention apparently will come without approval from the United Nations or support from our stalwart allies in the U.K. Tomahawk missiles flying in the night to a distant land is definitely ugly.

Is all of this normal? Absolutely not. But it is the path to normal. We suspected the journey would be difficult, and it has been. Monetary stimulus is a double-edged sword — while it saved the financial system, unwinding the central banks out of the markets will be an arduous process, one that has already contributed to global credit excess and destabilization in Asian emerging market currencies.

Asian Crisis Redux

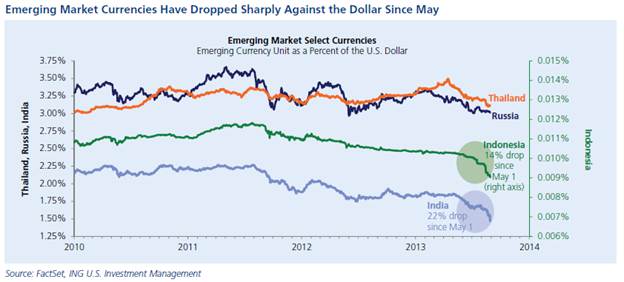

Mark Twain is reported to have said, “History doesn’t repeat itself, but it does rhyme.” If that’s true, then recent events in India and Indonesia sound a lot like those that precipitated the last Asian financial crisis in 1997. That year, a number of currencies collapsed due to the massive excess credit that had been extended to countries in the region — so-called “hot” money that exited in waves at the first sign of trouble. Thailand was the epicenter of hot money at the time, and the exodus of investors exposed the country’s large current account deficit, lack of foreign reserves and liabilities denominated in foreign currency. The financial crisis and the economic meltdown that followed ultimately forced the resignations of the leaders of Thailand and Indonesia, and South Korea was also badly scarred.

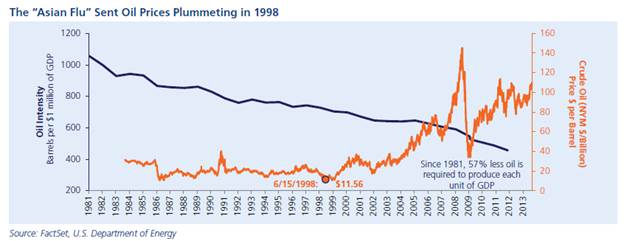

The Asian financial crisis taught us about the hazards of “contagion” — the tendency for financial stress in remote parts of the world to work its way to domestic shores. The “Asian flu”, as it came to be known, started off small — the DJIA lost 6.5% in October 1997 — but the tsunami soon gained strength. These fast-growing emerging market economies were badly damaged, hurting global growth expectations and sending oil plummeting to a low of $11 per barrel by mid-1998. The loss of oil revenue was too much for Russia, leading that country to a financial crisis of its own and ultimately bringing down the now-infamous Long Term Capital Management (LTCM), a hedge fund manager so leveraged that when it failed the Federal Reserve had to step in to prevent a meltdown of the financial system. Does any of this sound familiar? It should; it seems that when the Fed saves the financial system, it also sows the seeds for the next crisis.

Today, it is not hot money that is the primary issue; it is the systemic withdrawal of speculative credit from the emerging markets in the aftermath of the Fed’s unexpected announcement in mid-May that it was likely to soon begin winding down its unconventional bond-buying program (aka QE3). Asia has felt the brunt of the Fed’s rhetoric; India’s rupee is down 22% since May, for example, while the Indonesian equity market has lost 20% over the same period. But the effect has also been felt as far away as Turkey, which has been forced to raise interest rates in order to defend its currency.

All of this suggests that we are watching a bubble burst, and it leads us to believe the Fed will begin tapering off its bond purchases following its mid-September FOMC meeting. The markets realize the jig is up; money is flying out of the carry trade, resulting in plummeting currencies and surging bond yields.

Of course, emerging markets are much better capitalized now than they were 16 years ago, with considerably more foreign currency reserves to buffer the hot money withdrawals. So this looks like an evolving, but contained, crisis for now. Keep in mind that abandoning the equity markets during the LTCM crisis in 1998 proved to be an enormous mistake; while the S&P 500 corrected by 14.5% in August 1998, it returned more than 26% over the balance of the year as it began a multiyear rally to new all-time highs.

Fundamentals Remain Strong

While bad news from around the globe can have a day-to-day impact on market sentiment, it is ultimately fundamentals that drive long-term performance. Here is an update on our ABCDs of market fundamentals.

Advancing earnings growth. With second quarter earnings season almost complete, U.S. companies have once again managed to deliver growth; S&P 500 companies posted year-over-year earnings growth of 2.1% while establishing a new record for quarterly earnings per share. The financial and consumer discretionary sectors were notable standouts on the quarter, while the tech sector generated negative earnings growth.

Broadening manufacturing. Manufacturing activity in August, as reported by the Institute for Supply Management, expanded at the fastest pace in 26 months, coming in at 55.7. While manufacturing is not the powerhouse it once was, the sector has stemmed its decline and is on the upswing. According to the Boston Consulting Group (BCG), the U.S. is fast becoming one of the lowest-cost countries for manufacturing in the developed world. Additionally, BCG predicts that by 2015 average manufacturing costs in other developed markets such as Germany, Japan, France, Italy and the U.K. will be 8–18% higher than in the U.S, thanks in large part to cheap natural gas.

Consumer as the game changer. Consumer spending is holding its own. Retail sales rose to a new all-time high of $424 billion last month, and U.S. auto sales soared to pre-crisis levels. Revised second quarter GDP growth of 2.5%, up from the initial 1.7% estimate, was a pleasant surprise but was attributable to a more favorable trade picture, not an improvement in consumer spending. Housing remains a tailwind to spending, but the latest reports in the sector — including a 1.3% drop in pending-homesales — suggest a moderation in the rate of improvement as consumers grapple with higher interest rates and limited inventory.

Developing markets. Developing markets were hammered again in August, with the notable exception of China. The Shanghai Stock Exchange composite was up more than 3% for the month, buoyed by data suggesting a stabilization of Chinese economic conditions.

A Busy Fall on Tap in Washington

A busy, news-filled autumn in the U.S. will bring its own volatility and uncertainty.

• Congressional approval of a military strike against Syria may come any day.

• The FOMC will meet on September 18, with discussion of QE tapering likely on the table.

• President Obama will appoint a new Fed chairman, likely Janet Yellen or Larry Summers, within the next few weeks.

• Treasury estimates that the debt ceiling will be reached by mid-October, with a 2011-style standoff potentially triggering another ratings downgrade.

U.S. talk on Syria initially seemed to be more gamesmanship than an actual precursor to war; however, these things tend to take on lives of their own and demand close attention.

The government calendar, meanwhile, has a more predictable — and more significant — financial impact throughout the world. The Fed’s possible tapering of its quantitative easing program has had an enormous impact on interest rates in the U.S. and the emerging markets, as discussed earlier. Meanwhile, the infamous “sequestration” — draconion across-the-board cuts on government spending — has not been as bad as predicted; in fact, it has been quite salutary for spending and debt levels. Sequestration has helped reduce the deficit to 4.2% of GDP as of June from 10.2% in 2009, and federal government spending-to-GDP ratio is projected to fall to 21.5% by the end of the year from 24.8% just two years ago.

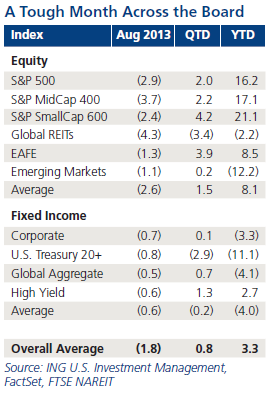

Despite a Poor August, U.S. Equities Have Been Strong in 2013

August was a month of extraordinary volatility across global equity and fixed income markets, with all asset classes negative for the month. Especially painful is the 11.1% year-to-date decline in long U.S. Treasury bonds, while troubled emerging market equities are down more than 12% for the year. The U.S. equity market has been the place to be this year, with small-cap stocks generating a whopping 21.1% return, and mid-cap stocks adding an impressive 17.1%; despite all the media attention paid to the larger end of the capitalization spectrum, the S&P 500 has been the domestic caboose, up only 16.2%. High yield bonds are the only fixed income asset class with year-to-date positive returns.

Building Wealth in Good, Bad and Ugly Markets

The message to investors is that global diversification builds wealth while helping to control risk. To wit: Despite the year-to-date carnage in emerging market equities and bonds of all stripes, a broadly diversified global portfolio has outperformed a defensive one. In fact, a portfolio based on a 60% equity/40% fixed income allocation gained 3% year to date through August compared to 4% decline for an all-fixed income strategy. It’s important to remember that risk is what you did not anticipate; investors who have tenaciously maintained a traditional defensive stance were preparing for the wrong risk, and they may have sacrificed wealth in the bargain.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 7324