Dear Shareholders:

Overview

FPA Crescent returned 2.95% in the second quarter and 10.38% in the first six months of 2013, as compared to the S&P 500’s returns of 2.91% and 13.82% respectively.

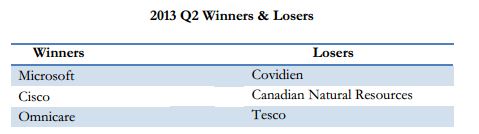

The second quarter’s winners and losers are as follows:

The largest three contributors added 1.28% to our second quarter return, while the detractors cost the fund 0.53%. In the past, we have described our investments in Canadian Natural Resources and Tesco, and while the price of each has bounced around, other than that little has changed. Covidien had the biggest positive impact on Q1’s performance, only to decline so much in Q2 that it topped the “Losers’” chart. While still early in the quarter, Q2’s “Winner”, Microsoft, is now trying to pull a “Covidien” as it is leading the early Q3 charge for poor performance. Needless to say, stock prices change far more than intrinsic value and our quarterly reporting of winners and losers only serves to answer the frequent question as to what drove the Fund’s recent performance. We suggest you don’t read any more into it than that, as it is more a curiosity than a foreteller of future performance.

Ultimately, we pay more attention to the underlying financial performance of the companies in our investment portfolio than we do their stock charts and in one instance, Omnicare, the largest supplier of pharmaceuticals to patients in nursing homes, delivered in spades. New management came in several years ago and began executing on a business plan that revolved around basic blocking and tackling to improve performance. While the engineer of the turnaround, John Figueroa, has handed off the plan to his successor, the momentum remained intact under the present CEO, John Workman. The company has lowered costs, reduced customer churn, won new accounts and essentially built the best mousetrap in the institutional pharmacy space. The net result is that all of the aforementioned improvements in aggregate have manifested themselves in the form of higher and more consistent earnings. Those achievements and the belief that the company’s future continues to look bright are reflected in a stock price that has more than doubled from our original cost.

Economy

Our views on the economy are not terribly original and have not changed significantly in the past six months. It’s a challenge finding new ways to say the same thing. So we won’t. We think our past commentaries effectively communicate our longstanding view that as we exited the 2008-9 financial crisis, the average Joe on the street was left with less in his bank account, a diminished home value, and what stocks he did own weren’t worth as much. When Joe could afford less, the U.S. government stepped in and spent in his place, and hasn’t stopped spending since. What the Joes of the world can’t afford, the U.S. government apparently can – but don’t ask us to explain that “new” math. The recovery has been disappointing and largely engineered by central bank policy. We worry that low interest rates and novel and theoretical Fed policy could lead to unintended consequences.

The past quarter included a brief hiccup when investors considered their exposure to low interest rates in the event the Fed allows rates to normalize. There was a lot of discussion in the media during the past quarter regarding how and when Ben Bernanke intends to taper the purchase of bonds by the Federal Reserve. Interestingly, we can’t recall having a single conversation internally about the taper, as this simply isn’t how we look at the world. We are worried about how a business and the world might look three to five years from now, not next quarter. In fact, if one thinks back five years, the world has dealt with a great financial crisis, potential currency collapse and fears of sovereign liquidity, just to name some of what we have seen. Through it all, we invested with a long-term strategy dependent on patience, discipline and a focus on longterm value. With an average holding period of roughly five years, we strive to add value over a full business cycle rather than try to guess where central bankers may move interest rates.

On the other hand, many investors who took a myopic approach and chased short-term yields were met with a rude surprise this past quarter as interest rates spiked higher. During this period, rate sensitive investments – including real estate investment trusts (REITs) - declined in value, especially those that use leverage to invest in leases. Our appreciation for the macro backdrop, coupled with our value standards, has resulted in the portfolio eschewing yield enhancing investments (REIT, MLP, Bonds) over the past few years.

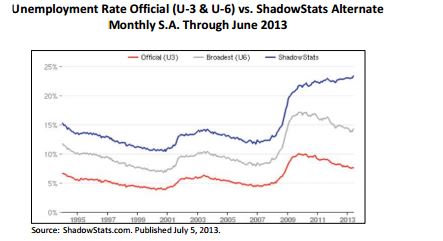

The apparent decline in the unemployment rate is something of a bright spot in the US economy, but as you know, we have long held reservations about how this statistic is reported. Unemployment has largely declined because many have left the workforce.1 Since 1984, on average, 66% of the population worked, but now it’s just 64%.2 That may not seem like much of a change, but for every 1% of the population that gives up seeking work, unemployment declines by 1.5%. If one were to assume that the U.S. shouldn’t be any different than it has been historically, then unemployment would currently be 10.6%. In addition, the ranks of the employed include an increasing number of people working part-time, but many part-time workers would prefer full-time employment. 3 John Williams’ Shadow Government Statistics tries to get to the truth behind government economic reporting. His less sanguine view of unemployment is represented below and reflects a new record high. We don’t know if his number is correct but we certainly agree directionally, as does Mr. Bernanke, who said that the current unemployment rate is “not exactly representative of the state of the labor market.”

We would like to believe that Fed officials understand this, but you wouldn’t know it from the way they talk. In their June 19 press release, Fed officials said, “the Committee reaffirmed its expectation that the current exceptionally low range for the funds rate will be appropriate at least as long as the unemployment rate remains above 6½ percent so long as inflation and inflation expectations remain well behaved.” We have already established that the unemployment rate definition is loose at best, but now we apparently have to determine the nature of inflation’s comportment. Instilling little confidence, the Fed interprets this combination of data and tea leaves to justify its bond purchasing taper and ultimate exit. The Fed governors seem to be using, as the Scot poet Andrew Lang once wrote, “statistics as a drunken man uses lamp posts, for support rather than illumination.”

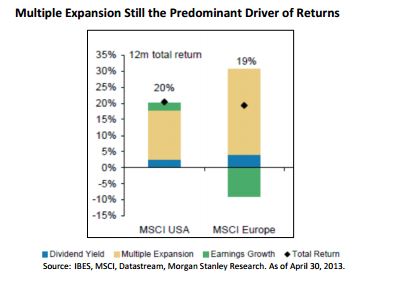

Government assistance has yet to be felt in any kind of substantive, let alone sustainable, way. But the Fed, along with other central banks, has certainly been successful in lifting asset prices. As can be seen below, the vast majority of the market’s return in the U.S. and Europe over the past year has been driven by multiple

expansion.

We find it difficult to invest in an environment that seems manipulated to engineer higher asset prices regardless of business fundamentals. So, instead, we allow cash to build and spend our time building an actionable inventory for the future.

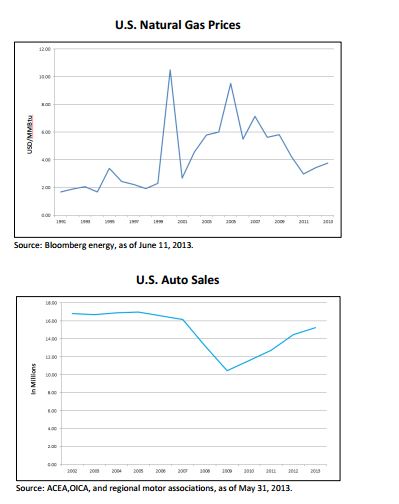

Despite our fiscal policy concerns, we recognize that economies have a way of overcoming difficulties and that there are a number of bright spots in the US. In particular, housing looks to be entering a period of strength. U.S. manufacturing continues to have the benefit of lower input costs, thanks to natural gas prices that remain far lower than in many parts of the industrialized world. What’s more, auto sales are still well below average and the construction industry (commercial and residential) is still far off its peak.

If this brief discussion leaves you wanting and frustrated, then we have succeeded in fostering a feeling that sits in the pits of our stomachs. We wish we could offer more, but we are torn between a concern over the unintended consequences of novel policy and the knowledge that things tend to work out in the long run. As for the portfolio, we invest when we find opportunities that offer a margin of safety4 and the prospect of an attractive real return. We avoid those investments that appear overly exposed to obvious macro excess. Macro excess can go on for years, though, so as we discuss in the following Investments section, we continually investigate a broad swath of prospective investments – companies, industries, asset classes, all located in different geographies, mostly public but some private.

1 Bureau of Labor Statistics, bls.gov. June 2013 not seasonally adjusted.

2 Population = civilian non-institutional population, excluding, among other people, those younger than 16 years and those who have been incarcerated.

3 Unemployment is going down due, in some immeasurable part, to Obamacare. The Patient Protection and Affordable Care Act (PPACA) requires that beginning in 2015, companies must provide health insurance to those employees who work 30 hours a week or more. Many companies are reducing payroll hours ahead of time, particularly those that already operate with a significant portion of part-time labor (like restaurant chains) with the commensurate benefit being an increase in employment, albeit part-time. The unforeseen side effect of the PPACA is many employers are reducing weekly hours below the 30 hour/week threshold that requires that they provide healthcare to employees.

4 Buying with a “margin of safety” is when a security is purchased for less than its estimated value. This helps protect against permanent capital loss in the case of an unexpected event or analytical mistake. A purchase made with a margin of safety does not guarantee the security will not decline in price.

To continue reading, please click here.

© FPA Fund