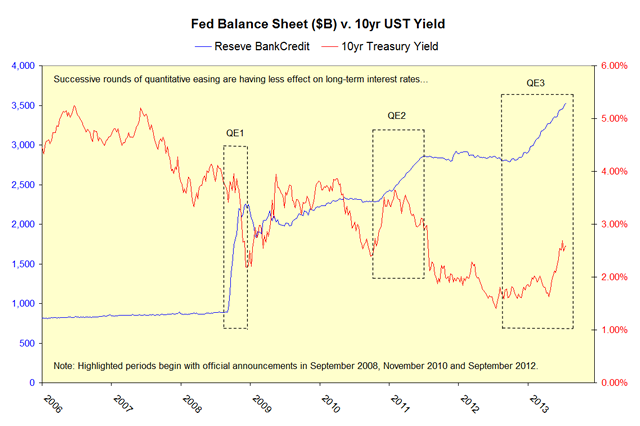

In September 2012, the FOMC announced a third round of quantitative easing intended to reduce long-term interest rates. Since then, the New York Fed has purchased about $700 billion of mortgage-backed securities. But a funny thing happened on the way to lower interest rates. During the “QE3” period, the benchmark 10-year US Treasury yield has risen by a full percentage point. The targeted 30-year mortgage rate has also risen by about 100bps.

The chart below compares the size of the Fed’s balance sheet (left scale, blue) with the yield on 10-year Treasury securities (right scale, red). Balance-sheet-growth periods, beginning with QE announcement dates, are boxed for close examination. Here we see that successive rounds of quantitative easing have produced less and less of the desired effect on long-term yields.

This suggests that, despite its massive size and influence, the Fed is not the marginal buyer of long-dated bonds.

Alternatively, one could argue that the market looks ahead, discounting the full effect of quantitative easing prior to announcement. But QE3 was open-ended in nature with no pre-defined size or scope. And bond yields accelerated upward in December 2012 when monthly purchases were increased from $40 billion to $85 billion.

The stated purpose of quantitative easing is to reduce long-term interest rates when short-term interest rates are near the zero bound. By this measure, the policy has had mixed results since inception in 2008. While quantitative easing is undoubtedly influencing the market economy, the mechanism if far from clear.

© Charter Trust Company