Tensions and the humanitarian disaster in much of the Middle East have continued to worsen over the last several weeks, with United States forces now standing ready to move into Syria, andEgypt’s future looking increasingly unsure.

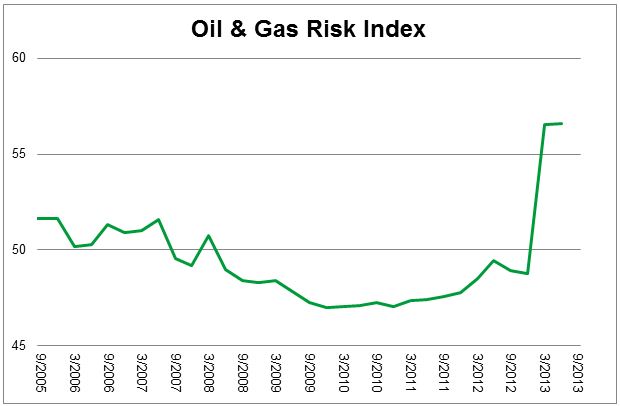

Unfortunately, there is little evidence that the violence and civil unrest is diminishing. As the chart below shows, an index of geopolitical risk in oil-producing countries recently hit a multi-year high. Elevated levels of the index have historically been associated with higher oil prices.

In fact, oil prices have already jumped this weekon concerns over military action in Syriaand a further escalation in violence in the Middle East would not only have a terrible human toll, itcould also lead to oil prices rising further. This is becausethe oil marketisalready tighter than most market watchers realize. Consider the following:

- Significant Middle Eastern and African production has already been lost because of recent unrest across the region. Due to sanctions, Iranian exports are down from a peak of more than 2 million barrels per day to less than 1 million barrels daily. Meanwhile, civil unrest has led to production cutbacks in Nigeria, Libya, Iraq, South Sudan, and, of course, Syria. While Syria was never a major oil producer, production has fallen from a pre-crisis peak of roughly 380,000 barrels per day to virtually nothing.

Whilerising US productionhas prevented a violent spike in crude, less supply from the Middle East and Africa has kept oil prices elevated and is one reason crude oil has generally outperformed the broader commodity complex year-to-date.

- While theOrganization of Petroleum-Exporting Countries (OPEC)does have significant spare capacity, the majority of that spare capacity is of a type that is sub-optimal for refiners. The spare capacity, mostly in Saudi Arabia, is mainly heavier, sour crude that is problematic for many refineries to handle.

While it’s impossible to predict how events in the Middle East will unfold, any further escalation in violence risks taking more supply offline and driving oil prices higher. Should this happen, consumption will likely fall from already tepid levels as higher oil will put more pressure on US consumers still struggling with low income growth and higher taxes.

Higher oil prices act as a tax on consumers in the form of higher gasoline prices. This is particularly true in the United States, where gasoline taxes are low and increases in crude translate fairly quickly into higher gasoline prices. To the extent gasoline prices rise, this typically comes at the expense of discretionary purchases. In the past categories such as apparel and restaurants have been quickly impacted by such spending cuts.

And as rising oil prices would be yet another brake on consumer spending in an environment in which many households are still living pay check to pay check, slowing spending could hurt the US and global recoveries. In addition, as evident in market performance earlier this week, the possibility of rising oil prices isa risk adding pressure on financial markets.

So where does this leave investors? As I’ve mentioned before, I expect thatmarket volatility is going to pick up into the falland based on this assumption, I advocate trimming some exposure to risky assets such as high yield bonds andparts of the equity market that look particularly extended year-to-date. In addition, I continue to suggestremaining cautious on sectors that rely on consumptionsuch as the consumer discretionary and consumer staples sectors.

© iSharesBlog