China has been an incredible export engine of manufactured goods over the past decade and the central player of the BRICs era. But mounting competition from other countries is gradually pulling production away from China. How should investors proceed?

Although it’s hard to imagine a world without China as a manufacturing superpower, back in 1980 China was an insignificant exporter in global terms. It has consistently gained market share over the past 30 years and has accelerated strongly since 2001, when it joined the World Trade Organization.

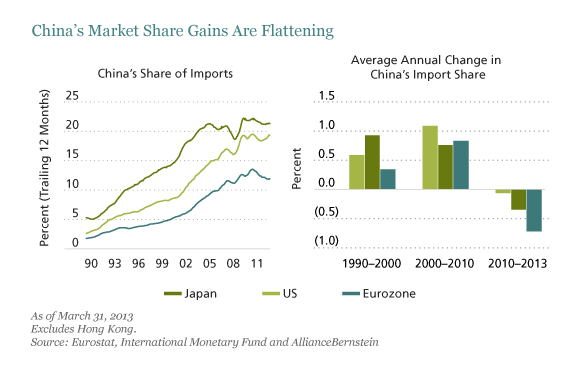

China’s Market Share Gains Are Flattening

It took China about 25 years to grab the first 10 percentage points of US import share, and only nine more years to double it. By 2010, China delivered 19% of all US imports and 29% of US imports of manufactured goods. However, since 2010, China’s market share gains have started to flatten (Display) because of rising labor costs and increased competition.

Investors shouldn’t really be surprised. Long-term shifts in global manufacturing power centers are actually quite common. For example, Japan became a major global exporter from 1950 to the mid-1980s—accounting for 20% of US imports at the peak in 1986. Korea and Taiwan followed suit in the 1970s and 1980s. But Japan and Taiwan relinquished their leadership after their exchange rates appreciated dramatically in the mid-1980s, making their exports comparatively expensive.

Which Industries Are Vulnerable?

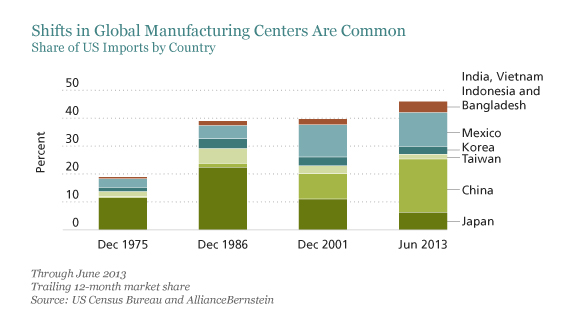

Today, we think investors should keep a close watch on China’s most vulnerable sectors. Signs of weakness can already be seen in apparel, toys, consumer electronics, computers and accessories, and machinery, according to recent US Census Bureau statistics.

US clothing imports from mainland China jumped from 8% in 2001 to 40% in 2010. Over the same period, US apparel imports from Mexico, the Dominican Republic, Honduras and El Salvador tumbled from 25% to 12%. However, in the last two and a half years, China has lost more than five percentage points of US market share for clothing, with Vietnam, Bangladesh, India and Indonesia filling the gap.

Vietnam Is a Big Winner

Vietnam has been a big winner from a series of free trade agreements over the last decade including its ascension to the WTO in 2007. Nike already makes 40% of its shoes in Vietnam—more than in China. In our view, investors should look out for other multinationals in footwear and apparel—and their suppliers—that could reap significant cost benefits from expansion outside China.

Even in electronics, where China looks more resilient, change is imminent. Despite its strong supplier base and other competitive advantages, China’s market share gains have stagnated—and Vietnam has doubled its share from a very low base. Following Intel in 2010, Samsung, Nokia and others have invested in factories in Vietnam.

Mexico Gains Attention in Autos

China’s ambitions to penetrate higher-end manufacturing sectors such as autos, aerospace components and industrial equipment, could be thwarted by Mexico. Mexican auto production is poised to rise from 2.9 million vehicles in 2012 to about four million in five years, as global carmakers such as Volkswagen, Nissan and Honda increasingly use Mexico as an export base, lured by competitive labor costs and preferential trade agreements.

We believe that Mexico and Vietnam are well positioned to gain market share in world exports, while India, Bangladesh and Indonesia are also likely to play a role in the manufacturing shift away from China. It won’t happen overnight and some Chinese companies will adapt to these challenges by moving upstream or out of China themselves. Investors will need to understand how these shifts are unfolding in order to identify companies that are poised to benefit from the growing threats to China’s manufacturing dominance.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.

Sammy Suzuki is Portfolio Manager—Emerging Markets Core Equities and Director of Research—Emerging Markets Value Equities at AllianceBernstein.

© AllianceBernstein