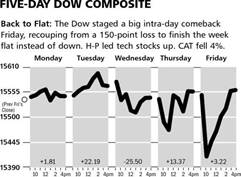

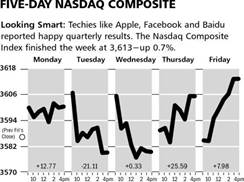

Stock averages were nearly unchanged last week as earnings reports are being reported mostly in line albeit with the usual concerns about the pace of economic activity. This is reflected once again by a lack of revenue growth for many industries.

As the charts above illustrate the Dow Jones Industrial Average was flat last week while the NASDAQ Composite moved higher by .7% as the news from

Apple was not as bad as many had feared (neither was it exciting).

The Markets & Economy

Turmoil around the world including the Middle East and the horrible economic news emanating from Europehas failed to leave a mark on stock prices. The odd dichotomy between what societies are experiencing and how investors are faring continues unabated.

Europe’s problems are being massaged to not reach a boiling point until after the German elections the third week in September. Here at home, the Obama administration is delaying (perhaps lawlessly) implementation of the employer mandate part of Obamacare until after the 2014 mid-term elections. All of these measures are simply attempts to “kick the can down the road”.

Meanwhile governments in Italy, Greece, Portugal and Spain, just to name a few, are very close to falling as they lack clear majorities in their respective parliaments. Then, of course, there is Egypt where some sort of revolution is underway and the Civil War in Syria has now seen over 100,000 deaths and counting.

All of this has held up the price for oil even as the USA is becoming less and less dependent on foreign oil. This is truly a very bullish development and a positive for the American consumer. The only problem is that many states (including the Commonwealth of Massachusetts ) have responded by raising gasoline taxes. Thus the benefits gained by the private sector through exploration are being expropriated by the government sector to the detriment of the consumer and economic growth in general.

Where is the media to report on such problems? The bottom line is that the positives and negatives are washing each other out and stocks are benefitting along with the investor class. Consumers and those looking for full-time employment are bearing this negative impact disproportionately and nothing is due to change soon.

What to Expect This Week

…Quite a bit, actually. Earnings reports will continue forth. Additionally, the FederalReserve Board has a two-day meeting which will keep financial markets who are on the edge of their seats waiting to see when/whether the Fed will “taper”. What a world!

Friday will bring the employment report for July. The expectation is for a gain of some 175K non-farm payroll jobs, but as you know this number is so manipulated through assumptions and political pressures as to be useless.

The chart below, which shows the proportion of those working to the population as a whole, tells you all you need to know. Things are lousy for many people, and the sort of economic growth likely to be seen over the next few years as discussed above is not likely to help them. It just serves to make them even more dependent on a bankrupt federal/state/city government.

With this as a background, don’t be fooled by those who want to pretend things are getting better in a self-sustaining manner. Remember today’s pathetic growth rate has required zero interest rates, a one trillion dollar or more federal annual deficit and a Federal Reserve printing one trillion paper dollars per year. Take away those props and who knows what the underlying strength of the economy is. Don’t forget next year’s looming Obamacare taxes as well.

Stocks in secular growth businesses (natural gas infrastructure for instance), and those with rich dividend histories still look solid.

Finally, our weekly look at the Economic Cycle Research Institute’s leading economic index shows more muddling along. No surge there and neither is there a collapse, but I will say that housing is looking soggy again and that is another reason NOT to expect much higher interest rates anytime soon.

![]()

SYMBOL: BA

Boeing reported better than expected second quarter earnings last week as demand for its commercial aircrafts continue to gain momentum globally. Net income rose 13 percent to $1.09 billion, or $1.41 per share, which was 15 cents higher than consensus estimates. Revenues also grew by 9 percent from last year to $21.82 billion. Management also raised its earnings-per-share guidance for the remainder of this year by a dime. We expect this new guidance is still too conservative.

The demand for Boeing’s fuel-efficient aircrafts continues to head higher as the Company ramped up its production of both of the 737 and 777 aircrafts. On the conference call with investors CEO Jim McNerney indicated that Company will likely have to increase shipments of 737, 777 and 787 aircrafts during the second half of this year. The Company has booked orders for 83 more 787’ s this year, and delivered sixteen 787’s in the past three months. Boeing delivered a total of 169 commercial aircrafts during the quarter, which was up from 150 last year.

Not only is demand for Boeing’s products accelerating, but the Company continues to improve its financial position. Boeing generated over $3 billion in free cash flow during the second quarter, up from just $552 million last year. Operating margins also rose across the board, even with defense spending flattening out during the quarter. We expect management will use this large cash position to either raise its dividend or aggressively buy back stock in the second half of this year.

Even though the 787 remains in the headlines for smaller technical issues, Boeing shareholders are being rewarded now that the Company is in the sweet spot of its business cycle. Airlines around the world have to continue to upgrade their aging fleets, and Boeing has the best products on the market. We look for a strong second half of this year, and believe the shares will reach $150 by the end of 2014.

![]()

SYMBOL: BIIB

Biogen Idec reported blockbuster second-quarter earnings results last week, boosted by its recently approved drug Tecfidera. Excluding one-time items, the Company earned $2.30 cents per share, which was 36 cents better than Wall Street’s consensus estimates. Revenues also rose significantly during the quarter, and management raised its revenue growth forecast to 23 percent for this year. The Company now expects to earn $8.50 per share this year, which is 7 percent higher than its previous guidance.

The early results from the launch of Tecfidera have been much better than expected. The pill was only approved on March 27th of this year, and the Company already booked $192 million in revenue. This was nearly 3 times more than Wall Street was expecting, as demand for this product has been greatly underestimated. Most analysts expect the drug to book $3.5 billion in annual revenues by 2017. The Company’s other treatments for multiple sclerosis also had strong performance during the quarter.

The share price of Biogen Idec was volatile last week after a report of a patient’s death who had been taking Tecfidera. A 59-year-old woman that had been taking the drug for 5.5 weeks died from pneumonia. It was reported that the woman had gastrointestinal problems prior to taking the drug and stopped two and half weeks before her death. From all data currently available, the death is unlikely to have any link to Tecfidera. We expect this to be a non-issue for the company in coming months.

Shares of Biogen initially surged following these solid earnings results, but investors began taking some profits later in the week. We expect the news concerning Tecfidera to only improve as we believe WallStreet is still being too conservative with its growth assumptions. We also look for the management team to make more acquisitions in the second half of this year to add to its industry-leading drug pipeline. We believe the shares will move to $300 within the next12 months.

SYMBOL: AKAM

Akamai reported strong second-quarter results last week, as more consumers are watching higher-quality videos online. Excluding one-time items, the Company earned $0.46 per share, which was one cent better than consensus estimates. Revenues rose by 14 percent from last year to $378.1 million, which was the second quarter in a row that the Company exceeded revenue expectations. The management team also maintained their previous guidance for the rest of this year.

Strong internet traffic growth helps to drive higher earnings for Akamai, and we believe we are still in the early stages of video migrating to the net. Akamai has a fairly dominant position in this market, and the Company has been successful inking new profitable deals with large media companies. We are encouraged by market trends, and expect Akamai to increase its market share of profitable business during the second half of this year.

Shares of Akamai have traded roughly 30 percent higher during the last three months, and the price has continued to surge following this report. We believe an acquisition of Akamai makes more sense now than it ever has, and we wouldn’t be surprised to hear that several large technology conglomerates are taking a look at the Company. We expect the positive news flow will continue to push the share price higher, and look for $55 within the next 12 months.

© McIntyre, Freedman & Flynn