ING Fixed Income Perspectives July 2013

Bond Market Outlook

Global Interest Rates: We are constructive on interest rate risks in many developed and emerging economies as global central banks reinforce accommodative monetary policy.

Global Currencies: We favor the U.S. dollar versus the Japanese yen, the Euro and other developed market currencies.

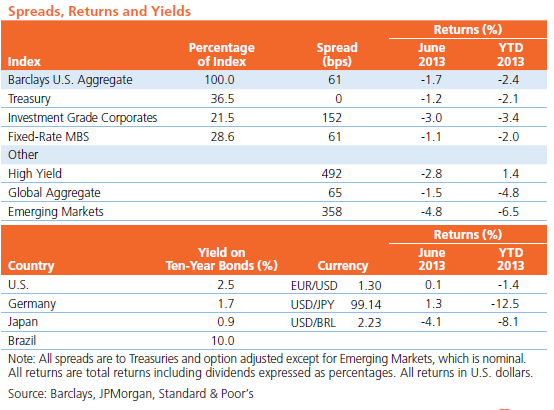

Corporates: Credit spreads should narrow from current levels as the markets gain confidence and the Treasury market stabilizes.

High Yield: Spreads offer more than adequate compensation for likely credit losses and a further rise in interest rates.

Mortgages: Spreads have been pressured to pre-QE3 levels and mortgages look attractive at these higher levels as prepayment speeds slow.

Emerging Markets: We remain cautious in the emerging markets due to benign global growth expectations and higher developed market rates.

Macro Overview

- ‘The Great Kate Wait’ is over — finally. Time to shift gears to more mundane obsessions like the due date of Fed tapering. But with a September taper likely fully priced in, the Fed committed to long-term low rates, and no inflation born of quantitative easing worth celebrating yet, what’s all the hullaballoo about? The market getting stuck on the difference between tapering and hiking is like those British parents who made the unfortunate mistake of combining Barb and Dwyer in naming their firstborn child. Because, even if the Fed decides to buy less this year, the 6.5% level of unemployment is not sufficient in and of itself to prompt an interest rate hike, and the labor market data, according to recent comments by the Fed Chairman, may overstate the health of the labor market. In fact, the Fed, ever data dependent, has suggested that it would fight back against any tightening of financial market conditions that jeopardized its inflation and employment objectives.

- In other words, the advent of Fed tapering is overblown because, even with a stronger U.S. labor market, weak global growth and benign inflation are likely to continue in the third quarter of 2013. This means more, not less, central bank liquidity globally. And the fact that forward indictors of inflation like TIPS were crushed — the May/June interest rate tizzy moved real rates higher and inflation expectations, perversely, lower — also means that the market overshot the explicit central bank guidance on rate hikes, which are still not expected until mid-to-late 2015.

- This mispricing moved interest rates into cheap territory for the first time in over two years, and has provided tactical opportunities in spread sectors like High Yield and Securitized Credit that are now cheaper and benefit from the higher rate base. Interest rate valuations have already begun to retrace in the near term; an outcome market participants should expect in a world wrought by deflationary, not inflationary, pressures. But ‘the Great Fed Wait’ is not over and will likely cause continued upticks in volatility as the market fixates — rightly or wrongly — on its significance.

Sector Overviews

Global Interest Rates

- The Bank of Japan continues its ambitious asset purchase program, leaving the door open to do more, while the ECB has uttered the magic words “extended period” to describe the duration of its accommodation. The Bank of England has also moved towards forward guidance, and emerging market central banks have added to these highly accommodative bank funding conditions. Even with September tapering, the Fed is likely to purchase $600-800bn more in Treasury and Agency Mortgage-Backed Securities.

- Inflation and global growth remain subdued, and given favorable valuations in light of the May and June selloff, we are constructive on interest rate risk in a number of developed economies, including the United States, Australia, and Germany, all of which should benefit as global central banks reinforce accommodative monetary policy. We are also positive on higher-yielding emerging economies including Brazil, Russia, and South Africa.

Global Currencies

- We continue to maintain the U.S. is the most credible growth and recovery story in the developed world, and remain constructive on the U.S. dollar and its relative strength versus the Japanese yen, the Euro, and other developed market currencies.

- We are cautious on emerging markets, as the outlook for a strong U.S. dollar does not bode well for sustained strength in emerging market currencies, but are constructive on higher yielding and attractively valued currencies like Brazil, Mexico, China, Nigeria and Malaysia.

Investment Grade Corporates

- The recent back-up in Treasury yields and credit spreads constitutes an opportunity for corporate spreads to narrow as the U.S. economy continues to improve and underlying credit fundamentals remain healthy with the earnings season off to a strong start.

- We continue to favor Financials in the 2013 credit market, driven by better visibility on earnings growth and less likelihood of event risk compared to other sectors. We also continue to favor BBB securities over A-rated securities from a valuation standpoint, and remain bearish on the metals and mining industries, which are weighed down by weak growth in emerging markets.

High Yield Bonds

- The high yield market has shifted its concern from credit to rising interest rates as investors become convinced of a recovery — however uninspiring — in the U.S.

- Corporate balance sheets remain healthy enough to prevent a meaningful increase in defaults for some time, even with low U.S. growth. High yield spreads, at approximately 500bp above Treasuries, offer more than adequate compensation for credit losses. Their ability to absorb at least a portion of a further rise in interest rates positions high yields to outperform most other fixed income asset classes. Still, we expect macro headline-induced volatility to continue through the remainder of 2013.

Mortgages

- Fears of the Fed slowing, and ultimately ending, the $40 billion of Agency MBS and $45 billion of long maturity U.S. Treasuries purchases per month pushed Agency MBS yield spreads beyond pre-QE3 levels long before any ‘tapering’ of QE3 is actually expected.

- This latest surge in mortgage rates leaves the majority of borrowers without an economic incentive to refinance. Thus, prepayments are expected to slow over the summer diminishing the available supply of Agency MBS to market participants, and creating an extremely attractive supply/demand profile given higher rates.

- The technical picture has proven challenging of late for Non-Agency MBS as record-setting redemptions have pressured spreads wider. The asset class continues to benefit from an improving housing market, and while rates will need to stabilize for liquidity to improve, the market will not be able to ignore the relative attractiveness of this asset class for long.

- CMBS continues to be supported by the recovering commercial real estate market, but the technical picture is of concern with elevated new issue supply and a soured appetite for interest rate risk. As rates stabilize at these higher all-in yields, we would anticipate renewed demand, particularly from longer-term holders like insurance companies.

Emerging Markets

- Emerging markets stabilized somewhat in July, a trend that will likely continue as liquidity improves and the outlook for outflows becomes clearer. However, we remain cautious in the near term across the emerging markets complex due to the negative technical picture and concerns about the potential impact of weaker commodity prices, slower emerging market real GDP growth, higher U.S. interest rates, and other potential market and economic impacts from the prospect of Fed tapering.

ING U.S. Investment Management’s fixed income strategies cover a broad range of maturities, sectors and instruments, giving investors wide latitude to create a new portfolio structure or complement an existing one. We offer investment strategies across the yield curve and credit spectrum, as well as in specialized disciplines that focus on individual market sectors. We build portfolios one bond at a time, with a critical review of each security by experienced fixed income managers. As of December 31, 2012, ING U.S. Investment Management managed $127 billion in fixed income strategies in the United States.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 7071