Market Melt-Up Catches Defensive Investors by Surprise

Executive Summary

- Extraordinary returns in the fourth year of a bull market remind us that long-term defensiveness can’t be rationalized.

- July saw remarkable returns across global equity and fixed income markets, with the exception of U.S. Treasuries.

- Investors would be well served to ignore media drama and fear mongering and simply follow the fundamentals.

- Five years spent worrying about Armageddon is too long, but there’s still time to get back to a normal allocation.

It is prudent to be defensive at times — but not forever. Some investors are learning the hard way that post-traumatic stress following an event like the 2008 Credit Crisis may inspire extreme risk aversion and the inadvertent reduction in wealth as a result. Five years into an extraordinary bull market admittedly peppered with troubling events — including the U.S. sovereign debt downgrade, the second anniversary of which coincides with this report — many investors and the media especially remain vigilant for the next sign of Armageddon.

The media referred to the equity markets’ success in the year that followed the August 2011 Standard & Poor’s action as a “stealth” rally, suggesting it was a big secret that the most widely followed stocks in the world were surging relentlessly. More recently the media has adopted the term “Goldilocks” to describe the financial environment; who could possibly have known that we would get a perfect balance of economic statistics — “not too hot/not too cold” — that would keep the Fed in an accommodative stance, perhaps forever? I don’t buy these attempted rationalizations for long-term defensiveness; investors are going to wake up one day wondering why they have been relegated to the sidelines during one of the most exhilarating bull runs in the history of both equity and fixed income markets.

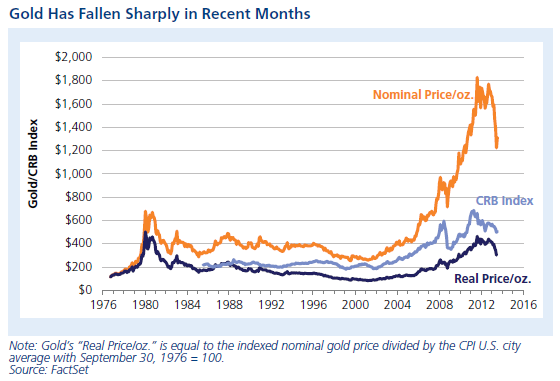

It seems that the more defensive an asset class, the worse its performance. Imagine the defensively inclined investor being told — incorrectly — that commodities are a good diversifying asset because of their low correlations with equity markets. Take gold, for example. The price of the metal peaked in 1980, entering a 20-year bear market before returning to an upward trajectory, only to drop like a rock — by more than 22% — year to date. Beware of statistics like correlation in the hands of inexperienced investors; adding a key metric like mean return would provide the insight required to evaluate the attractiveness and suitability to an investor’s portfolio.

Broad Global Diversification for Market Returns

July was a month of extraordinary returns across global equity and fixed income markets. U.S. small-cap equities were the best performers, surging 6.8%, followed by U.S. mid-cap stocks and MSCI EAFE index. Even bonds — with the exception of U.S. Treasuries, which were the only negative returning asset class out of a cross section of ten global assets — delivered a positive month. ETF flows into global equities had their best month this year, racking up $44.1 billion in inflows. The DJIA ended July with its sixth consecutive winning week.

Fundamentals Relentlessly March Forward

Investors would be well served by ignoring the drama incited by the media and Wall Street fearmongers and simply following the facts, as represented by our ABCDs of fundamentals.

Advancing earnings growth. Second quarter 2013 earnings season is shaping up to be good but not great. With 80% of S&P 500 companies having reported results, earnings have grown 1.7% over last year. This would be the third consecutive quarter of positive earnings growth. In contrast with the first quarter, top-line revenue has improved in the second quarter, posting year-over-year growth of 1.4% thus far.

Broadening manufacturing. The ISM Purchasing Managers’ Index surprised on the extreme upside, coming in at a whopping 55.4 in July. This was the highest reading in two years and has alleviated concerns of a manufacturing soft patch after the surprise slight contraction in May.

Consumer as the game changer. Retail sales moderated in June, growing only 0.4%. Still, aggregate sales exceeded $422 billion, the highest level ever. Additionally, auto sales increased at their fastest rate since 2007, a testament to the strength of the consumer. Finally, home prices continued to rebound sharply; Case-Shiller’s most recent reading showed a year-over-year increase of 12.2%, which will undoubtedly continue to bolster consumer confidence.

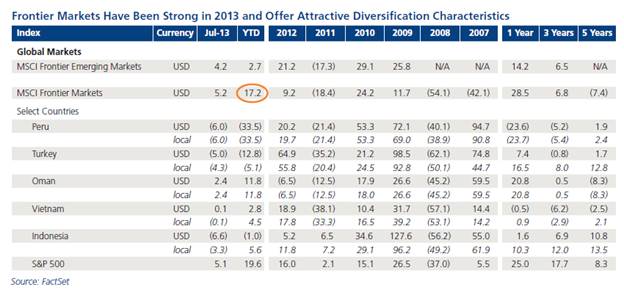

Developing markets. The emerging mark-ets have been battered this year but managed to post a positive gain in July. Interestingly, frontier markets — the next round of emerging markets — have delivered mostly positive returns this year, driving the MSCI Frontier Index up 17.2% through end- July. In their search for safety, investors may have missed one of the best — if somewhat counter-intuitive — defensive plays around. Yes, individual frontier countries may be volatile in the short run, but a broad collection of these markets provides portfolio diversification as well as upside potential

Tectonic Shifts: Energy

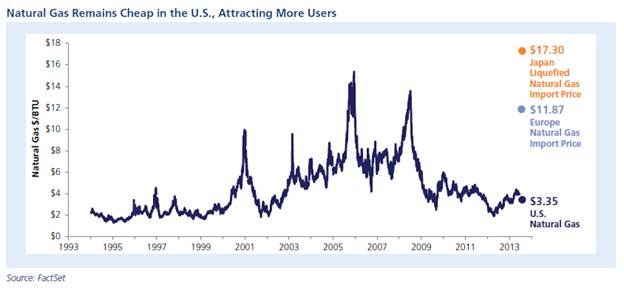

The natural gas revolution is a catalyst for growth that is astounding the market and gaining steam. Just this month Ford, the manufacturer of the most popular full-size pickup truck in the world, announced that it will begin selling a pickup truck later this year that is modified to run on compressed natural gas. Natural gas prices, already exceedingly cheap, are down 17% since April, adding to a steady expansion of gas use by a wide range of foreign and domestic manufacturers, from chemicals and steel toglass and fertilizers. In fact, the companies that use natural gas in the U.S. may be the biggest beneficiaries of the shale revolution; Businessweek reports “Cheap natural gas is powering a $100 billion investment boom in the U.S. chemical industry led by foreign companies.”

Getting Back to Normal

We feel it’s worth reiterating an idea we proposed last month: Five years spent worrying about Armageddon is too long.

This is evident by the surge in a variety of fundamental metrics:

• S&P 500 corporate profits at a record high

• S&P 500 Index and Dow Jones Industrial Average at record highs

• Retail sales at a record high

• Housing markets posts largest year-over-year price increase since March 2006

It was prudent to take a defensive investment posture in the immediate aftermath of the worst bear market since the Great Depression. But just as you wouldn’t remain hunkered down in an emergency shelter five years after a devastating hurricane, it is unproductive to maintain a risk-averse investment allocation long after the most acute danger has passed. A portfolio globally diversified across equity and fixed income markets defends an investor’s assets while also releasing the power of compound returns that build wealth. Accepting meager, cash-like returns and calling it risk management is neither prudent nor accepted investment management practice.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 7165