Reason 1: Current Valuations

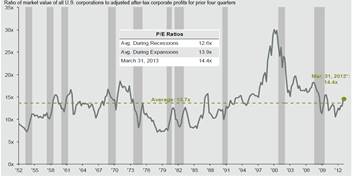

Wall Street is currently calling the stock market cheap or fairly valued because we are trading at 14 times earnings based on 12-month trailing P/E, which is near historical averages (Chart 1).

Chart 1: Lagged P/E Ratio – All U.S. Corporations

Source: BEA, Federal Reserve Board, Wilshire Associates, J.P. Morgan Asset Management.

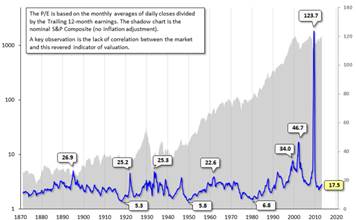

The issue with using this simplified metric stems from the fact that one-year trailing earnings can be volatile, causing the P/E ratio to appear unusually high or low at various periods when earnings (E), are above or below their historical norm. Before dissecting the current 12-month trailing earnings metric and assessing earnings relative to historical levels, let’s first examine just how misleading this measure has been in recent years.

During the spring of 2009 (recall the market low from the Financial Crisis was March 2009), the P/E level was as high as 123.71, indicating a level of extreme market overvaluation. Yet, this was the best time to be purchasing equity securities ahead of an impending 130%2 total return for the S&P 500. Furthermore, in early 2007 – just months before the financial crisis – the P/E ratio reached a modest level of 17. As we can see from Chart 2, this measure of market valuation has been very misleading during times of great importance.

Chart 2: S&P Composite: 1871-Present

Nominal Price with the Trailing 12-Month P/E Ratio

Source: Is the Stock Market Cheap, Doug Short

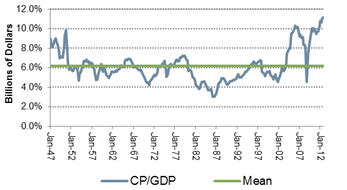

Next, let’s address whether the current level of the P/E ratio being touted by Wall Street could be misleading us today. In order to assess this, I have constructed a chart of the historical level of corporate profit margins relative to GDP, Chart 3. We can see that not only are we currently above historical norms for corporate profit margins, but we are roughly 70% above the historical average. With earnings at such extreme highs relative to the historical average, one can’t help but think that the 12-month trailing P/E is being distorted to reflect abnormally high profit margins.

Chart 3: Corporate Profits as a Percentage of GDP

Source: U.S. Bureau of Economic Analysis, Mesirow Financial

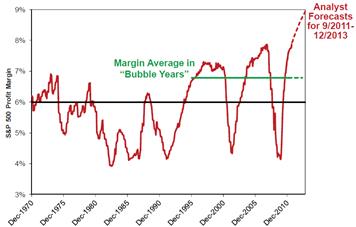

The global investment firm, GMO, is known for studying market bubbles and historic market trends, including this recent spike in profit margins. James Monteir of GMO recently wrote a piece on the subject, summing up their argument as: “Whilst we at GMO fret over evidence of the strained nature of profit margins, the ever bullish Wall Street analysts expect profit margins to continue to rise!.. In our search for evidence of a structural break, this simple-minded extrapolation gives us some comfort because the Wall Street consensus has a pretty good record of being completely and utterly wrong.3”

In the same piece, Montier also includes a chart of historical profit margins and includes the “margin average in bubble years.” Notice the current position of this metric in relation to the bubble averages; more importantly, notice the Wall Street forecasts in relation to this level (Chart 4).

Chart 4: S&P 500 Return on Sales

Source: GMO

If we compare Chart 3 alongside the one from GMO, we can conclude that we have reached a level where corporate profit margins are stretched beyond their normal averages, not just in isolation, but as a percentage of the overall economy as well. Essentially, this indicates that the “standard” P/E ratio is misleading investors based on the recent abnormal earnings spike.

The Shiller P/E is a metric that attempts to eliminate these distortions in short-term earnings and account for these types of fluctuations in the business cycle by using an average of the prior 10 years of trailing earnings (inflation adjusted)4. It can be used as a market valuation predictor for 10-year forward real returns. By smoothing out earnings over a longer time horizon, it presents a more stable measure from which to base valuations. Using this metric, pictured in Chart 5, we are currently sitting at a level of 23.6, which is above the long-term mean valuation by roughly 40%. By using a more normalized value for our earnings measure, the Shiller P/E is implying that the market has reached over-valuation.

Chart 5: Schiller P/E Historical Value

Source: Robert Schiller, Mesirow Financial

If we compare the above chart to the commonly used P/E historically, when the standard P/E was indicating extreme overvaluation at the market lows in 2009, the Shiller P/E was indicating strong future real returns as it was positioned below its long-term average. In addition, you may recall that in early 2007, just months before the market peak preceding the financial crisis, the P/E level was at a modest 175; however, the Shiller P/E was at 26.2, which was 61% above its then historical average.

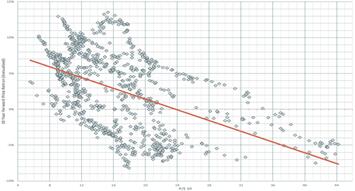

It is important, however, to note that the Shiller P/E is only effective as an indicator of market valuation, and should not be used as any sort of market timing tool. It has, however, been a good indicator of what to expect as 10-year, forward- average real returns fall nearly monotonically as the starting Shiller P/E increases (see Chart 6)6.

Chart 6: 10-Year Forward S&P 500 Real Price Return (Annualized) by P/E Starting Valuations 1926-2013

Source: Bloomberg, Mesirow Financial

After compiling these data points into deciles and viewing what each Shiller P/E level has meant for 10-year, forward-looking real returns, things look a lot less rosy for the next 10 years than the trailing 12 month P/E would indicate (Chart 7).

Chart 7: Results for S&P 500 From Different Starting Shiller P/Es 1926-2012

Now, the Shiller P/E certainly isn’t without flaws, but it is hard to argue against the popular P/E alternative when viewing the data. So, before you sour on the future returns expectations put forth by the Shiller P/E, recall that roughly four years ago during the March 2009 market lows, the Shiller P/E was at 13.37 (the standard P/E measure was in the triple-digits8). Again, looking at Chart 7, at that time the metric was indicating an average future 10-year annualized real return of 8%. With an annualized four-year, real price return of 16.8% on the S&P 500 since that time, does a more-muted return pattern in the years to follow seem all that unreasonable?

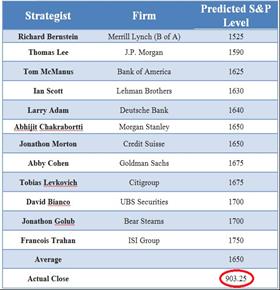

As a final point before moving onto the next section, keep in mind the 12 month trailing P/E failed in times of great importance. This is partially due to Wall Street analysts extrapolating recent earnings into the future. In December of 2007, the Shiller P/E indicated that the market was extremely overvalued relative to its historical average, indicating that equity market participants should either be exercising caution or lowering their forward-looking return expectations. Yet, what was Wall Street’s “best and brightest” predicting for the S&P the following year based on their ever so dependable trailing 12 month P/E metric? See Chart 8 for a grim reminder – how soon we forget!

Chart 8: Barron’s Round Table Results, Dec. 2007

Source: Bloomberg, Butler|Philbrick & Associates

Reason 2: Interest Rate Levels

Since rates of return that investors need from investments are directly tied to the risk-free rate that they can earn from government securities, interest rates act on investments like gravity acts on matter. As rates rise, investments must adjust downward, to a level that brings their expected rates of return into line – the same would be at work in the opposite direction. To quote Warren Buffett: “In the case of equities or real estate or farms or whatever, other very important variables are almost always at work, and that means that the effect of interest rate changes is usually obscured. Nonetheless, the effect – like the invisible pull of gravity – is constantly there.9”

Recently, there have been several arguments among investors that if the Fed were to taper off its asset purchasing program and interest rates were to rise, their rising levels would not affect equity markets. The reasoning behind this thinking is if the Fed were to stop their manipulation of interest rates (currently being enacted by their asset purchasing), it would have done so due to the improving economy. Therefore, improving unemployment, brought about by economic activity (GDP), would boost the returns of risk assets, in spite of rising interest rate levels.

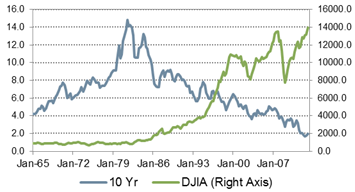

Far be it from me to fight this logic. On its face, it seems reasonable. Yet, I would like to point our attention to the last time we experienced strong GDP growth in the face of rising interest rates, January 1, 1965 with the Dow Jones Industrial Average (DJIA) standing at 893.7 and interest rates at around 4%. In the subsequent period from 1965-1981, interest rates increased to more than15%, and the DJIA ended 1981 at 875. Ponder that for a second: start of 1965 DJIA at 893.7, end of 1981 DJIA at 875 (see Chart 8).

Chart 8: 10-Year Treasury Yield Compared to DJIA

Source: Board of Governors of the Federal Reserve, Mesirow Financial

The point here, and in the context of where we are today, is that from 1965-1981, the GDP of the U.S. soared, increasing by 370%. Or, looking at it another way, the sales of the Fortune 500 companies more than sextupled, yet the DJIA actually remained relatively flat (the S&P went from 86.6 to just 122.5 in the same timeframe).

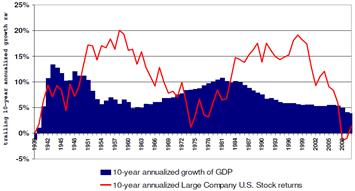

In the years to follow, we’ve again seen growth in GDP reach roughly 380%, but the DJIA has rose from 875 to 13,104 (the S&P 500 has increased from 122.5 to 1,426). This addresses another point for those that continue to link GDP with stock market performance. The lack in correlation between the two in the data that I have presented can be seen in the chart below. Two time periods experienced roughly the same growth in GDP, yet one saw relatively flat market performance, and the other experienced extreme market gains. The difference between the periods was the behavior of inflation, and its influence on interest rates. I am not saying that we will see the kind of inflation that we saw before Paul Volcker’s tenure at the Fed, however, we do know two things for certain: (1) interest rates will most certainly rise from here at some point, and (2) we have pumped an unprecedented amount of liquidity into the system by way of the Fed’s Quantitative Easing program and really have no way of determining how inflation will react, and what that could mean for how long interest rates rise.

Chart 9: Trailing 10-year Annualized Growth Rates

Source: U.S. Bureau of Economic Analysis, Mesirow Financial

If you were to expect a normalized return for the markets, you need two key events: (1) interest rates must fall further, and (2) corporate profits as a percentage of GDP must continue to hold at historical highs. I think the consensus on point one rules that out, and point two was addressed earlier in Charts 3 and 4.

In summary, as of today we are facing fairly high valuations as measured by the Shiller P/E, corporate profits are at all-time highs, and interest rates – which pull asset values downward as they rise – are at all-time lows. The starting position for all three measures coupled with a 130% run up in equity prices indicates that we should be lowering our equity expectations for the long-term. I underline and bold those words because investors often get the “here and now” confused with a long-term investment horizon. We can certainly continue to see the S&P 500 continue to reach new highs from here; however, a prolonged period of such market behavior is not supported by the fundamentals.

You should remain skeptical when reading Wall Street estimates, as they once again seem to be up to their old tricks of extrapol-ating recent results into the future. I think that the performance of the popular 12-month trailing P/E in times of great importance (i.e. the period before and after the financial crisis), and the past predictions of Wall Street analysts (remember 2007) speak for themselves.

Reason: Current Starting Prices

After the case has been made that the expectations for equity returns should be somewhat subdued, it might be surprising that when it is all said and done, equities appear to be your best option relative to the fixed income alternative. While equities are currently not set-up for “normalized returns,” which is often classified as the 7-8% long-term real annualized market return, something more muted than that may not seem so negative when we break down the argument for expected future returns in the fixed income markets.

The yields on fixed income securities have declined markedly and in many cases are the lowest we have ever seen in our nation’s history. This is partially due to the interest rate manipulation by the Fed, and has partially been driven by investors that have remained spooked by the wild ride equities have taken over the past decade or so. Many people have sought the “safety” of fixed income assets and bid down yields in the meantime.

In discussing the “safety” of assets, let’s look back in time for an investment history lesson that many of you might remember. Back in the 1960s there was a popular investment approach known as the “Nifty Fifty,” in which investors invested in what was deemed to be the best and fastest growing companies in America. Many of them were in fact great companies (Coca-Cola, General Electric, McDonald’s, etc.); however, they were not great performers for investors. By the early 1970s their P/E’s went from 80 or 90 to roughly 8 or 9, and those who had invested in these “top quality” companies had lost 90% of their money10.

Shortly thereafter, towards the end of the 1970s, some investors had begun to dabble in “junk bonds.” These were high-yielding, fixed income securities that – as their name reflects – were considered highly risky and unsafe for investment. Yet, if you had placed $1 into a high yield bond index in 1979 you would have more than $23 today, and would have never been in the red. In other words, you can invest in the best companies in America and lose money, and invest in the worst companies in America and have your investment make money with relatively no downside experience11.

The point here is that no asset, no matter how “safe” the perception, is unable to be bid up to the point where it is no longer a good investment. The same goes in the opposite direction. Today we are looking at this scenario in the fixed income markets. If we expect inflation to be 2%, then yields on the 10-year Treasury of 1.87% mean that you are receiving a nominal negative real return to own Treasuries. This is important because the 10-year Treasury yield has been an excellent indicator of forward-looking, 10-year returns for fixed income assets (see chart 10). The chart below is a very telling chart about what should be expected for future fixed income returns.

Chart 10: Starting Bond Yield Versus Forward Return

10-Year U.S. Treasury Yield vs. Forward 10-Year Returns on Bond Indices

Source: Mesirow Financial

Earlier, we mentioned the affect that interest rates have on the value of assets. This influence is not as easily recognized with equity securities, but with fixed income securities the relationship is easily observable. As interest rates rise, the price of bonds will fall – period. Given current yields, the expected impending rise of interest rates, and the potential loss in purchasing power represented by nominal returns given inflation, fixed income securities offer a poor outlook for investors. Lastly, and the point investors have failed to realize given asset flows over the past few years12, all other things being equal, as illustrated above in our “Nifty Fifty” example, it is the price of an asset that determines its risk, and right now fixed income securities are priced poorly for investors to expect any possibility of good future returns.

In closing, the theme of this piece is quite clear: Lower Your Expectations. The point though, should not be missed: knowing how an asset is priced and properly assessing the current environment is the best way to set expectations for future returns. While equities are not priced particularly well and the current environment does not seem to bode well for future long-term expected real returns, we think they are currently a better choice for investors relative to the alternative. Right now, any meaningful shifts in one direction or the other could be setting the investor up for additional disappointment. At this stage in the game, equities look to offer better prospects in the long-term. However, the time is not right to abandon your long-term investment plan in the face of the positive market headlines and lofty predictions emanating from Wall Street.

This report has been prepared for informational purposed only. It is based on information generally available to the public from sources believed to be reliable. No representation is made that information is accurate or complete. Past performance is not indicative of future results. Additional information is available upon request. Mesirow Financial refers to Mesirow Financial Holdings, Inc. and its divisions, subsidiaries and affiliates. The Mesirow Financial name and logo are registered service marks of Mesirow Financial Holdings, Inc. © 2013, Mesirow Financial Holdings, Inc. All rights reserved. Some information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. Any opinions expressed are subject to change without notice. Advisory Fees are described in Mesirow Financial Investment Management, Inc.’s Form ADV Part 2. Mesirow Financial does not provide legal or tax advice. Advisory services offered through Mesirow Financial Investment Management, Inc. an SEC registered investment advisor. Securities offered by Mesirow Financial, Inc. member FINRA, NYSE and SIPC.

1 Data from Standard & Poor’s

2 IBID

3 What Goes Up Must Come Down!, James Montier (GMO) March 2012

4 The idea was originally motivated by the ideas of Benjamin Graham and David Dodd in their classic book, Security Analysis. It has since been popularized by Professor Robert Shiller of Yale University who used it in his book Irrational Exuberance as a time warning of poor stock returns to follow in the coming years just before the 2000 stock market crash.

5 Data from Robert Shiller

6 An Old Friend: The Stock Market’s Shiller P/E, Clifford Asness, Ph.D. November, 2012

7 Data from Robert Shiller

8 Data from Standard & Poor’s

9Mr. Buffett on the Stock Market, Fortune Magazine, November 22, 1999. Warren Buffett and Carol Loomis

10Ditto, Howard Marks, January 7, 2013

11 IBID

12 Data from the Investment Company Institute, which tracks mutual fund behavior, suggests that investors have missed the gains in the equity markets due to strong asset flows into fixed income mutual funds.

© Mesirow Financial Wealth Management