I’ve written a lot lately on the subject of “duration” and its potential impact on investor portfolios, now that the initial goals of the Federal Reserve’s “Great Monetary Experiment” appear largely accomplished — and tapering of its monthly purchase of Treasuries to keep rates low is on the table. The era of lowering interest rates and rising bond prices looks finally at an end, with no place for rates to go but up. It’s vital, then, that investors think about the impact that rising bond yields could have on their portfolios. Here are a few scenarios we might see.

Treasury Yield Curve and Interest Rate Scenarios

As the Fed begins to reduce monetary accommodation, first through the tapering of its asset purchases and then eventually via a rise in interest rates, the Treasury yield curve should respond to this changing environment.

First, a reminder of the term duration. Duration is a measure of a bond’s sensitivity to rising rates. In general, the longer the bond’s maturity, the longer its duration, and the more sensitive its price will be to changes in market yields. The next four graphs, extracted from one of my papers on the subject of duration from earlier in the summer, illustrate a hypothetical sequence of yield curve steepening and interest rate raises. The levels of rates and yields are not our forecast – although we believe they are quite plausible, and there is no assurance that these will happen. (Since June when these charts were first published, the yield curve has already shifted higher.)

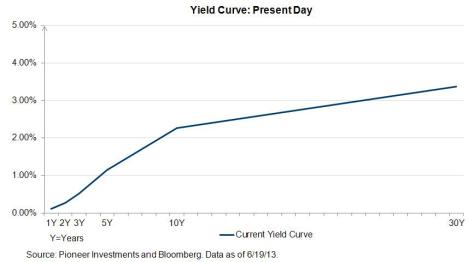

Yield Curve: Present Day

Scenario 1: This is what we see now, and assumes the Fed maintaining ZIRP (Zero Interest Rate Policy)

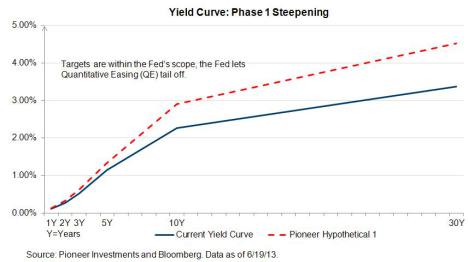

Yield Curve: Phase 1 Steepening

Scenario 2: Yield curve steepens as monetary velocity (the average frequency with which a unit of money is spent on new goods) picks up. Targets are within the Fed’s scope, the Fed lets Quantitative Easing (QE) tail off, credit expansion is offset by liquidity withdrawal. Investors are not getting overly anxious about Inflation.

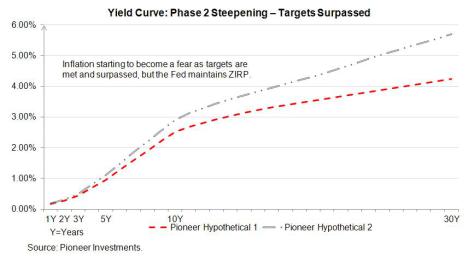

Yield Curve: Phase 2 Further Steepening as Targets are Surpassed

Scenario 3:Monetary velocity accelerates further. Inflation starting to become a fear as targets are met and surpassed, but the Fed maintains ZIRP.

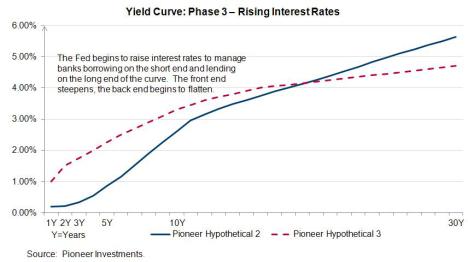

Yield Curve: Phase 3 – Rising Interest Rates

Scenario 4 :ZIRP Abandoned. The Fed begins to raise interest rates to manage the velocity through net interest margin contraction – the profit a bank derives by borrowing on the short-end of the curve and lending against the long-end. The front end steepens, the back end begins to flatten in response to higher interest rates.

The Stage is Set for Rising Rates and Changes in Fixed Income Markets

The stage is being set for a potentially significant change in the fixed income markets. Investors need to understand how the evolving landscape could affect them and the risks of duration on their existing portfolios. Click here to read Pioneer’s Blue Paper The Damage Potential of Rising Rates, in which we review these interest rate scenarios and the conditions that could invoke them, along with a broader discussion of duration.

© Pioneer Investments