Stocks CLose Out Disappointing August

Equity markets concluded an ugly month of August with another down week, as concerns surrounding a potential Syrian intervention rattled investors. For the month, the S&P 500 declined 2.9% while the Dow Jones Industrial Average lost 4.1%. That was the worst month for the Dow since May 2012.

Economic data was generally disappointing last week, with a smattering of reports occurring before the holiday weekend.

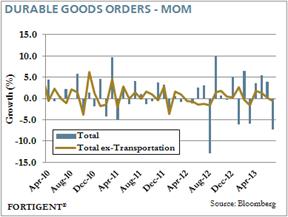

On Monday, the Census Bureau reported that durable goods orders contracted by 7.3% in July, led down by the transportation component. A decline was expected following three straight months of gains, but consensus called for only a 4.0% drop. The transportation component alone fell 19.4%, led down by nondefense aircraft.

More troubling, however, was weakness at the core, which strips out this volatile transportation component. The core reading slipped 0.6%, which was 0.9% below expectations. Losses were concentrated in computers & electronics and electrical equipment. Softness in core new orders data continues to bring the health of the US manufacturing sector into question.

On the housing front, the S&P/Case-Shiller Home Price Index continued to rise in June, increasing 0.9% during the month and 12.1% year-over-year. June’s figure was slightly below expectations, and a bit below the pace of 1.4% observed during the first five months of the year. The pace of year-over-year gains has also leveled off in recent months after nearly two years of continued improvement. Tuesday’s report is the latest evidence that the recent back up in mortgage rates is starting to eat away at the rebound in the housing market.

One of the bright spots of the week occurred on Thursday, when second quarter GDP was revised upward to 2.5%. The initial estimate suggested the US economy grew 1.7% in the period.

The new estimate was boosted by an increase in exports that was larger than previously estimated. The quarterly trade balance was also aided by a downward revision to the level of imports. In comparison to the previous quarter, second quarter GDP advanced due to an increase in personal consumption expenditures, exports, and private inventory investment. These were partly offset by a dip in federal government spending.

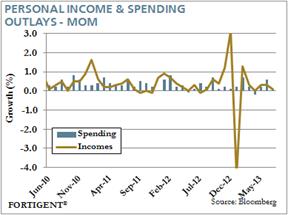

Third quarter GDP may not shape up quite as well as the second quarter, as the personal income and spending outlays report came in flat for July. Friday’s figure of 0.1% for consumer spending disappointed consensus and represents a sharp drop from 0.6% growth in June. Income was also tepid, increasing just 0.1%. A lack of wage growth will put continued pressure on the US economy as spending gains will only come through reduced savings and increased debt leverage.

Fixed Income – where to noW?

Since the end of the Global Financial Crisis (GFC), investors moved aggressively into fixed income asset classes. They were quickly rewarded in the years following the crisis with a combination of falling interest rates and tighter credit spreads, which led to positive absolute returns. The easy money in fixed income is gone, however, and now is the time for careful asset class selection.

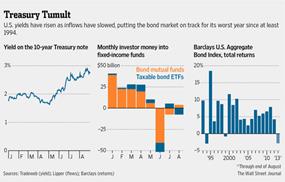

Year-to-date through August, the Barclays Aggregate Bond Index is down 2.8%, the first negative calendar year performance in more than a decade. The primary culprit behind the negative returns is the sudden rise in Treasury yields, with the 10-year U.S. Treasury yield moving from 1.76% at the start of the year to 2.78% more recently.

Source: Wall Street Journal

The sudden rise in interest rates is causing many investors to reconsider their fixed income exposure. After years of massive flows into fixed income funds, investors withdrew more than $57 billion from taxable fixed income mutual funds in the last three months.

There are strong signs that fixed income markets are at an inflection point that requires investors to tread very careful. From a technical perspective, 10-year Treasury yields are nearing Fibonacci resistance levels, suggesting a possible rally in bonds and a decline in interest rates.

Source: Humble Student of the Markets

Additionally, the Commitment of Traders report shows speculators moving to a crowded short position in Treasuries, suggesting there is little additional support to push Treasury yields higher.

Source: Humble Student of the Markets

Despite the potential for a rally, investors are likely to remain bearish due to recent levels of volatility. Recent readings of the Merrill Lynch Option Volatility Estimate MOVE Index, which shows volatility across the Treasury term structure, are the highest since the S&P downgraded the U.S. debt rating in mid-2011.

Source: Bloomberg

Within credit sectors, similar concerns exist, but fears are not as pronounced. The Barclays High Yield Index has a spread of 4.5% over Treasuries currently, with an absolute yield of more than 6.3%. In investment grade, yields are around 3.4% with a spread of 1.4%.

Credit sectors have performed relatively better this year, with the BofA ML US HY Master II Index up 2.8% through August, However, this is nowhere near the 15%+ returns investors became accustomed to in 2009, 2010 and 2012. The sharp rate increase drove a 2.7% loss in June for the high yield sector, which was the biggest monthly loss since late 2011.

Treasury markets are expected to remain volatile given upcoming debates around the debt ceiling and discussions over the federal budget. While credit sectors will be impacted by some of that volatility, higher yield areas of the market are likely to see investors move slowly back in their direction. The thirst for yield remains strong around the globe and the recent back up in rates only served to make high yield a more attractive option for investors.

The Week Ahead

Economic data picks up this week, with several important reports spanning the holiday-shortened period. This includes the ISM manufacturing index on Tuesday and the government jobs report on Friday. Consensus is looking for a 175,000 increase in jobs in August following a slightly disappointing July.

Discussion surrounding possible US involvement in Syria will likely dominate headlines and markets this week. The latest news indicates that the President will not act unilaterally without Congressional approval.

Given the legislature’s current posturing, there may be a lower probability of military action occurring, although that is far from certain. Markets thus far appear to be negatively predisposed to any involvement.

The Bank of Japan, Bank of England, and European Central Bank meet this week, although no major shifts in policy are anticipated. Other central banks releasing monetary policy guidance are Sweden, Malaysia, Mexico, Canada, Poland, and Australia.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent