Excess Cash in the Technology Sector: A Source of Underappreciated Value

As analysts,we are constantly searching for opportunities to purchases hares of a business at a meaningful discount to our estimate of intrinsic value, or short shares of a business at a meaningful premium to our estimate of intrinsic value. While this premium or discount is often a function of our estimate of the value of the business’s future earnings power, it can also be the result of the current market price not properly reflecting the value of assets on a company’s balance sheet. In the technology sector, we own shares of several companies that have significant amounts of excess cash on their respective balance sheets. Because this excess cash has accumulated over a number of years and the timing within which it will be either returned to shareholders or reinvested in the business is uncertain, in many instances it seems that current market prices reflect a belief that this excess cash has little value. While we acknowledge that the precise amount of value that will ultimately be realized from this cash is uncertain, we believe its value can be reasonably estimated.

Overseas Profit and Overseas Cash

Asa result of both the global nature of their businesses and the nature of intellectual property and tax planning, many technology companies recognize a substantial portion of their profit outside of the United States. The profit is taxed by the country in which it is recognized immediately, but it is not taxed by the U.S. government until the cash is returned to the United States. Because many of the countries in which the profit is recognized have lower corporate tax rates than the U.S., corporations benefit in the short-term by paying less income tax. However, when this cash is returned to the U.S., it is taxed at roughly the difference between the 35% top U.S. corporate tax rate and the tax rate that was already applied in the country in which the profit was recognized. For example, if profit was taxed at a 10% rate in a foreign jurisdiction, an additional tax of roughly 25% would be owed to the U.S. government upon repatriation of the cash from the foreign jurisdiction to the U.S. Reluctant to pay this additional tax, many companies have elected to keep overseas cash in the foreign jurisdictions rather than repatriating the cash to the U.S. and paying the additional tax. Therefore, while overseas cash is listed at its full value on the balance sheet, only the amount net of the additional tax owed to the U.S. government would be available for dividends or share repurchases if that cash were to be repatriated.

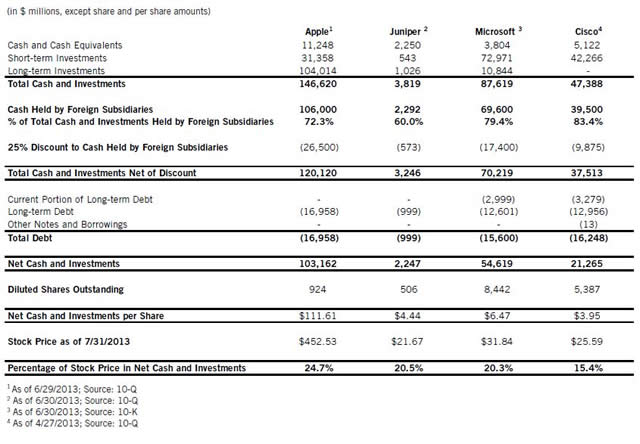

In2004,Congress passed a repatriation tax holiday that allowed companies to bring back profits earned in foreign jurisdictions at roughly a 5% incremental U.S. tax rate. According to the Internal Revenue Service, 843 companies repatriated a combined $312 billion as a result of that legislation. Critics of the 2004 legislation argue that it also provided an incentive for companies to stockpile cash in foreign subsidiaries in anticipation of future repatriation tax holidays instead of repatriating foreign profits on an ongoing basis. As a result, future repatriation tax holidays remain politically controversial. Exhibit A details the net cash positions of four of our technology holdings, Apple, Inc. (AAPL), Juniper Networks, Inc. (JNPR), Microsoft Corp. (MSFT), and Cisco Systems, Inc. (CSCO). In the interest of conservatism, a discount for a 25% repatriation tax is applied to cash held by foreign subsidiaries when calculating net cash for each company. A future repatriation tax holiday would clearly be beneficial to these companies, but net cash, even after adjusting for a 25% repatriation tax on cash held by foreign subsidiaries, represents between 15% and 25% of the current share prices. When we combine this balance sheet value with the value of the future earnings power of each business, we believe these four businesses represent attractive investment opportunities at current market prices.

Impact of the Current Interest Rate Environment

The current ultra-low interest rate environment impacts both the interest income that is earned on cash holdings and the cost of debt when companies elect to issue debt rather than repatriate cash held by foreign subsidiaries. In the current environment, cash earns very little interest income, and therefore some valuation methods would overlook the cash and mistakenly assume that it has no value. Ultra-low interest rates also allow companies to borrow inexpensively to access cash, as Apple

recently did, without repatriating cash held by foreign subsidiaries. This borrowing serves as a low-cost means of positioning the company to benefit from any future repatriation holiday while still having access to an ample supply of cash for reinvestment in the business as well as dividends and share repurchases.

Conclusion

With a long-term perspective, the fact that investors cannot know exactly how cash on the balance sheet will ultimately be utilized to create value for shareholders presents an opportunity for us to purchase shares of businesses possessing large amounts of excess cash at a discount to our estimates of intrinsic value. We have ideas about how some of this cash will be utilized overtime. Most importantly though, there are a variety of scenarios in which shareholders would be rewarded for recognizing the value of cash, even in a low interest rate environment, and possessing the patience to wait for that cash to be either returned to shareholders or invested in growing the earnings power and intrinsic value of the businesses.

Exhibit A

The views expressed are those of the research analyst as of August 2013, are subject to change, and may differ from the views of other research analysts, portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice.

© Diamond Hill Investments

© Diamond Hill Capital Management