Many investors have been conditioned to accept that the economy will be in the rehabilitation ward for the foreseeable future, rates will remain low, and monetary stimulus unending. We believe this is an increasingly dangerous mindset and the next great risk for bond investors is coming into view: the return of higher interest rates. We look at the “refuge” subsectors – those areas of the fixed income market that investors may believe provide “safe haven” from the gathering storm. The third in a series of three papers.

Key Points

- It has been nearly five years since the near-collapse of the global financial system. Investors have been conditioned to accept that the economy will be in the rehabilitation ward for the foreseeable future, rates will remain low and monetary stimulus unending.

- While we think it is unlikely that investors will be tested by a “Duration Blowback” (a dramatic rise in yields and decline in bond prices), the need to reduce exposure to the next phase of the fixed income cycle – the return of higher interest rates – is growing.

- Duration is a measure of a fixed income instrument’s sensitivity to rising rates. While duration can be a painful harbinger of the possibility of principal loss in a rising yield environment, not all duration is bad. Indeed, spread duration has the ability not only to help cushion the loss but also to provide strong and positive excess returns in a rising yield curve and interest-rate-environment.

- We take a look at the fixed income subsectors that are being viewed as “refuges” from what may be a turbulent transition to higher rates.

The Next Big Challenge to Investors: Duration

It has been nearly five years since the near-collapse of the global financial system, and the world is still dealing with its fallout. Investors have been conditioned to accept that the economy will be in the rehabilitation ward for the foreseeable future, rates will remain low and monetary stimulus continues.

We believe that this is an increasingly dangerous mindset and the next great risk for bond investors is coming into view. While we think it is unlikely that investors will be tested by a “Duration Blowback” (a dramatic rise in yields and decline in bond prices), the need is growing to reduce exposure to the next phase of the fixed income cycle: the return of higher interest rates.

In the last couple of months investors experienced the market’s “shot across the bow” as 10-year Treasury rates backed up almost 100 basis points and the yield curve steepened. Almost all fixed income asset classes convulsed, selling off in response to the first indications that the bond “Bull Market” could be coming to an end. In this instance, investors were responding to the possibility that Quantitative Easing (QE) would be tapered sooner than expected. How will the market respond when the data begins to reveal that the U.S. recovery is finally starting to gather steam?

Even without a violent upwards move in interest rates, high quality fixed income investments may struggle to provide a positive return and could be the next great source of risk in investors’ portfolios. We continue to advocate caution and a move into strategies that have the ability to help protect from a rising yield-curve and interest-rate environment. Over the course of this final installment in “The Danger of Duration” we will examine the most popular sectors that have historically proven to be “safe havens” from rising rates.

Not all Duration is Created Equal, and Not All is Bad

A simple definition of duration is that it measures the severity of an investment’s value to interest rate changes. More specifically, as we described in the second installment of the “Danger of Duration” it is:

“a measure of a fixed income instrument’s sensitivity to rising rates. In general, the longer the instrument’s maturity, the longer its duration, and the more sensitive its price will be to changes in market yields. The instrument’s value is the sum of cash flows received (interest payments and principal payments), discounted at the current rate demanded by investors for that instrument until its maturity.”

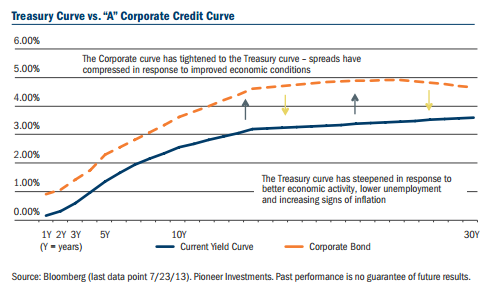

While duration can be a painful harbinger of the possibility of principal loss in a rising yield environment, not all duration is bad. There is spread duration, the calculation of the amount of spread associated with a debt instrument’s underlying duration. The more spread (and therefore the higher the spread duration), the better. Indeed, spread duration has the ability not only to help cushion the loss when rates are climbing, but provide strong and positive excess returns in a rising yield-curve and interest-rate environment. This is because “top-down” spread compression, which is often associated with an improving economy and therefore decreasing credit risk, can more than offset spread compression from the “bottom-up” (the result of higher yields demanded by investors in a rising rate environment). This is illustrated in the graph below where we are looking at the current single “A” corporate credit curve relative to the underlying Treasury curve.

Fixed Income Sectors: Running to Short Duration for Cover

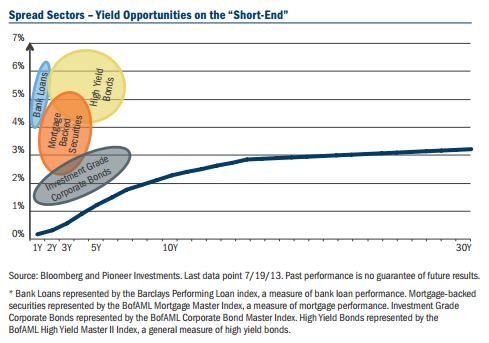

The math of spread duration and compression is not lost on bond managers. Investors in recent months have increasingly shifted exposure away from the long-end of the curve towards the short-end of the curve. This has led to dramatic spread and yield compression in the 0- to 5-year part of the high-grade corporate curve and has been largely responsible for the tremendous interest in high yield bonds (average duration of 4.2 years), bank loans (.25 years), non-agency mortgages (2-3 years) and generally anything that “floats” or adjusts to interest rates.*

But will this “rush” toward low duration end in tears as more and more investors abandon the long end of the curve, crowd into the short end, and ultimately drive spreads to levels that no longer even remotely compensate for credit risk or the risk of rising interest rates?

The Shot Across the Bow – Test of the “Safe Haven” Hypothesis

Treasuries reached their low point in terms of yield in 2013 on May 1st as a combination of mixed economic data, sequestration concerns and worries about a looming slowdown in China drove many investors to add duration to their portfolios. The beginning of the fixed income sell-off a few days later was due to much stronger-than-expected U.S. payrolls and manufacturing data. But the true shift in investor perception occurred in June 2013 as Fed Chairman Ben Bernanke revealed details on the likely timing of QE’s withdrawal. This crystalized for many investors that the Zero Interest Rate Policy (ZIRP) era was coming to an end.

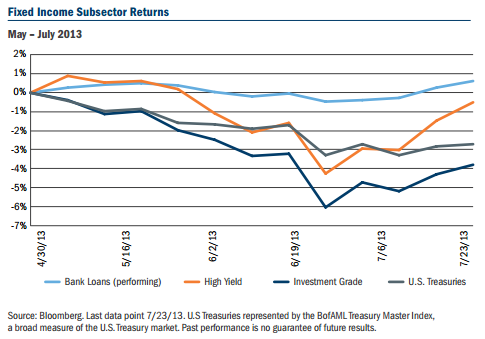

Over the following weeks, virtually all fixed income sectors sold off as investors pulled their money. While Treasuries and Agency Mortgages were the worst performing asset classes in June, investment grade corporates, high yield, emerging market bonds and even bank loans suffered as investors appeared to indiscriminately reduce exposure. Since June 25, 2013 many investors have moved back into spread-centric fixed income asset classes as yields became attractive and concerns about premature monetary tightening diminished. Below is a graph that depicts the sell-off and then recovery of many of the fixed income subsectors.

The question is – what was the lesson learned? Are investors over exposed to fixed income?

Or, given the strong recovery in high yield and the relatively benign loss in bank loans, do they just have too much exposure to the wrong sectors? In the next section, we examine each of the fixed income subsectors that have (in the past) been “safe havens” to investors in a rising rate environment, and ask the question: are they still “safe?”

Short Duration Investment-Grade Corporates Bonds: Is there anything left?

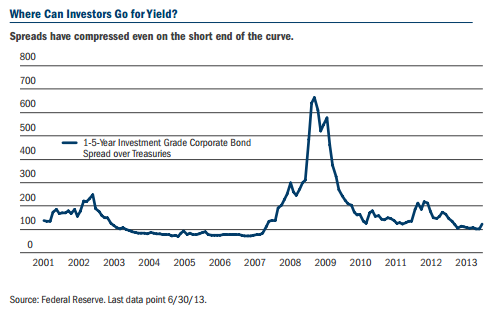

The investment-grade corporate credit market has been one of the primary beneficiaries of the search for yield in the short duration space. Spreads have dramatically compressed since 2009.

Interestingly, the area that we believe has provided some of the best risk/reward in recent months – bank and finance paper – has been trading on top of industrial and utility subsectors after having traded wide for the last four years (the fallout of investor angst after the near-collapse of the financial system). However, the narrowing of bank and finance spreads relative to the rest of the market is indicative to us of two things: 1) the growing realization that regulatory restrictions on financial entities and the unwinding of financial leverage has improved their credit-worthiness; and, 2) a growing concern over the resurgence of Leveraged Buyouts (LBOs) in the non-bank and finance sectors. At this stage, due to the growing event risk and limited spread, we think investors have to be cautious in this area of the credit universe.

High Yield: A “crowded” trade?

Pundits have been arguing that high yield is overbought because: 1) the call-constrained nature of the market will make it difficult to earn anything more than a coupon return; 2) the artificially low default environment – a consequence of ZIRP – will increase quickly once interest rates rise; and, 3) spreads are nearing their lows of the last era of economic reflation (2003-2007), and, therefore, cannot protect investors much in a rising rate environment.

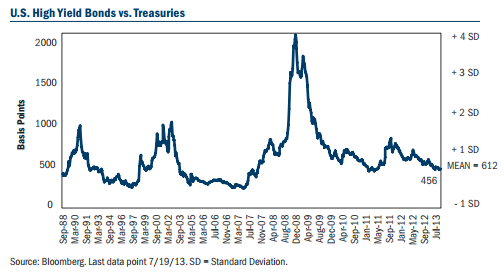

These observations have some validity and the sell-off in high yield in June certainly appeared to provide a proof statement to these claims. However, the quick “snap-back” in the high yield market suggested to us that investors may be focusing on the more positive aspects of this sub asset class. We would suggest that looking at “the market” as an aggregated whole often misses the trees for the forest. While 50% of the high yield market is call constrained, 50% is not, and can, therefore, experience spread compression. Spreads are also quite a bit higher than their lows of 2007. Below is a chart of the spread to Treasury ratio of the high yield market over time. As you can see, with the recent back-up in spreads and yields, spreads currently are just below average.

We think it likely that – despite the eventual removal of QE – the low interest rate environment will be maintained for some time to come. This should sustain a low default environment. Finally, the “carry” on high yield over the next 18-24 months – even if we don’t see any spread compression – could provide a possible 9-12% return, relative to a possible 4-5% return on 10-year Treasuries (assuming no shift in the yield curve). Thus, the potential return differential is substantial.

Ultimately, the high yield asset class will struggle when, after a period of rate increases, the economy softens and heads towards a recession. But given the likely continued muted default experience, we believe spreads do currently compensate investors for the added risk of this asset class.

The math: 460 basis points [1% = 100 basis points (bp)] of spread – (150bp of defaults x .30% historical recovery) = 4.15% excess return over Treasuries.

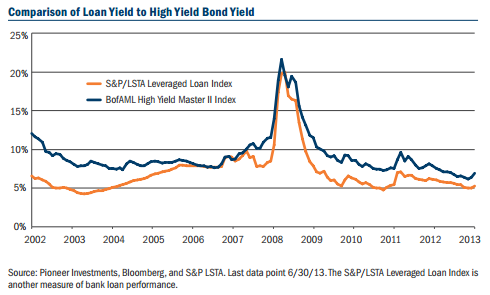

Bank Loans: Paying too much for interest rate protection?

If you don’t believe interest rates are going to rise anytime soon, why consider an investment in floating rate securities? The question is reasonable but misses the point. These securities seek to adjust their yield to a level above current interest rates. The floating rate feature of these securities is the cost of protection – essentially the price of insurance if investors are wrong on the timing and interest rates move higher sooner than expected. This was clearly on investors’ minds in the May-June 2013 sell-off as bank loans were the best performing asset class in the fixed income universe. Investors have enjoyed a reasonable yield from floating rate securities and, on average, an up-in-quality investment relative to a straight high yield bond due to the secured nature of the instrument. Of course, past performance is no indication of future results.

The trade-off between bank loans and straight high yield bonds are related to recovery value (historically 70% vs. 30%) vs. yield differential.

As the yield differential narrows, bank loans can become an increasingly more attractive asset class (all other things being equal).

Non-Agency Mortgages: A Bet on Housing?

Non-agency mortgage-backed securities, formerly known as “subprime” instruments, have been a strong source of return since their meltdown in 2008/2009. Contributing factors include: shrinking supply (when was the last time you saw a new subprime mortgage issued?), reflating house prices, and the hunt for protection from the possibility of rising interest rates (as these are largely floating rate securities).

We broadly think about the opportunity set for these securities in three buckets (based on 6/30/13 yields from Bloomberg):

- Highest quality with approximately 1-3%yield and a 1-to 4-year duration. This section of the market has tremendous subordination (meaning there are many layers of potential cushion).

- Mid-level quality with 3-4%yield, balanced subordination and delinquency.

- Lowest quality, 5+% yield, trading in the $70-$90 range in which principal return maybe in question, but for which we believe the yield (we think in terms of loss-adjusted yield) can adequately compensate an investor for the risk.

We continue to believe that non-agency mortgages can provide decent return potential but the opportunity for dramatic out-performance is limited.

Thinking Outside the Box

While many of the historically sought “safe-haven” fixed income sectors in a rising rate environment may still be capable of providing some degree of cover (due to spread cushions), the degree of protection has diminished. As we pointed out in our very first installment of this series, all fixed income has been drawn into the black hole of zero interest rates. As a result, fixed income investors may find themselves on an increasingly narrow path.

On one edge of the path they face potentially steep losses from duration. On the other side of the path, given how low yields are and, in many cases, how high bond prices have become, they face the threat of significant losses when the credit cycle finally tips over. This typically would not occur until after rates have begun to rise. However, we believe that given current yield and spread levels – which have “front-run” the economic recovery cycle – it does not pay to take on too much idiosyncratic credit risk. Nor does reaching for the riskier parts of the credit market or towards levered strategies (that promise outsized fixed income returns), make sense.

Ultimately, we believe investors should seek out money managers that are cognizant of the twin risks of duration and credit, are mindful that the greater, more looming risk is duration, but who can adjust their portfolios over the next several years to this shifting landscape.We suggest that investors have their fixed income allocation in nimble strategies that are not tied to a specific “box” – an index or a narrow asset class. The next several years will require managers and strategies that have the ability and the mandate to rapidly adjust exposure, from credit back into duration-centric investments, across geographic boundaries and towards sectors that might provide (if only fleetingly) opportunities to outperform in the coming years.

In coming papers, we will explore the topic of “unconstrained” investing in fixed income more fully.

© Pioneer Investments