ING Fixed Income Perspectives August 2013

Bond Market Outlook

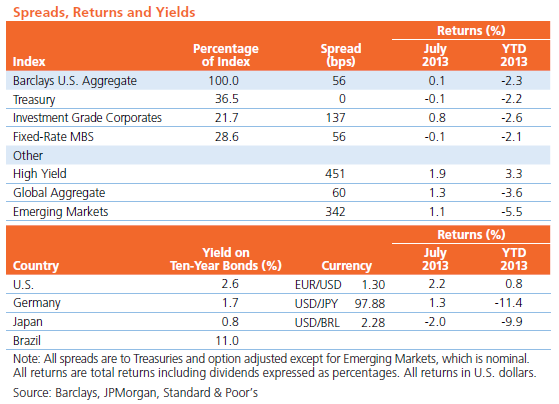

Global Interest Rates: Fed tapering is on the horizon, but the near-term impact is largely priced in. We favor select exposures to peripheral Europe.

Global Currencies: We continue to favor the U.S. dollar and have become more constructive on the euro; emerging markets are attractive, but idiosyncratic risks leave us cautious.

Corporates: Fundamentals are better than average, but the trend is still negative. Volatility could pick up as we draw closer to the start of Fed tapering.

High Yield: We remain constructive, though upside is more limited after July’s recovery.

Mortgages: Valuations are fair, but Fed tapering fears and interest rate volatility warrant caution.

Emerging Markets: We expect the technical picture to remain negative, trumping fundamentals for the remainder of the year.

Macro Overview

- While it’s been said that a picture is worth a thousand words, some pictures are just not that complicated. Take the current U.S. yield curve, for example, our interpretation of which can be boiled down to just a handful of syllables: “zero interest rate policy” and “taper”.

- The historically steep gradient of the current yield curve is a function of how markets have priced the relationship between the Fed’s plans to taper its asset-purchase program and its zero interest rate policy (aka ZIRP). The front end of the curve clearly depicts the market’s expectation that Bernanke and any of his likely dovish successors will keep the overall level of interest rates low by anchoring the federal funds rate well into 2015. The back end of the curve, meanwhile, reflects the more opaque taper picture that the Fed started to paint for us back in May.

- The yield curve steepened sharply in the aftermath of the Fed’s taper announcement, as the market began to price, re-price and mis-price what a normalized term premium should look like absent extraordinary Fed influence. This inability of the market to elegantly express the difference between the looming end of quantitative easing and the more-distant end of ZIRP has also pushed interest rates higher across the curve. Given the absence of inflationary pressures, though, the picture going forward is likely to be flatter and higher —led in a disproportionate degree by the front end of the curve — as the market transitions its attention from the wind-down of quantitative easing to the eventual tightening of monetary policy.

- Though a September taper appears priced in, the picture for fixed income could get blurry if the market remains unable to process the Fed’s two-pronged strategy to unwind its extraordinary accommodation. In the meantime, it makes sense to hold dry powder with a bias toward those fixed income asset classes tied to credit risk and more removed from interest rate risk. Longer term, as interest rates begin to normalize in a post-taper world, the resiliency of developed markets will eventually buoy emerging markets, providing opportunities in spread sectors that still look cheap from a fundamental perspective in the wake of the recent selloff.

Sector Overviews

Global Interest Rates

- Inflation is trending lower, and with no signs of inflationary pressures on the horizon the December 2015 barometer for the fed funds rate has retraced from 1.25% to 0.95%. Interest rates are slightly above fair value in most G-10 countries and are showing some lingering signs of fundamental cheapness. The fair value of rates is likely to increase gradually as economic growth improves, the rate of fiscal tightening slows and Fed tapering gets underway.

- We have a broadly negative view on rates in the intermediate term. However, we do favor select exposures to peripheral Europe; conditions in the region have improved, while an increasingly dovish European Central Bank provides fundamental support and various pan-European safety mechanisms help diminish tail risks. Countries like Portugal and Ireland have outpaced fiscal targets and have the potential to benefit from Europe’s improved growth outlook.

Global Currencies

- Despite its recent weakness, we continue to favor the U.S. dollar and its relative fundamental strength, though an improved European growth outlook makes us more constructive on the euro. We remain bearish on the Japanese yen. And while we see value in the emerging markets, we are still expressing caution due to idiosyncratic risks; however, we are dialing up exposures in more liquid emerging currencies, like the Mexican peso, that will benefit from stronger U.S. growth and improved expectations for emerging market growth. As commodities prices — particularly oil — bottom and rebound, we also favor the Norwegian krone.

Investment Grade Corporates

- Risk sentiment has improved thanks in part to the stabilization of interest rates and better-than-expected economic data; financial issues and long-dated bonds have been the primary beneficiaries. Liquidity is still robust, though the new-issue calendar is expected to soften a bit.

- While corporate fundamentals are better than average, the trend remains negative. Earnings data continue to outpace lowered expectations while revenue disappoints. Sales and capital expenditure growth have slowed sharply over the last two years; while sales seem likely to rebound as global growth reaccelerates, the path for capex is less clear given the recent weakness in commodity prices. Spreads thus appear fairly valued, and “carry” or yield will be the most likely driver of excess returns.

High Yield Bonds

- High yield fundamentals are in good shape, though gains in revenues and earnings are increasingly difficult to come by and outflows remain slightly negative. Solid balance sheets limit the near-term potential for a spike in defaults. The relationship between spreads across rating categories has not changed materially, suggesting investors are comfortable with credit risk and are instead focusing their concerns on the prospect of higher rates.

- With valuations more attractive than they had been earlier this year, we remain constructive on high yield, though the upside is more limited after July’s recovery. Thematically, we continue to favor energy, specifically oil over natural gas, and are looking for opportunities that benefit from the European recovery story.

Mortgages

- The near-term performance of mortgages has been dominated by flows and fears of Fed tapering. The limited supply from originators at these higher rate levels gets gobbled up by the Fed or hedge funds, driving the mortgage basis tighter; however, the expectation of tapering and uncertainty about the next marginal buyer have driven spreads wide of their pre-QE3 levels. Agency RMBS valuations are fair and technical demand remains positive, but rate and basis volatility have been increasing and warrant caution.

- We are constructive on non-agency RMBS as rates stabilize, dealer inventories decline and house prices trend higher. But the asset class remains susceptible to fatigue in terms of potential unanticipated supply from the government-sponsored enterprises (GSEs) selling legacy paper as well as interest rate volatility driven by fears of Fed tapering. We are more constructive on CMBS. The new-issue pipeline appears quite manageable. And while the GSEs have large inventories to sell, the paper is of high quality and likely to attract strong demand, particularly from insurance companies.

Emerging Markets

- Outflows from emerging sovereigns continue as developed market rates move higher. Lower commodity prices and reduced Chinese demand have also hurt emerging markets, though turbulence in the Middle East could provide some support for energy prices and offset downside risks related to slower Chinese growth. However, the technical picture will likely trump any positive fundamental developments for the remainder of the year.

- Stabilization in U.S. rates and improved economic data have helped emerging market corporates recover, though the rebound has been lackluster relative to other markets. Emerging corporate fundamentals will likely weaken versus U.S. issuers due to greater commodity exposure, and risk sentiment is likely to favor developed markets relative to emerging markets and widen the interest rate spread between them.

ING U.S. Investment Management’s fixed income strategies cover a broad range of maturities, sectors and instruments, giving investors wide latitude to create a new portfolio structure or complement an existing one. We offer investment strategies across the yield curve and credit spectrum, as well as in specialized disciplines that focus on individual market sectors. We build portfolios one bond at a time, with a critical review of each security by experienced fixed income managers. As of December 31, 2012, ING U.S. Investment Management managed $127 billion in fixed income strategies in the United States.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 7283