Float Research: Is Fed Starting to Lose Control of Bond Market?

Bond yields hit two-year highs as investors pull an additional $19.7 billion from bond funds in August. Read this investor insight by Minyi Chen, CFA, Chief Operating Officer of TrimTabs Investment Research and Portfolio Manager of AdvisorShares TrimTabs Float Shrink ETF (NYSE Arca: TTFS) to learn what concerns may arise in the coming months if this trend continues.

-Short-Term Outlook for Stock Market Brightens, but Intermediate-Term Outlook Darkens Slightly. Inflows into Leveraged Short ETFs Accelerate to Four-Week High.

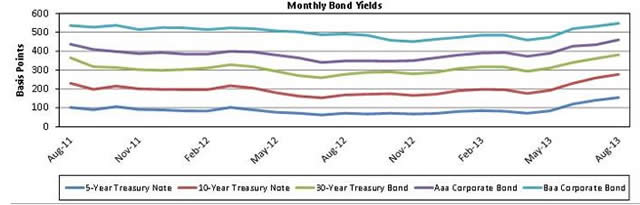

The stock market finally seems to be taking note of the ugly action in the bond market. Bond yields have increased for the past four months, and they hit two-year highs in the past week. For example, the yield on the 10-year Treasury note reached 2.83% on Friday, up 107 bps from 1.76% in April; and the yield on Baa corporate bonds sits at 5.47%, up 88 bps from 4.59% in April.

Past performance is not indicative of future results.

Despite soothing words from various Fed officials, fund investors are dumping bonds at a record pace. Bond mutual funds and exchange-traded funds have redeemed a staggering $103.5 billion (2.7% of assets) since the start of June. The outflow of $69.1 billion in June was the highest ever, and the outflow of $19.7 billion so far in August is already the fourth-highest ever. If the Fed starts tapering and investors keep selling bonds, how much will the government and corporate America eventually have to pay to borrow?

We are concerned that the Fed is starting to lose control of the bond market, which is not good news for the stock market or the highly leveraged U.S. economy. Higher bond yields make stocks—particularly dividend paying stocks—relatively less attractive. They are also a big headwind to a highly leveraged economy dependent on low interest rates and easy credit (total credit in the U.S. is equal to 345% of GDP). Of course, the Fed could decide not to “taper” or even expand its money printing, but then it would risk further distorting the Treasury market and inflating even bigger asset bubbles. Unfortunately, it is a lot easier to start or expand money printing than it is to diminish or stop it.

ETF flows turned much less negative from a contrarian perspective in the past week, which suggests stock prices will stabilize or even rebound over the near term. Inflows into leveraged short ETFs accelerated to a four-week high of 3.2% of assets in the past week, while leveraged long ETFs redeemed 0.9% of assets. Another encouraging sign is that investors are losing their affection for U.S. equities. U.S. equity ETFs issued only $6.4 billion (0.8% of assets) in the month ended August 15, down from a 4½-year peak of $35.6 billion (4.2% of assets) in the month ended August 2. As we explain in this issue, far more money coming out of bonds seems to be flowing into savings vehicles—particularly bank savings accounts—than into equities.

On the supply front, corporate actions have turned less favorable. To be sure, companies are still net buyers of shares, but buying is outpacing selling by far less than it did earlier this year. Announced corporate buying (new cash takeovers + new stock buybacks) has exceeded new offerings by $16.6 billion so far in August. Also, an average of $2.3 billion daily in new stock buybacks was announced in earnings season, the lowest volume in a year. Fortunately for the bulls, new offerings should be seasonally slow for the next three weeks.

This communication is a publication of TrimTabs Asset Management. It should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. Information presented does not involve the rendering of personalized investment advice. Content should not be construed as an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein. Performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing performance returns. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Past performance may not be indicative of future results. Therefore, no investor should assume that the future performance of any specific investment or investment strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions, may materially alter the performance of an investor’s portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor’s portfolio.

© AdvisorShares