“…an unfortunate consequence of the most recent naïve interventions is that capital preservation in the long run and capital preservation in the short run have been made mutually exclusive.”

- Dylan Grice, Edelweiss Journal Issue 13

Dear Client,

To begin, let us state that we are tired of writing about macroeconomic issues. We suspect you are tired of reading about them. We would like nothing more than to send out a quarterly letter full of updates on the companies we own and the rationale for individual buy and sell decisions. Nevertheless, we must address the market action following Federal Reserve Chairman Ben Bernanke’s May 22nd testimony before Congress, where he merely floated the idea of “tapering” the Fed’s quantitative easing efforts. Subsequently, almost every global asset class fell in value. We believe this market reaction is just a taste of what is possible and justifies a continued conservative investment posture that recognizes the ephemeral nature of current valuations. Thus, brace yourself for a discussion of financial repression, perfect asset price correlation, and tail risk1.

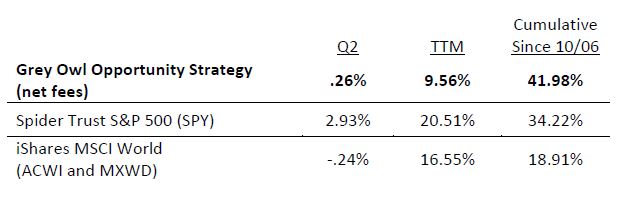

Before moving on, here is the standard performance table for Grey Owl Opportunity Strategy as of June 30, 20132:

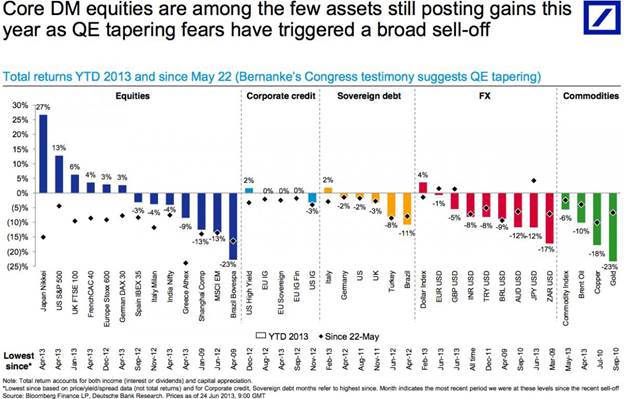

In congressional testimony on May 22nd, Federal Reserve Chairman Ben Bernanke indicated that the central bank COULD begin to taper purchases of Treasuries and mortgage backed securities as early as September of 2013. For the next month, almost every global asset class fell in value, some dramatically. The following chart from Deutsche Bank shows how widespread the losses were.

What happened? Aren’t “safe” Treasury securities supposed to go up when “risky” equity securities go down? Isn’t that the basic principle behind asset allocation and modern portfolio theory? If the market’s reaction to the possibility of a slowdown in Fed bond buying at some point in the future is an indication, it would seem that some long-held investment axioms are now up for debate by a broader set of folks than just us (and a small number of others we often reference in these letters).

Every single asset class is levitating on the back of more than four years of unconventional Federal Reserve policy. The latest GMO3 quarterly letter provides a detailed exposition of this and is well worth reading (and rereading). We grossly simplify the premise in the charts below.

In the first chart, we plot three asset classes (cash, bonds, and stocks) on a two-axis grid. The y- axis is return and the x-axis is risk. Notice that cash is very low risk, and thus offers a requisite low return. The risk goes up a bit for bonds and with this the return. Stocks go a step further: even more risk and even more return. Each offers a positive real (i.e. adjusted for inflation) return, with incrementally higher return coinciding with incrementally higher risk. Chart 1 shows cash, bonds, and stocks in an equilibrium position.

From time-to-time however, this equilibrium is disturbed. Sometimes the equilibrium breaks down among the highest-level asset classes (cash, bonds, and stocks). More often, breakdowns occur between sectors within asset classes. The example most investors are familiar with is the technology, media, and telecom (TMT) bubble of the late 1990s. Anything beginning with an “e” or ending with a “dot-com” in its name traded at price-to-earnings ratios above 100, while REITs and “value stocks” were unloved and thus cheap.4

Today, the entire universe is in disequilibrium because Chairman Bernanke has his thumb on the scale. We depict this in Chart 2. The various Fed interventions have served to increase asset prices across the spectrum (and thereby decrease their future returns). PIMCO’s Mohamed El- Erian has referred to this as a “stable disequilibrium.” But, as we saw subsequent to May 22nd, the disequilibrium is only stable so long as the Chairman’s thumbholds out.

Putting specific numbers to this phenomenon, David Rosenberg of Gluskin Sheff estimates that“the Fed’s actions, both directly and indirectly, have added as many as 500 points to the S&P 500 this cycle; have depressed 10-year bond yields by more than 300 basis points; and have rendered high-yield spreads at least 60 basis points ‘richer’5 than they would be if they were trading on credit risk fundamentals on their own.” The critical implication of this is that we are left with only two potential outcomes:

- Markets will continue their positive returns, but the annualized returns for the next 7-10 years will be much lower than those to which we have become accustomed. Recently strong investment results have “pulled forward” future returns and it will take 7-10 years for assets to “grow” into their current valuations.

- Markets will experience a violent price reversal in the next few years that will correct the Fed-induced overvaluation, setting up asset classes for future returns more consistent with historic averages (and investors’ expectations).

Given those possibilities, chart 2 gets at the heart of the current investment conundrum. Cash and lower-risk bonds are both likely to provide a negative real return over a 7-10 year investment horizon. In order to get a positive real return from today’s asset price levels, investors probably have to reach for riskier debt securities or equities. Based on this premise, many professionals and commentators recommend overweighting equities. Unfortunately, the decision is not that simple. This will only work if the Fed’s financial repression continues for another 7-10 years and any meaningful asset price correction is avoided. If the Fed loses its willpower, or the market loses its faith in the Fed, scenario 2 described above is more likely. If that occurs, the right investment choice will have been to hold cash, accept slightly negative current real returns, and avoid a major asset price correction. Should scenario 2 develop, a correction of 30-50% is well within the realm of possibility.

We have absolutely no idea how long the Fed will continue with its current policy and/or how long the market will retain its faith in the Fed. No one does. Given their rapid backpedaling after the May 22nd induced correction, our belief is reaffirmed that the current Fed has very low tolerance for market instability and is thus inclined to continue on the current path. But politics are volatile too so this can change very quickly. In addition, the market’s faith in the Fed is somewhat dependent on what is going on in the rest of the world (e.g. Japan, Europe, and China). There are just too many moving parts to predict this with any degree of accuracy.

Our choice continues to be to construct portfolios that will perform well should either scenario 1 or scenario 2 develop. We detail what this means for equity and fixed income portfolios below, as well as the role we believe gold plays as a hedge given this unprecedented and unstable environment.

Equities

As asset markets in general have been driven more and more by the Federal Reserve’s actions, our general philosophy has been to hold between 20-30% cash in equity accounts. Given the probability that the current Fed policy will continue for at least the short-term, this feels like the right “barbell” structure to deal with the potential of either scenario 1 or scenario 2 developing. Something closer to scenario 1 is more likely, but scenario 2 is very possible and more so as each day passes. In addition, we have weighted our portfolio to “high-quality” companies (i.e. those with consistent earnings growth, lower leverage, and consistently higher underlying business returns). Like insurance, both of these portfolio decisions have costs – costs we to continue to accept given the extremely damaging impact should scenario 2 develop (as evidenced by the reaction to the Chairman’s May 22nd comments).

Cash is a drag and high-quality securities have underperformed low-quality securities (see Chart 3 for the recent comparative performance) for multiple reasons. Perhaps the most important one is that debt has been so inexpensive. This makes levered companies more profitable, but it also enables essentially terminal companies to gain a second life. In addition, the continued Federal deficit spending for transfer payments6 has sustained consumer spending and forestalled any modest recession that underlying economic fundamentals would suggest is likely. Low quality companies are typically more economically sensitive. Without even a modest recession, it is hard to see “who is swimming without their bathing suit.”7 None of this is sustainable, but we can’t predict exactly when it will end. Either way, we want to be firmly in our chairs when the music stops.

Chart3

SPXQRLUT is the S&P 500 low quality index (the lowest quality quintile of the S&P 500). SPXQRUT is the S&P 500 high quality index (the highest quality quintile of the S&P 500). The graphic shows that for the first six months of the year, low quality outperformed high quality by almost 5%.

Fixed Income

“Duration” is an investment term that defines how sensitive a security or portfolio is to changes in interest rates. The higher the duration, the greater the impact a change in interest rates will have on the portfolio. If interest rates go up, a portfolio with a high duration will lose more value than one with a low duration.

In response to the 2007-2009 financial crisis the Federal Reserve has taken step after step to lower and then keep low interest rates all along the yield curve (that is short, medium, and long-term rates). Absent the Fed’s intervention, interest rates would find a (different) natural level – presumably higher. Thus, for the past few years, we have structured our portfolio to have a low duration. In addition to low on an absolute basis, the duration has also been relatively low compared to bond indexes such as the Barclays Aggregate Bond Index. So, when Treasury bonds have rallied as interest rates have gone down, our portfolio has been at a disadvantage to the various broad bond market indices that are heavily weighted to Treasury bonds. However, when rates have gone up, our portfolio has been protected from that specific risk.

This does not mean our portfolios have no interest rate risk. The duration has not been and is not zero. In addition, the portfolios have taken on other forms of risk; most specifically currency risk and very targeted credit risk. Some level of risk must be assumed in order to earn a return, but we believe that the compensation for currency and certain forms of credit risk has been adequate, while the compensation for significant interest rate risk has not.

Despite this longer-term, strategic view, we will still be opportunistic. As such, with interest rates spiking in June, we reallocated capital from credit sensitive securities in the middle of the duration range into slightly longer duration government securities. With GDP continuing to decelerate, CPI tame, and growing economic issues in both Japan and China we believe there is a high probability that Treasury rates move back towards 2% over the short-term. An additional factor working in our favor is the very wide (and atypical) spread between short-term rates and medium-term rates.

Gold

We own gold as a hedge against currency debasement and inflation. Based on analysis of historical data, Wainwright Economics has found that a mix of 15 percent gold and 85 percent Treasury securities is virtually immune from inflation.

Gold has been in a correction since October of 2012, shortly after Chairman Bernanke announced QE III.8 This may be one of the most extreme examples of “buy the rumor, sell the news” ever. Despite this, we are comfortable with our position and its role in the portfolio.

Again, we have no idea what the Fed’s next move will be. But, if the rapid backpedaling in response to the market’s reaction to the May 22nd comments are any indication, continued if not more QE is the path of least resistance.

About gold’s recent decline, Michael Lewitt in The Credit Strategist wrote, “First, a lot of gold was held by leveraged speculators who were forced out of the market as prices dropped.

Second, investors who view gold as an inflation hedge are abandoning the trade based on the low level of reported consumer price inflation in the U.S. Third, investors who view gold as a hedge against the inevitable demise of the fiat paper9 standard are coming to believe – wrongly in my view – that central banks are going to change their ways. For all of these reasons, gold is back to levels last seen in 2010.”

From a portfolio construction standpoint, one might expect gold to perform well when bonds don’t. After all, bond yields typically move with inflation expectations. Likewise, if real economic growth were to pick up, one would expect equities to perform well while bonds suffered. From May 22nd through the end of June, all three broad asset classes performed poorly. Gold certainly didn’t act as a hedge. This is because neither growth nor inflation expectations picked up. Instead, all asset classes reacted to the potential removal of some of the Fed’s market manipulation. We suspect this is a short-term phenomenon. Today, gold is trading close to its marginal cost of production and the Fed has backed away from the “tapering” comments. Perhaps gold has found a new floor.

Conclusion

June introduced the kind of violent market reaction one should expect when markets re-price based on the removal of Fed intervention. While we were not immune and the negative action was short-lived for many asset classes, the overall reaction to Chairman Bernanke’s May 22nd comments vindicates our approach. Our portfolios remain structured to deal with further shocks – be it more or less Fed intervention, a slowing economy, or a spike in measured inflation.

As Dylan Grice points out, the Fed’s manipulations mean we cannot guarantee ourselves long- term capital preservation by holding cash. With bank deposits paying zero, even modest inflation quickly eats away at our principal. Likewise, with equity markets at all time nominalhighs due to the Fed’s intervention, even the threat of removing the Fed’s support has proven short term capital preservation is impossible in equities. From our seat, the only sensible answer is to diversify portfolios such that they can survive any scenario. “Binary” or “all-in” bets are a recipe for disaster.

*****

As always, if you have any thoughts regarding the above ideas or your specific portfolio that you would like to discuss, please feel free to call us at 1-888-GREY-OWL.

*****

Sincerely,

GreyOwl Capital Management

Grey Owl Capital Management, LLC

1 Tail risk refers to the probability that a statistical value is in one of the two low probability “tails” of a normal (i.e. bell curve) distribution. Such events are by definition statistically unlikely, but depending on the situation could be disproportionately damaging.

2 For more information regarding performance, please refer to the performance disclosure at the end of this letter.

3 GMO is a value-oriented, institutional investment manager with $110B of assets under management. www.gmo.com

4 Starting valuations really do matter. Thirteen years later, the Nasdaq Index is still almost 26% off its March 10, 2000 intra-day high of 5132. When dividends are included, investors would be down 16%. Whereas, the Russell 2000 Value Index is up 237% including dividends over the same period.

5 Spread refers to the difference in yield between two investments (or asset classes or segments of an asset class). For example if the 5-year Treasury bond has a yield of 2% and a 5-year A-rated industrial company bond has a yield of 2.8%, the spread is 0.8%. We interpret Mr. Rosenberg’s use of “richer”to mean that the spread is narrower than it otherwise would be and thus providing less compensation for whatever degree of credit risk the investor is assuming. 100 basis points is equivalent to 1%.

6 Transfer payments include unemployment insurance, Social Security (including disability), Medicare, Medicaid, etc.

7 Warren Buffett coined this helpful analogy several years ago.

8 Gold actually peaked in price just over a year earlier in September of 2011, but then went sideways for about a year.

9 InvestorWords.com defines fiat money as money which has no intrinsic value and cannot be redeemed for specie or any commodity, but is made legal tender through government decree. All modern paper currencies are fiat money, as are most modern coins.

This newsletter contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves the potential for gains and the risk of losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Any information prepared by any unaffiliated third party, whether linked to this newsletter or incorporated herein, is included for informational purposes only, and no representation is made as to the accuracy, timeliness, suitability, completeness, or relevance of that information.

The securities discussed above were holdings during the last quarter. The stocks we elect to highlight each quarter will not always be the highest performing stocks in the portfolio, but rather will have had some reported news or event of significance or are either new purchases or significant holdings (relative to position size) for which we choose to discuss our investment tactics. They do not necessarily represent all of the securities purchased, sold or recommended by the adviser, and the reader should not assume that investments in the securities identified and discussed were or will be profitable. A complete list of recommendations by Grey Owl Capital Management, LLC may be obtained by contacting the adviser at 1-888-473-9695.

Grey Owl Capital Management, LLC (“Grey Owl”) is an SEC registered investment adviser with its principal place of business in the Commonwealth of Virginia. Grey Owl and its representatives are in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which Grey Owl maintains clients. Grey Owl may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements.

This newsletter is limited to the dissemination of general information pertaining to its investment advisory services. Any subsequent, direct communication by Grey Owl with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of Grey Owl, please contact Grey Owl or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For additional information about Grey Owl, including fees and services, send for our disclosure statement as set forth on Form ADV using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

The performance information for the Grey Owl Opportunity Strategy presented in the table above is reflective of one account invested in our model and is not representative of all clients. While clients were invested in the same securities, this chart does not reflect a composite return. The returns presented are net of all adviser fees and include the reinvestment of dividends and income. Clients may also incur other transactions costs such as brokerage commissions, custodial costs, and other expenses.

The net compoundedimpact of the deduction of such fees over time will be affected by the amount of the fees, the time period, and the investment performance. Grey Owl Capital Management registered as an investment adviser in May 2009. The performance results shown prior to May 2009 represent performance results of the account as managed by current Grey Owl investment adviser representatives during their employment with a prior firm. THE DATA SHOWN REPRESENTS PAST PERFORMANCE AND IS NO GUARANTEE OF FUTURE RESULTS. NO CURRENT OR PROSPECTIVE CLIENT SHOULD ASSUME THAT FUTURE PERFORMANCE RESULTS WILL BE PROFITABLE OR EQUAL THE PERFORMANCE PRESENTED HEREIN. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable. For additional performance data, please visit our website at www.greyowlcapital.com.

The indices used are for comparing performance of the Grey Owl Opportunity Strategy (“Strategy”) on a relative basis. Reference to the indices is provided for your information only. There are significant differences between the indices and the Strategy, which does not invest in all or necessarily any of the securities that comprise the indices. In addition, the Strategy may have different and higher levels of risk. Reference to the indices does not imply that the Strategy will achieve returns or other results similar to the indices. The performance shown for the iShares MSCI World Index Fund (“Fund”) includes performance of the MSCI World Index prior to March 26, 2008, inception date of the Fund.

© Grey Owl Capital Management