Comments from the Federal Reserve to begin reducing its stimulus operations have weighed heavily on markets across Asia in recent weeks. Growing investor concerns have largely centered on those economies that have been running current account deficits and that are likely to be further impacted by lower growth forecasts and reduced capital inflows. More short term, speculative flows from investors into fast-growing Asian economies have also fallen as expectations for higher interest rates in the U.S. have risen.

Two of the most affected markets in the region have been India and Indonesia as their economies face similar challenges. In order to grow their economies, both India and Indonesia require sufficient capital inflows in the form of exports and Foreign Direct Investments (FDI). However, with a lackluster manufacturing sector and falling FDI inflows, both countries run the risk of further weakening currencies and higher inflation that will ultimately lead to lower economic growth. A recent World Bank report downgraded Indonesia's growth to 5.9% citing weaker-than-expected Foreign Direct Investment and softer commodity prices. Headline inflation for July also came in at 8.61% year-over-year—much higher than the consensus estimate of 8.04%—driven by the Muslim fasting period, Ramadan and a hike in fuel prices. In June, policymakers in Indonesia aimed to reduce wasteful subsidies by increasing the price of gasoline as much as 44%.

Similar to Indonesia, India also has wide fiscal and current account deficits and high inflation. In late July, India's government cut its growth forecast to 5.5%–6.0% in the year through March 2014, far slower than the 6.1%–6.7% expansion the government estimated in its federal budget in February. Additionally, concerns of the impact of tapering of monetary stimulus in the U.S. have significantly weakened the Indian currency in recent weeks. The Indian government may be aiming to plug the gap in funding the country's current account deficit by increasing reliance on shorter-term sources of funding. Recent measures announced by the Indian government and the Reserve Bank of India (RBI) suggest that policymakers are viewing the rupee movements as a short-term issue while paying less attention to some of the structural problems confronting the economy.

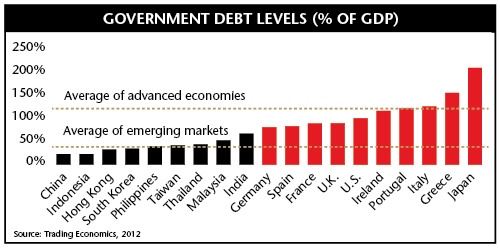

Growth momentum may have slowed in Asia, and indeed there are short-term issues in some countries in the region, particularly those running current account deficits that need to be addressed. However, at Matthews Asia, we do not believe it is crisis time circa 1991 in India and 1996 in Indonesia, nor do we see this as a trigger for a larger regional crisis. One of the key saving graces is that in both these countries, the component of foreign debt to GDP ratio is lower than in the past. We are also beginning to see more decisive action from respective governments in Asia with structural reforms being initiated.

Over the long term, we believe that the drivers of short-term volatility in countries such as Indonesia and India could spark their governments to make much needed structural reforms which could lead to greater long-term growth in the ASEAN region. While there is a short-term risk of contagion, these markets are more domestically driven than they have been in the past and less susceptible to longer-term dislocations.

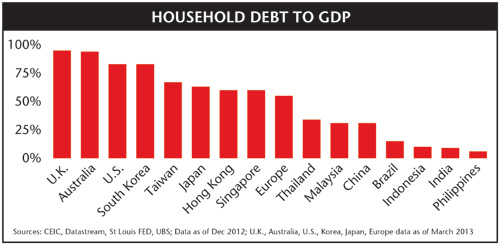

Asia is still a region of strong demand and we don't believe that this marks an end to the region's long-term growth story. The majority of countries in Asia are in a far better position with lower levels of external foreign currency debt, higher foreign reserves, fast-growing rates of productivity and wealthier populations with lower levels of household debt than their Western counterparts.

Asia is still a region of strong demand and we don't believe that this marks an end to the region's long-term growth story. The majority of countries in Asia are in a far better position with lower levels of external foreign currency debt, higher foreign reserves, fast-growing rates of productivity and wealthier populations with lower levels of household debt than their Western counterparts.

While this period of market uncertainty continues, our portfolios will be affected. However, as long-term fundamental investors we remain focused on identifying attractive businesses to hold through-out full market cycles. In addition, as more attractive valuations emerge in countries such as India and Indonesia, we may have many new opportunities with which to implement our long-term view.

You should consider the investment objectives, risks, charges and expenses of the Matthews Asia Funds carefully before making an investment decision. This and other information about the Funds is contained in the prospectus and summary prospectus which may also be obtained by calling 800.789.ASIA (2742). Please read the prospectuscarefully before you invest or send money as it explains the risks associated with investing in international and emerging markets. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation.

The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Matthews International Capital Management, LLC does not accept any liability for losses either direct or consequential caused by the use of this information.

Matthews Asia Funds are distributed in the United States by Foreside Funds Distributors LLC

Matthews Asia Funds are distributed in Latin America by HMC Partners

© 2013 Matthews International Capital Management, LLC

© Matthews Asia