· For those in college during the 60s – the time of “sex, drugs, and rock 'n roll” – it’s hard to believe that marijuana has become legal. It is currently legal in some form in about 20 states and more are considering it, at least for medical purposes. Even Florida has strong proponents for the medical use of marijuana. There are always people who are trying to take advantage of the situation and this is no exception. Scammers are making phone calls to investors talking about companies that will grow marijuana and/or provide marijuana and offering the potential investor a chance to “get in on the ground floor”; meaning send them money for worthless stocks, not for marijuana. Should you get one of these phone calls, tell the caller to stuff it in a pipe and smoke it.

· Is the real estate industry still a bright spot in an otherwise slow growing economy? Or is it slowing down or potentially heading into a recession? The answers are: most likely, maybe, and not very likely. In July, new home sales declined dramatically, down 13.4% as represented by new contracts. For the twelve months ending in July, however, new home sales were up 7% year over year. It should come as no surprise that, with long term interest rates rising significantly since May, it might take a few months for people to readjust to higher rates as they consider a new home purchase. For those born after 1980, it may seem the current rate on a 30 year mortgage (about 4.5% on a conventional basis) is high when compared to 3.3% just a few months earlier. However, those of us that purchased homes in the 70’s were delighted to get a mortgage for 14%. Thus, rates are still low by long term historical standards, but from recent history it seems like a shock. Once people adjust, we should see a pickup in new home sales again. By the way, if you are in the market for a new or resale home, do NOT be tempted by the lower rates of an adjustable mortgage unless you plan to sell the home within the low rate window. Just when the window opens for a higher rate, you may be kicking yourself for not having opted for a fixed rate loan. Be sure to run the numbers before being tempted by the lower rate. (Source: Commerce Department)

· As a matter of convenience and ease, many people are using target date funds inside of their 401(k)s. A target date fund is designed to create a portfolio supposedly consistent with one's age. That is to say, as the mutual fund owner gets closer to retirement, the fund increases its exposure to bonds and cash, leaving less allocated to equities. This is a traditional approach to risk reduction but it isn’t one we necessarily agree with for everyone. In today's environment, people may be very disappointed in the results of their target date funds since bonds are likely to decrease in value over the next couple of years as interest rates go up. These target date funds did not protect investors during the downturn, and they may not again over the next couple of years. While making it "easy" for an investor to participate in the markets, they must be watched carefully. If you or a family member are using target date funds, dig down deep to truly understand them to see if they are the type of investment you really want. For most people, we believe that they should set up their own portfolio inside of the 401(k), but only after getting professional advice.

· With some Baby Boomers working past age 66, it may make sense to delay taking Social Security as the payment increases 8% per year until age 70. The benefits go beyond the increased payments. Since Social Security is inflation adjusted, the cost of living increase throughout life will be on a larger amount, and because a surviving spouse can receive either his/her own Social Security or that of a deceased spouse, this benefit could continue for 20 to 30 years. This is especially beneficial when there is a disparity in Social Security benefits. Suppose one spouse is due the maximum benefit, while the other spouse has a much lower benefit. What can they do in retirement? When the spouse with a larger income reaches full retirement age (currently age 66), he/she can go through the process of "filing and suspending". This allows the other spouse to file under the higher income spouse’s Social Security benefit once the lower income spouse reaches at least age 62. But, if possible, it’s better to wait until full retirement age otherwise there is a reduction in the benefit. Because the higher income spouse suspended Social Security benefits, his/hers continues to increase 8% per year. But let's suppose that the lower income spouse’s Social Security benefit is better than 50% of the higher income spouse. Obviously he/she would be better off filing on his/her own. But here's the interesting twist; if the high income spouse has reached full retirement age, he/she could file for a spousal benefit and receive 50% of the lower income spouse’s Social Security benefit, even while continuing to work and watching his/her own Social Security increase by 8%. At age 70, the higher income earning spouse would give up the spousal Social Security benefit and then file on his/her own. There are lots of subtle ways to maximize Social Security benefits. If you are between the ages of 62 and 66 and have not yet talked to us about your Social Security benefits, please don't hesitate to give us a call for assistance.

· It's hard to believe that the summer is almost over and that by next week almost all children will be back in school. This is a good time for parents to reflect on how they might pay for a college education. Too many students graduate from college with too much debt, and as a result start off life behind the proverbial financial eight ball. By doing a little planning, parents or grandparents can go a long way to ensuring that students start off life after college with much less debt. One of the more practical ways to save for a college education is the use of a Section 529 plan. Although the money deposited into a plan is not tax deductible, it does grow tax-deferred, and when withdrawn for qualified educational expenses, it comes out tax-free. In some states there are income tax benefits to contributing to a state-sponsored plan, so be sure to check on various plans when you are considering setting up a 529 plan. Saving a little bit on a regular basis, and then adding larger gifts along the way, can create a tidy sum to help offset the costs of a college education. What happens if the student doesn't go to college, or use all the funds? The money can be transferred amongst family members, including brothers, sisters, cousins, etc. If you've never thought about setting up a Section 529 plan for your children/grandchildren, please let us know and we will provide you with some additional information.

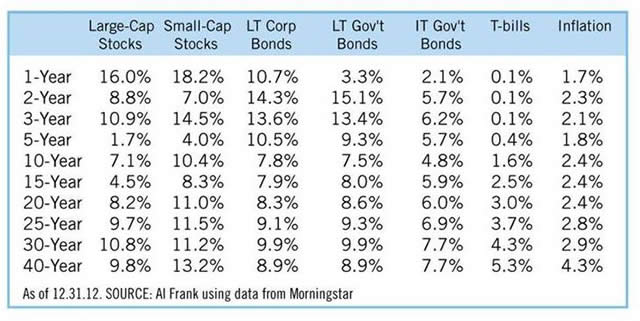

· The chart below was provided to us by our good friends at Al Frank. It helps put in perspective the importance of long-term investing. Although it's easy to see the underperformance of large-cap stocks over the past five, 10, and 15-year time periods, we see a significant upward trend when looking at 20 years. Is it possible that there will be a reversion to the mean over the next five to 10 years and stocks perform closer to their long-term averages? The chart also shows the importance of diversification by adding small-company stocks to a portfolio, along with long-term corporate bonds, long-term government bonds, intermediate term government bonds, and even T-bills. But it also shows that long-term corporate and government bonds have produced above average returns over the past five years, so is it possible that there will also be a reversion to mean averages for bonds but in a downward direction? Obviously, no one knows for sure what the markets will do going forward, but the pendulum moves in both directions for both stocks and bonds.

· During the third week of August, which included the release of the Federal Reserve Board’s notes, investors withdrew $14.3 billion from equity mutual funds and exchange traded funds. Approximately $10 billion of this came out of the SPDR S&P500 EFT all by itself. Where did the money go? Money market mutual funds took in $22 billion that same week. If you are a contrarian investor, you would see this as a positive sign because traditionally the small investor does the wrong thing at the wrong time. In other words, when small investors are fleeing the markets, it's time for the smart investors to be jumping in. Whether this holds true or not in the short term remains to be seen. However, those same investors have to get it right twice, because they have a tendency to get back into the market when it's higher than when they got out.

· Congress will be returning to Washington right after the Labor Day weekend. As we've mentioned before, they need to tackle the budget and the debt ceiling. Here is a frightening fact that cannot be ignored on a long-term basis: the national debt reached $16.739 trillion as of July 31, which is twice as large as the $8.371 trillion national debt as of March 31, 2006. If you take all of the debt from the beginning of our country to March 2006, approximately 230 years, the debt doubled in only seven years and four months. During that seven year stretch, we experienced the 12 largest monthly deficits in our history. We cannot continue in this manner. Fortunately, the deficit this year will be the lowest in the past seven years, but still way too high. (Source: Treasury Department)

· We don't know how we let the date slip by, but on April 15 this year, we should have "celebrated" the 100th birthday of federal income taxes. When Congress first passed the law creating income taxes, taxpayers were expected to pay 1% of the first $20,000 of taxable income. That's a far cry from the top rate of 39.6% which, of course, doesn't include the additional tax to fund Obama Care. While we’re talking about taxes, it is estimated that the average American only pays about 85.5% of what they should pay in taxes. This is a result of taking unreported income and/or overstating deductions. As a result, Uncle Sam is losing an estimated $385 billion or more than 50% of this year's anticipated deficit. (Source: Internal Revenue Service)

· While much of the summer saw the market move sideways with a general bias to the upside, the last three weeks of August saw increased volatility and a decline of about 5% from the all-time market highs that were set in the early part of the month. This 5% setback has given the pundits an opportunity to talk about the market’s continued slide, and it's possible it could. Even after this pullback, both the Dow Jones Industrial Average and the S&P 500 are up over 15% year to date. It would not surprise us to see some additional ground lost over the next couple of months, but it is not likely the start of a new trend for the market. Yes, there will be lots of days that negative news on both the financial and political fronts will seem like we are in a bad place. The last time we were at these record levels, the 10 year treasury had a yield of approximately 5%, and today it is about 2.7%. The earnings for the S&P 500 were about $85, while this year they will approach $104 and projections for next year run anywhere from $115 to $122. Real estate, both commercial and residential, was in the early stages of decline from a raging bubble, while today both are in the early stages of a recovery. Corporate balance sheets were not nearly as secure as they are today, especially as it relates to the cash balances. In short, look past the next few months of potentially unsettling news and there should be a reasonably bright future ahead. Look past the noise, and look at the facts.

As always, we encourage you to give us a call if you would like to discuss anything further. We will visit again soon. Proudly and successfully serving our clients for over 26 years.

RAY, KIM, ERIC, BRUCE, LOU, NANCY, TINA, JON, STEVE and DOROTHY

© 8/30/13 ProVise Management Group, LLC

This material represents an assessment of the market and economic environment at a specific point in time. Due to various factors, including changing market conditions, the contents may no longer be reflective of current opinions or positions. It is not intended to be a forecast of future events, or a guarantee of future results. Forward looking statements are subject to certain risks and uncertainties. Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by ProVise), or any non-investment related content, made reference to directly or indirectly in these Bullets, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in these Bullets serves as the receipt of, or as a substitute for, personalized investment advice from ProVise. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Information is based on data gathered from what we believe are reliable sources. The information contained herein is not guaranteed by Provise Management Group, LLC as to accuracy does not purport to be complete and is not intended to be used as a primary basis for investment decisions. The indices mentioned are unmanaged and cannot be directly invested into. ProVise is neither a law firm nor a certified public accounting firm and no portion of these Bullets should be construed as legal or accounting advice. A copy of ProVise’s current written disclosure discussing our advisory services and fees is available for review upon request. If you do not want to receive the ProVise Bullets, please contact us at:[email protected]or call: (727) 441-9022. Please visit our Web Site at:www.provise.com.

Dow Jones Industrial Average - The Dow Jones Industrial Average is a popular indicator of the stock market based on the average closing prices of 30 active U.S. stocks representative of the overall economy.

S&P 500 Index is an unmanaged group of securities considered to be representative of the stock market in general. You cannot directly invest in the index.

© ProVise Management Group